Economy may reel from hurricanes for 6+ months, Fed president says

Recovery efforts for Hurricane Helene are just getting started in the southeastern U.S., as Hurricane Milton makes landfall in Florida. The back-to-back disasters less than two weeks apart will have a lasting impact on the economy, Atlanta Federal Reserve Bank President Raphael Bostic warned during the week of Oct. 6.

Bostic said hurricane season impacts could evolve over the next six months or more and is something the Fed will closely track. As Milton’s path becomes more clear, damage estimates range from tens to more than $100 billion in losses. Private insured losses from Helene are around $8 billion to $14 billion, Moody’s estimates.

“Hurricane Helene is by far the most impactful event of the current 2024 hurricane season thus far, though this may quickly change with Major Hurricane Milton due to impact Florida in the coming days,” Moody’s Chief Risk Modeling Officer Mohsen Rahnama said.

“The hurricane is going to have a substantial effect on numbers coming out of the entire Southeast. We’re going to see a very large number of people who are temporarily laid off,” Harris said. “It’s hard to know exactly how long that’s going to last…The swath of the hurricane [Helene] was quite broad, and it hit a lot of population centers. So I think that is going to have a meaningful effect.”

Supply chain shocks are also expected post-hurricanes, especially with food, medicine and gas, as people rush for supplies. The storms hinder transportation routes which bottleneck delivering goods. In addition, Milton has the potential to damage major port infrastructure in Tampa and hinder trade routes nationally and internationally.

“When we think about a huge, horrific natural disaster with a huge human toll, we tend to focus solely on the negative sides of the economic impact – and for obvious reasons,” RiverFront Investment Group Chief Investment Strategist Chris Konstantinos told Straight Arrow News. “The cold, hard economic fact is [there are] gives and takes of what happens after a catastrophe like this. There are often two sides of it.”

“There’s going to be a huge amount of infrastructure spend,” Konstantinos added. “And so for companies, industry sectors that are construction related, sometimes these things can actually be a huge stimulus of sorts in those areas. And that may, at least regionally, actually increase some of the manufacturing data that we’re seeing.”

Konstantinos also said despite massive insured losses in the short term, insurance companies can benefit from major storms in the long run because they can lock in rate hikes. In Florida, home insurance rates are already the highest in the nation, with homeowners paying an average of about $1,000 per month for coverage that does not include flood insurance.

Inflation cools for sixth month in September but food and shelter stay hot

Consumer price inflation cooled for the sixth straight month in September 2024, coming in at 2.4% annually. Monthly prices rose 0.2% from August, according to data released by the Bureau of Labor Statistics Thursday, Oct. 10.

Core inflation, which removes more volatile food and energy prices, rose 3.3% annually and 0.3% compared to August. September’s report came in just a tick higher than expectations for the month.

Shelter, which has been the main driver of core inflation, went up 0.2% compared to August but is still up 4.9% year-over-year. Annual shelter inflation fell from 5.2% in August. Shelter price increases are still responsible for 65% of the yearly rise in core prices.

Together, shelter and food account for 75% of all inflation for the month.

The energy index fell 6.8% on an annual basis and 1.9% compared to August. That drop was driven by energy commodity prices, which are down 15.3% annually.

The price of new vehicles fell 1.3% while used vehicles fell 5.1% annually. Vehicle inflation was a major driver of inflation in recent years.

September’s inflation report will further inform the Federal Reserve’s next move in November after lowering its benchmark interest rate by 50 bps in September.

Analysts expect the central bank will make an additional 25 bps cut at the November Federal Open Market Committee meeting, which starts the day after the election.

The U.S. economy added far more jobs than anticipated in September and the unemployment rate ticked down to 4.1%. The U.S. added 254,000 jobs in September when economists expected around 150,000. In August, preliminary data showed 142,000 jobs added and 4.2% unemployment.

