Driving down inflation without major job losses is a balancing act the Federal Reserve rarely nails. But hope for a “soft landing” is growing after this past week, as is the hype.

History tells us it could be too good to be true.

“We were having these same types of discussions in 2000 and again in 2007,” former Dallas Fed adviser Danielle DiMartino Booth said. “I was in the business back then and what was remarkable then — and the parallel to today — is the ubiquity of the soft landing consensus. Everybody thinks that this is the direction we’re headed in.”

“You’re often in a very dangerous environment when there is all across-the-board agreement as to where you’re headed,” DiMartino Booth, CEO and Chief Strategist of QI Research, continued. “When I was working at the Dallas Fed [in 2007], there was a high-up economist who said that it was going to be a soft landing, that the economy was going to moderate but not contract.”

Of course, what happened next was the most severe economic recession since the Great Depression.

Today’s economy

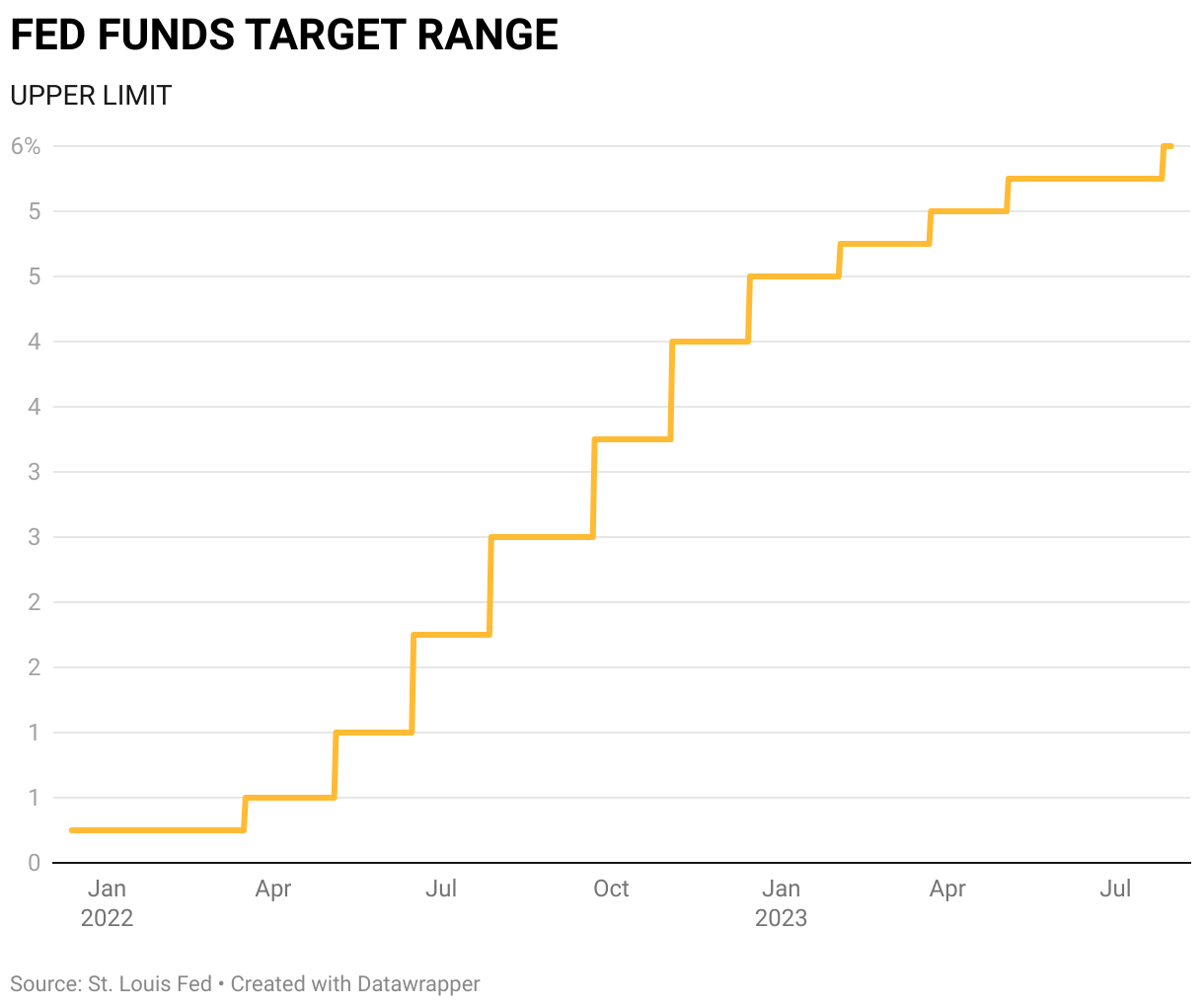

During the week of July 23, the Fed raised its interest rate for the 11th time since March 2022, to a restrictive level of 5.25% to 5.5%.

