Whatever happened to that recession? Several months ago, top economists predicted the country would be in a recession right now. Instead, consumer confidence just hit a 2-year high in July, the U.S. unemployment rate is 3.6%, and gross domestic product numbers due this week are expected to show a growing economy for the second quarter of 2023.

A large majority of surveyed business economists – 71% – now say the odds of the U.S. entering a recession in the next 12 months are 50% or less, according to the latest National Association of Business Economics survey.

Fitch Ratings was among the leading agencies predicting a recession by the second quarter of 2023. Now, updated forecasts point to a mild recession in the last quarter of the year and the first quarter of 2024.

“The bottom line is that this is a very resilient economy and the strength of the labor market has surprised everybody,” said Olu Sonola, head of U.S. Regional Economics at Fitch Ratings. “There’s a possibility that may actually continue, even though we think the labor markets would weaken from the third quarter going out through to 2024.”

Fed set to hike rate again

After pausing rate hikes in June, the overall consensus is that the Federal Reserve will again hike the federal funds target rate on Wednesday, July 26. It currently sits between 5% and 5.25%, whereas a hike will bring the borrowing rate to 5.25% to 5.5%.

“It seems like it may be one and done because inflation numbers have been surprisingly lower than expected. We’re at 3% now. Nobody actually thought we’d be at 3% this quickly,” Sonola told Straight Arrow News. “But I think the Fed will be paying a lot more attention to core inflation, which is still more than double its target.”

For that reason, Sonola said they cannot rule out another rate hike later in the year. Fitch Ratings currently predicts the Fed will start cutting rates around March 2024, with inflation at around 2.5% to 3%.

Lower headline inflation distorting true inflation picture

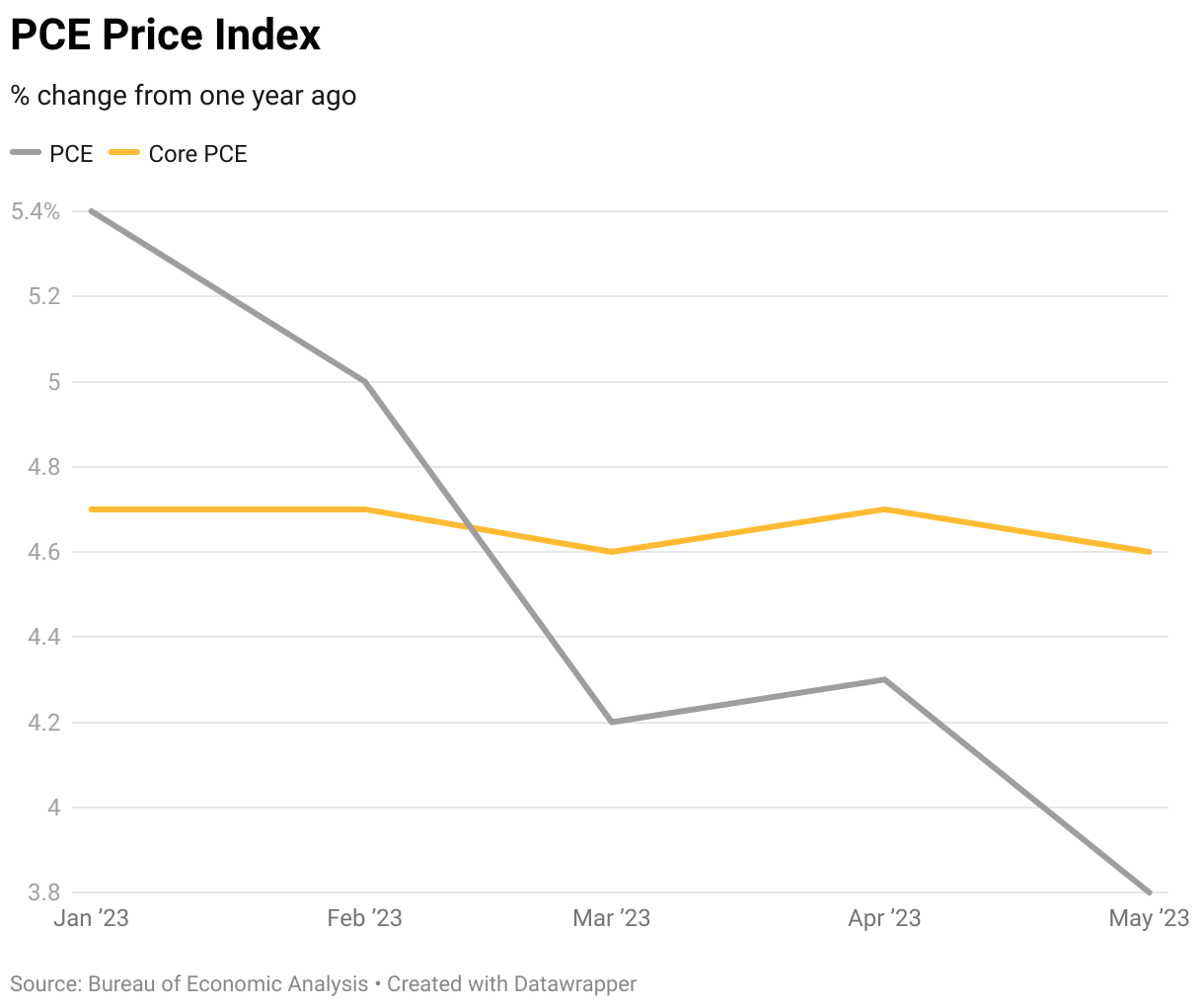

Despite significant declines in headline inflation numbers from the consumer price index and personal consumption expenditures price index, core inflation is proving much sticker.

In the Fed’s preferred inflation gauge, PCE, core prices, which exclude more volatile food and energy indexes, have barely budged all of 2023. While overall annual PCE has gone from 5.4% in January to 3.8% in May, core PCE has hardly moved, from 4.7% in January to 4.6% in May.

Sonola agreed the headline inflation figures are distorting the real picture largely because energy has been so deflationary. Gas prices are down 26.5% in the past year, according to the latest consumer price index.

Meanwhile, housing prices are fueling core inflation while strong wage growth has led to sticky service industry prices. For instance, while food-at-home prices month-to-month are barely growing in 2023, food-away-from-home prices are climbing at much stronger clips.

“Unemployment below 4% is probably still going to bring about inflationary pressures on the wage front,” Sonola said. “As perverse as this sounds, the Fed will be happy to see unemployment in the 4% range, 4% to 4.5%, just so that takes away the pressure on wages.”