Markets convinced Fed will cut by 25bps after ‘very, very good’ jobs report

The next Federal Reserve rate decision may still be one month away, but traders are increasingly confident the Fed will cut by 25 basis points in November after seeing September’s jobs report. In new data out Friday, Oct. 4, the Bureau of Labor Statistics reported the U.S. economy added a surprise 254,000 jobs in September, 104,000 jobs more than economists anticipated, while the unemployment rate lowered to 4.1%.

The Fed cut its benchmark interest rate for the first time in four years in September. After seeing inflation slow closer to its 2% target and unemployment on the rise, Fed Chair Jerome Powell declared, “The time has come for policy to adjust.”

The declaration followed a weak July jobs report, showing unemployment rising to 4.3% and employers adding 114,000 jobs, much lower than the 12-month average.

In the latest data, the BLS revised up July’s data to 144,000 jobs added. The Bureau also revised August’s numbers up to 159,000 from 142,000.

“We were all sort of wringing our hands, and we thought the labor market was a lot weaker than we had expected,” former Acting and Deputy Labor Secretary Seth Harris told Straight Arrow News of July’s jobs report. “And of course, after this survey was taken, the Federal Reserve cut interest rates by 50 basis points, which is intended to strengthen the labor market.

“And then it turns out that, from this report, the labor market actually was a little bit stronger than we thought it was,” Harris continued. “Now, that’s not to say the Federal Reserve got it wrong. I don’t think they got it wrong. I have been calling for rate cuts for about six months now…But what this tells us is the labor market is very resilient. It is still quite strong. It is doing well.”

Harris, who is now a distinguished professor of practice at Northeastern University and a senior fellow at the Burnes Center, said he still believes the Fed should move forward with a 25-basis-point cut at their next meeting in November.

The market agrees.

In the 15 minutes following the release of September’s jobs data, the probability of a 25-basis-point cut in November went from 68% to 87%, according to CME FedWatch. Within two hours of the data release, that skyrocketed to 97%.

“I just think 25 basis points makes a lot of sense,” Harris said on Straight Arrow News’ live broadcast following the jobs report. “There’s some volatility in the labor market. That is the big story here, is we thought things weren’t going so well [when] they were actually going moderately, not great. This is, I would say, a very, very good number.”

“At the end of the day, they’re also trying to set a tone for the economy. Twenty-five basis points is a gentle nudge that we’re moving towards growth: Everybody loosen up a little bit. Start spending, start hiring, start moving a little bit more, not too fast, but a little bit more,” he said of the Fed’s desired rate-cut messaging.

September surprise: US adds 254,000 jobs, unemployment dips to 4.1%

The U.S. economy added far more jobs than anticipated in September while the unemployment rate ticked down to 4.1%. According to the latest data from the Bureau of Labor Statistics (BLS), the U.S. added 254,000 jobs in September when economists expected around 150,000. In August, preliminary data showed 142,000 jobs added and 4.2% unemployment.

With the release on Friday, Oct. 4, the BLS revised July’s numbers up by 55,000 to 144,000 jobs added for the month. It also revised up August’s numbers by 17,000 jobs, from 142,000 to 159,000 jobs added.

In total, jobs added in July and August are 72,000 more than previously reported by the Labor Department.

The latest jobs report comes less than a month after the Federal Reserve lowered its benchmark interest rate by 50 basis points. The U.S. central bank has a dual mandate to maintain stable prices and reach full employment.

This stronger-than-anticipated report will put the Fed’s November meeting in focus, where it is anticipated it will cut rates again by 25 bps.

The Bureau of Labor Statistics said the number of people not working who want a job is at 5.7 million. Construction employment continues to trend up, adding 25,000 jobs in September. The construction sector has consistently grown over the last 12 months, adding an average of 19,000 jobs per month.

Jobs in food services and drinking establishments rose by 69,000 in September, considerably above the 12-month average of 14,000 per month. This sector contained the largest increase in jobs for the month.