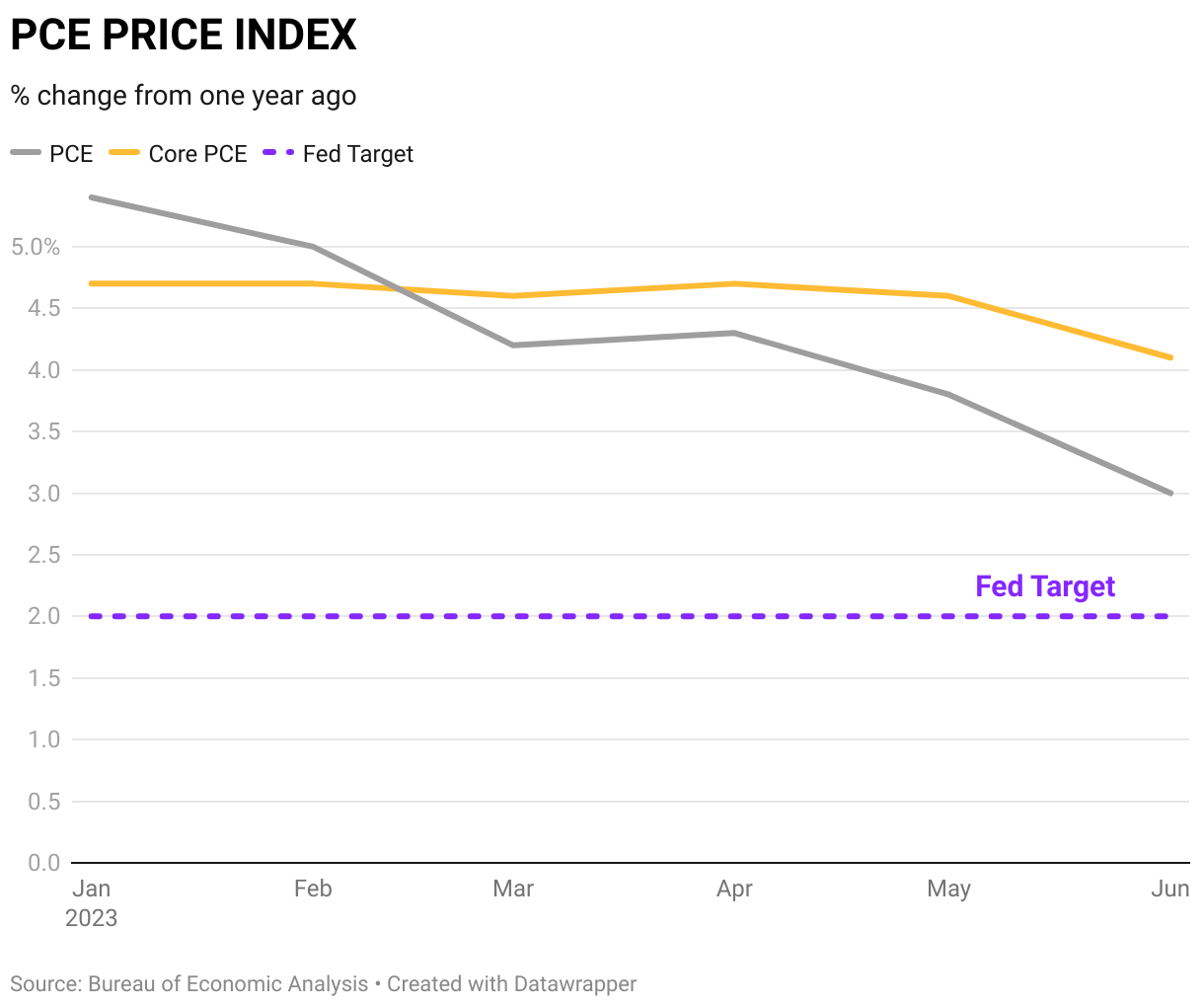

Two days later, core PCE — the Fed’s preferred inflation gauge — finally budged for the first time in 2023, down to 4.1%. That is still more than double the Fed’s target inflation rate.

“Core inflation is still pretty elevated. There’s reason to think it can come down now, but it’s still quite elevated and so we think we need to stay on task,” Fed Chair Jerome Powell said following the latest rate hike. “We think we’re going to need to hold policy at restrictive levels for some time. And we need to be prepared to raise further if we think that’s appropriate.”

The lag effect

The Fed is constantly advising that it will consider the lagging effects of monetary tightening as it makes decisions on whether or not to continue hiking the rate into more restrictive territory.

“We are in the teeth of the 12- to 18-month lag window when that first tightening that came out in March of 2022 should be biting,” DiMartino Booth said. “We are seeing the tightening effects manifest in the U.S. economy. But if you’re only looking through the prism of where the stock market is, then you might end up feeling as if you’ve been sideswiped by reality when it hits.”

The latest jobs report put U.S. unemployment at 3.6%, a historically low rate. The July payroll data will be released Friday, Aug. 4, with one additional jobs report and two months of inflation data available to the Fed before its next meeting.

DiMartino Booth noted that unemployment tends to rise after the U.S. has already entered a recession. The flags in the economy she is paying close attention to are bankruptcies, the closure of small businesses, bank mergers and failures, and shuttering of large businesses like Yellow Corp., a 99-year-old trucking company that announced Sunday, July 30, it’s closing its operations and laying off 30,000 workers after a union stalemate.

“Pay attention to what’s happening around you, not just what you’re seeing in terms of what the financial media is telling you should be seeing,” DiMartino Booth said.

Hiking is just the half of it

For the Fed to engineer a soft landing, knowing when to stop hiking is just part of the equation. Holding restrictive rates for an appropriate amount of time and then cutting rates before a recession ensues will prove to be an even tougher balancing act for the central bank.

Watch the video above to hear why DiMartino Booth said, “The Fed is already too late.”