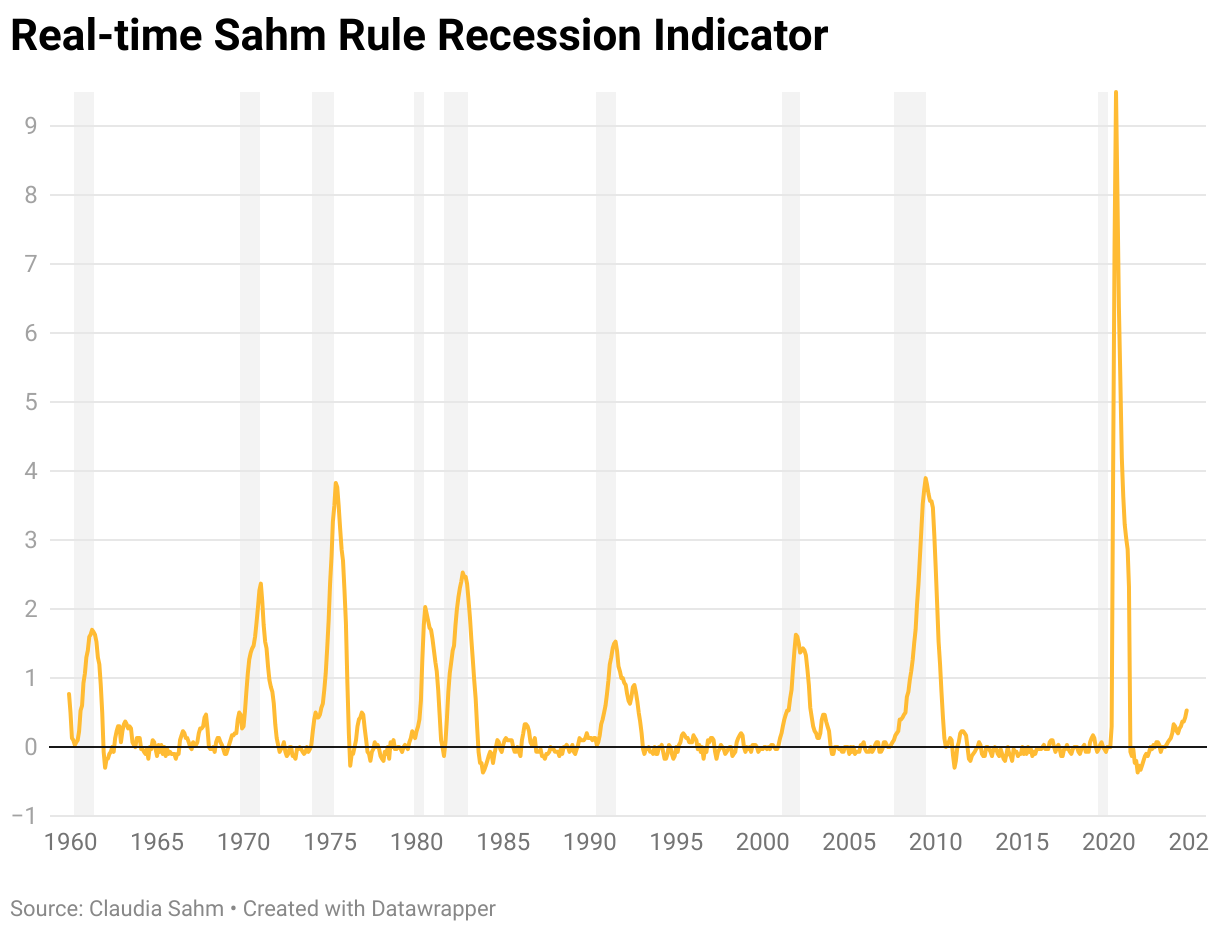

Recession fears have dominated headlines since Friday’s jobs report, where the rising unemployment rate triggered a recession indicator known as the Sahm Rule. The rule has an incredible track record of signaling the start of a recession, yet this time is an outlier, according to the rule’s creator.

The Sahm Rule states a recession in the U.S. has started when the three-month average of the unemployment rate crosses 0.5% or more relative to its low from the previous 12 months. July’s surprise unemployment rate of 4.3% triggered the Sahm Rule with a 0.53% rise.

Asked point-blank whether the U.S. is in a recession, Claudia Sahm told Straight Arrow News, “No, we are not.”

It’s not a recession and yet the risks are there because we do have these increases in the unemployment rate.

Claudia Sahm, Chief Economist, New Century Advisors

The following transcript has been edited for length and clarity. Watch the full interview in the video above.

Claudia Sahm: We should be concerned that [the unemployment rate] has been rising over the past year. And this is not just about hitting a particular level, or in July, we saw a larger jump than we’ve seen. The Sahm Rule averages across months. It looks over a year-long period. So it’s trying to get this direction that we’re headed and it’s not a good direction.

Now there are some very specific reasons, very special reasons that the Sahm Rule right now looks more ominous than it is. And the first thing we can say about, “we’re not in a recession,” is anytime we make a pronouncement like that, we should look around.

And in fact, broadly speaking, this economy is still growing and a recession means that it’s contracting, right? So we still see consumer spending, we’re adding jobs, industrial production. It’s slowed down, it’s not growing as fast, but we’re still growing. So that’s not a recession – right now.

So what’s going on with the unemployment rate? So there’s the bad reason unemployment rate goes up is there’s less demand for workers, it gets harder to find jobs. Hiring rates have come down a lot. It is a lot harder if you’re on the outside trying to find a job right now. So the unemployment rate has gone up for a bad reason. It does that in recessions.