Health care added 45,000 new jobs, which is below the average monthly gain of 57,000 over the last 12 months.

The latest jobs report comes amid two large labor disputes.

Powell says Federal Reserve is in no ‘hurry to cut rates quickly’

Experts say the greatest threat to the economy in the next year isn’t the upcoming election or even conflict in the Middle East or Ukraine. More professional forecasters say a monetary policy mistake by the Federal Reserve poses the greatest downside risk.

This month, the Federal Reserve adjusted its policy rate for the first time in 14 months. The Fed cut its benchmark interest rate by 50 basis points in a supersized kickoff to the rate-cutting cycle. But in a speech Monday, Sept. 30 in Nashville, Fed Chair Jerome Powell essentially said not to read too much into the size of that first cut.

“This is not a committee that feels like it’s in a hurry to cut rates quickly. It’s a committee that wants to be guided,” Powell said. “Ultimately, we will be guided by the incoming data, and if the economy slows more than we expect, then we can cut faster. If it slows less than we expect, we can cut slower. And that’s really what’s going to decide it.”

We’re recalibrating policy to maintain the strength in the economy, not because of weakness in the economy.

Federal Reserve Chair Jerome Powell

The Fed’s goal is a soft landing, where they raise rates high enough to bring down inflation without triggering a recession. So far, they’ve reached the rate-cut part of the equation without a recorded recession.

“Our design overall is to achieve disinflation down to 2% without the kind of painful increase in unemployment that has often come with these inflation processes,” Powell said during the National Association for Business Economics annual meeting. “That’s been our goal all along. We’ve made progress toward it. We haven’t completed that task.”

The Fed’s preferred inflation gauge is down to 2.2%, a hair above its 2% target, while core inflation is higher at 2.7%. Meanwhile, the unemployment rate climbed to 4.2% from the 3.4% low hit in January and April 2023.

Federal Reserve board members and bank presidents project unemployment will rise to 4.4% by the end of this year and next, while core inflation won’t hit the 2% target until 2026.

While unemployment is higher than the modern-era lows experienced not too long ago, Powell rebuffed worries about the weakening labor market.

“Just take the current situation,” he said. “What you see is solid growth in the economy and what you see is a solid labor market. So in a way, the measures we’re taking now are really due to the fact that our stance is due to be recalibrated, but at a time when the economy is in solid condition, that’s what we’re doing. We’re recalibrating policy to maintain the strength in the economy, not because of weakness in the economy.”

The Fed will meet two more times this year, with its next 2-day meeting right after the election.

Right now, markets are leaning more toward a 25-basis-point cut rather than a 50-basis-point cut in November, according to CME’s FedWatch. Assuming those in the 25-basis-point camp are correct, that would bring the target range down to 4.5% to 4.75%.

Traders are then projecting the rate will drop down to between 4% and 4.25% following the December meeting, which would equate to a 50-basis-point cut. That’s higher than the 4.4% the Fed itself is projecting.

Does Fed rate cut plus falling mortgage rates equal more affordable housing?

Falling interest rates may pique the interest of prospective homebuyers but experts don’t necessarily think it is going to loosen the market anytime soon. The rate for a 30-year fixed mortgage averaged 6.09% for the week, according to Freddie Mac. The dip comes as the Federal Reserve cut its benchmark interest rate by 50 basis points on Wednesday, Sept. 18.

Mortgage rates have been slowly declining since hitting a 23-year high of 7.79% in October 2023. Though rates may still seem pretty high, every percentage point makes an impact. For every one percentage point mortgage rates increase, buying power lowers by 10%.

At the same time rising mortgage rates decreased buying power, housing prices skyrocketed. Even with recently falling mortgage rates in anticipation of the Fed cutting its key rate, the housing market has barely budged.

Existing home sales fell 2.5% in August, according to a release from the National Association of Realtors.

This transcript has been edited for length and clarity. Watch the full interview in the video above.

