Markets are increasingly betting the Federal Reserve will make a supersized rate cut at this week’s meeting. There are two camps: Those who believe the Fed will cut interest rates by 25 basis points and those who believe the Fed will double up to 50 basis points.

A week ago, 2 out of 3 futures traders were betting the Fed would do a 25 basis point cut, according to CME FedWatch.

But by the time the Fed started its two-day meeting the morning of Tuesday, Sept. 17, odds had switched. As of 10 a.m. ET, 2 out of 3 futures traders were betting on a jumbo cut to kick off this rate-cut cycle.

“The market is thinking this because the market is sniffing out some economic weakness,” Fed Guy and CIO of Monetary Macro Joseph Wang told Straight Arrow News. “They’re noticing that the unemployment rate has gone up. It seems like there are a lot of indicators that the Fed might be over-tightening, and so in order to get ahead of this, the Fed might want to do with a supersized cut. Now I’m not in that camp, because so far, what I hear from Fed speakers is that it’s more likely that the economy is normalizing.”

Wang is in the 25-basis-point camp, joined by former Fed adviser and QI Research CEO Danielle DiMartino Booth.

“They want to be measured and gradual,” DiMartino Booth told Straight Arrow News. “They want to be Greenspan-esque. [Former Fed Chair Alan] Greenspan had 17 25-basis-point rate hikes in a row. So it was a little bit different dynamic. It was a tightening campaign, but they want to be as measured. They want to be able to say, ‘We’re going to engineer a soft landing. We’re going to be taking interest rates down at a very slow pace.’”

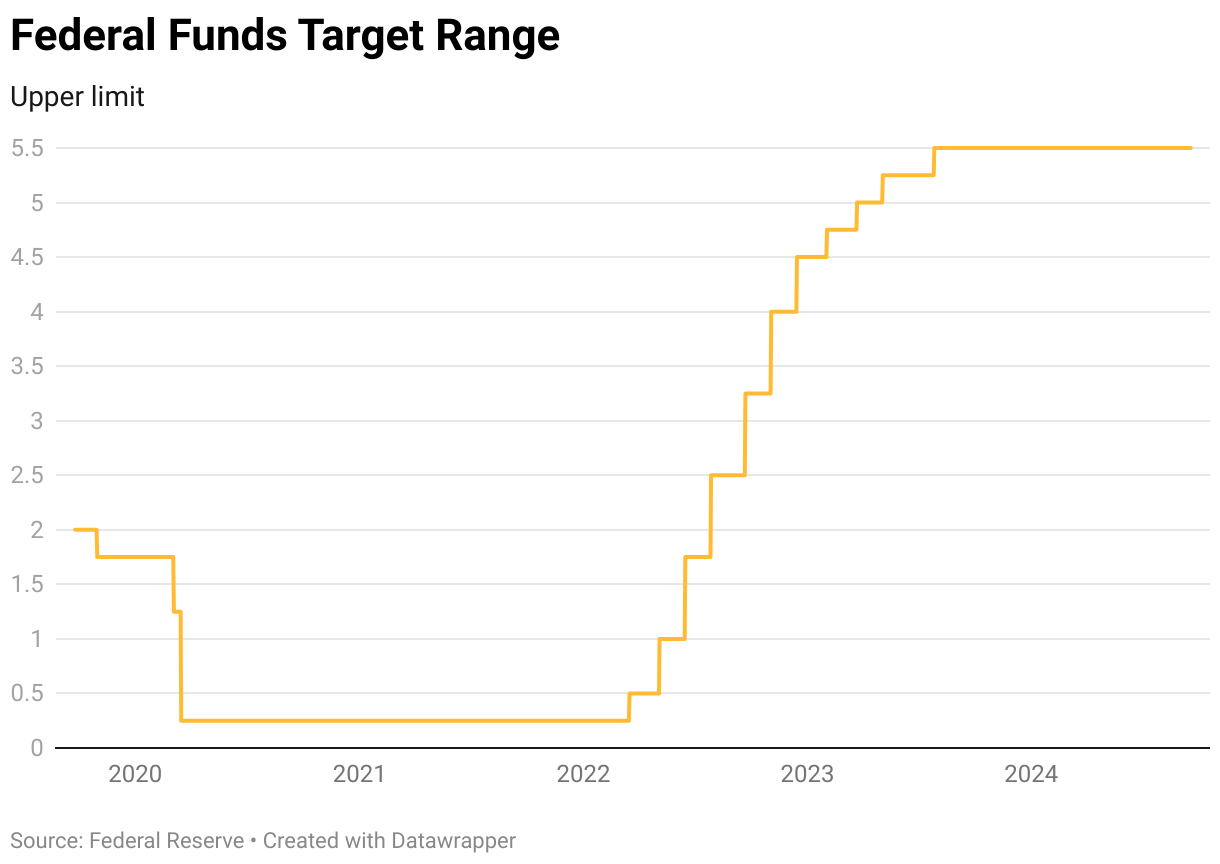

When inflation started getting out of hand in 2022, the Fed began its rate-hike campaign to tighten monetary conditions and get people and businesses to spend less. It hoped the move would bring down prices.

The team hiked the Fed funds target range all the way to 5.5%. They’ve held it there for more than a year now. This is the highest the rate has been since early 2001.

But now inflation is much closer to the Fed’s 2% target, the unemployment rate is rising. Therefore, a soft landing is getting more elusive.

Markets are betting that the Fed funds rate will go down to below 3% by next summer. That would mean cutting 250 basis points in less than a year.

“The pricing in the market seems to be pretty aggressive,” Wang said. “From my perspective, I think there’s too much doom and gloom being priced in. My base case expectation is that rather than having a series of huge cuts that the market is assuming that we have, some steady 25 basis point cuts, and maybe the cut cycle ends, let’s say around 3.5%, rather than below 3%.”

Wherever it lands, Americans will see a change in what it costs to borrow money. In the same way as when the Fed was hiking rates and mortgage rates, auto loans and credit card interest rates soared, this time those interest rates will also go down.

In fact, it’s already happening. Ahead of Wednesday’s Fed cut, mortgage rates fell to levels not seen since early 2023. If the Fed cuts rates by 25 basis points following its meeting, that cut is likely priced into the current mortgage rates. But if they go jumbo-sized to 50 basis points, mortgage rates could go down even more.

Subscribe to the Straight Arrow News YouTube page and tune in Wednesday, Sept. 18, at 2:10 p.m. ET, where SAN will have a live report of the Fed’s final decision and comments from Fed Chair Jerome Powell.