The unemployment right now is also going up for one of the good reasons. So we have had more people join the workforce who weren’t working before. In particular, there was a big increase in immigration. And that was so important for solving the labor shortages that we’ve been suffering through. And yet, it takes time to adjust. I mean, that should be the theme of this cycle since the pandemic, that big messy changes take time and it’s painful.

It can make it really hard to read where the economy is, but right now we have people who’ve come in, and for some of them, it’s just going to take time for them to find jobs. And in that period, the unemployment rate will go up. Once they find the jobs, it can come back down. And frankly, people coming in to work, that’s a good sign for keeping the economy growing because there are more workers. That extra piece of unemployment rate increase looks bad but actually, it’s probably not.

I can say, looking broadly, what we know about the economy, we’re not in a recession. I mean, it’s never time to panic, but it’s also not recession time either. So it’s not a recession and yet the risks are there because we do have these increases in the unemployment rate that are of the more problematic kind, we just don’t know exactly how much.

Simone Del Rosario: When you created this rule, it was so policymakers could act on signs of a recession. Looking at what’s happening right now, there’s obviously a major movement happening with unemployment. What’s the remedy?

Claudia Sahm: There is a very clear policy lever out there to be pulled and that is the Federal Reserve beginning to reduce interest rates. And that’s the most straightforward one at this point. And the Fed has told us they are pointed at doing that.

Before we found out about July’s employment report, that’s the path they were on. Seeing that there is probably more weakness or at least more slowing in the labor market than we had previously thought, that probably means that they can get going in September, and maybe even cut interest rates more quickly than they had expected.

And it’s important that they have that lever to pull. It’s so important that we’re still in a position of strength. We’re not in a recession, we are still growing, there’s a lot of good things in U.S. economy.

The direction is not good, right? We don’t need to soften or weaken more than we have and that’s kind of where we’re pointed. And the realization that the Fed has been putting pressure on the economy to slow it down and for them to say, “Okay, we don’t need to slow it down anymore,” and reduce risk, that is the release valve to this that can get us to a good place.

That we just kind of settle into the jobs catch-up, we keep growing, we stay away from the recession. That’s the path. And you can tell the story and the path is there. It’s just anytime you get close to these real risky places in the economy, like a recession, you have to be careful because the people can get scared, markets can react. Things can unfold in unpredictable ways. So I think people should have their guard up more than a typical time and yet, there’s still a path to this all being just fine.

Simone Del Rosario: Are you concerned about a near-term recession or are you confident that when the Fed pulls that lever, the risk is over?

Claudia Sahm: I’m a macroeconomist. I’m always concerned. I devoted much of my career to studying recessions and how to fight them. And so I think it’s a risk that we should always be aware of, or at least policymakers should certainly be aware of. It is not my base case.

And again, I don’t want to make light of the Sahm Rule. The pattern I identified, there are other similar people looking at labor market conditions, it’s not like I’m the only one who’s pointed to weakness right now.

It does have a really strong track record and I don’t want to dismiss it out of hand. Something is happening and I don’t want to just write off any of the bad signs because now would be the time to act on them. Given all that, I think the risks are there. They’re not overwhelming. And because we’re still in a position of relative strength, that gives us a real leg up in terms of like what happens over the next three months, six months, 12 months.

Simone Del Rosario: Did the Fed make a mistake last week by not cutting?

Claudia Sahm: I have made the argument for much of this year that the Federal Reserve should begin to gradually lower interest rates, that inflation was coming down. Yes, the beginning of the year was a little rough. We’re also learning that we probably got head-faked by some of that data. We might be getting head-faked by some of the employment data now. It might not be as bad as it looks, right? But there was definitely a case, inflation is coming down, the Federal Reserve should get out of the way.

I had said last week they should start gradually reducing rates because it would be so much better to gradually reduce interest rates, watch the effects on the economy, because there are many question marks. We don’t know exactly how this amount of interest rate cuts translates into that amount of spending. So just to kind of watch and see what the economy does.

They are in a position now where if things continue to slow, the Fed may need to decrease interest rates more quickly. And at any time, and we’ve seen in the last few days, it can be pretty disruptive.

Hindsight’s 20-20. I think they could have been the winner last week if they had gone ahead with a cut, but you don’t get to go back and redo. I firmly believe they will assess the situation and take the steps necessary. It takes time for their tools to work so they do need to get going. But it’s not like all is lost. They’re going to have to probably play some catch up and they won’t get to do the victory lap.

Simone Del Rosario: The Fed is finding itself back in a position that it was when it started the hiking campaign, which was that it started hiking too late and then they were doing massive hikes. There’s all this talk now about how much more they may have to cut in September and beyond. Do you think that’s overblown?

Claudia Sahm: This cycle was always going to be messy. This has been a very hard-to-read economy. If you think about it, 2022, the Fed went really fast. They raised interest rates really quickly. There were a lot of concerns that we were going to be in a recession, that that was going to be part of what we had to have happen to get inflation down because it had gone up. Well, in fact, two years later, there has been no recession and we had a big disinflation.

It was not pretty in terms of how you would necessarily want the policy to roll out, but things worked out relatively well. So just because it doesn’t have this elegant, gradual cuts, it’s about getting the job done.

It clearly creates strain on families and businesses when they see the stock market, big numbers moving and what comes next. Fear can take on a life of its own and that is something that lives around the edges and in the middle of a recession. So you don’t want to treat those dynamics lightly, but we’ve dealt with a very uncertain, hard-to-read world for the last four and a half years. So we’re not done with the drama.

It was a missed opportunity by the Fed. At least that’s what it looks like today. We’ll get inflation data next week, maybe it doesn’t. But it looks like that was a missed opportunity, but there are so many more opportunities ahead of them to do good policy.