Simone Del Rosario: Homeowner hopefuls have been putting off plans to buy for years. Are these lower rates going to be the entrance point they’re looking for?

Selma Hepp: I think the lower mortgage rates are certainly helping. Every time we saw mortgage rates come down, it did help spur some buyer demand. For example, when you think about what happened after the Fed meeting last December, mortgage rates came down. That certainly spurred housing market demand; same thing the year prior.

So whenever we move closer to 6% and further away from 7% and even come down to the 5% range, it does help with affordability. It helps with a buyer’s budget and it brings back that demand that we desperately have been needing in the housing market.

Simone Del Rosario: Is it possible that more affordable mortgage rates could actually drive up housing prices since more buyers would be trying to enter the market?

Selma Hepp: Yeah, that’s a question that keeps coming up because everybody’s worried that there’s so much pent up demand and not enough supply, meaning that as soon as mortgage rates come down, you’ll see more buyers coming in and pushing those prices higher. That’s certainly a possibility, but what we did see over the course of this year is more inventory of existing homes for sale, and that has helped put a lid on home price appreciation.

And the other thing is, when you think about mortgage rates further coming down, it’s going to unlock some of that inventory that’s been locked in because the difference was so high between where people locked in and where mortgage rates were.

So with that spread coming lower, I think we’re going to see unlocking of some of that inventory, so the balance between buyers and sellers is going to be better, and it’s going to keep the lid again on the rate of home price appreciation. So we certainly hope for that going forward.

Simone Del Rosario: For sellers looking at the market right now, when would be an optimal time for sellers to enter the market?

Selma Hepp: That’s usually very individual decision. It depends on how long you’ve owned the home. Are you moving to another place where home prices are more affordable or not; are you staying in the area? And it depends also, on what your family situation is.

A lot of time sellers are driven by a change in family status. So they are either selling because they need a bigger home or there is a divorce situation, or maybe somebody is no longer around, and so that’s usually what drives sales.

That’s the most frequent reason for sales, but sometimes lower mortgage rates are helping. They do help sellers sort of feel better about their next purchase because it’s more affordable again. And I think definitely with mortgage rates coming down, it’s going to help with that sense of, ‘How much am I giving up to buy my new home?’ So yeah, I think it will help the number of sellers in the market as well.

Simone Del Rosario: Yes, selling a home is an individual decision and has to do with your personal life. But what we’ve seen over the past couple of years is people holding onto their low interest mortgage rates and not moving on to the next home when they typically would.

So this could unleash sellers, but at the same time, I believe the sellers would want to have the best price they can get for their house since they’ve waited so long to be able to sell it.

Selma Hepp: That’s often an interesting dilemma because you want the most you can get for your home, but then you also think about, with next home that you’re purchasing, that next seller is gonna want for the most for their home as well.

That’s always a dilemma that sellers find themselves in, but you’re absolutely right in terms of length of tenure for sellers. Over the course of the last couple of decades, we’ve seen people staying in their home longer and longer because homes have become increasingly more unaffordable and there are fewer homes available for sale.

So oftentimes what I hear sellers say is, ‘I do want to sell. I do want to move, but where am I going to move? There’s no inventory. There’s not something that fits what I’m looking for.’ And so they just end up staying put.

Simone Del Rosario: Obviously, these mortgage rates have been a large part of people’s decision-making process. But as you just pointed out, that’s not the only thing that is stalling the housing market. What are the other things that are making the housing market more sticky?

Selma Hepp: Affordability is the biggest one. But affordability, the lack of affordability, comes from the fact that we’ve under built for so long, particularly first-time or entry-level homes. So when people are trying to think about their first home or thinking about moving to another home, there are fewer homes to choose from. So that’s holding people back a lot.

We definitely saw that. For example, mortgage rates came down in early spring of 2023 and we saw a burst of buyers coming into the market, but there were not enough homes for sale. And that’s when home prices surged again and we saw significantly more appreciation in the market because of that imbalance.

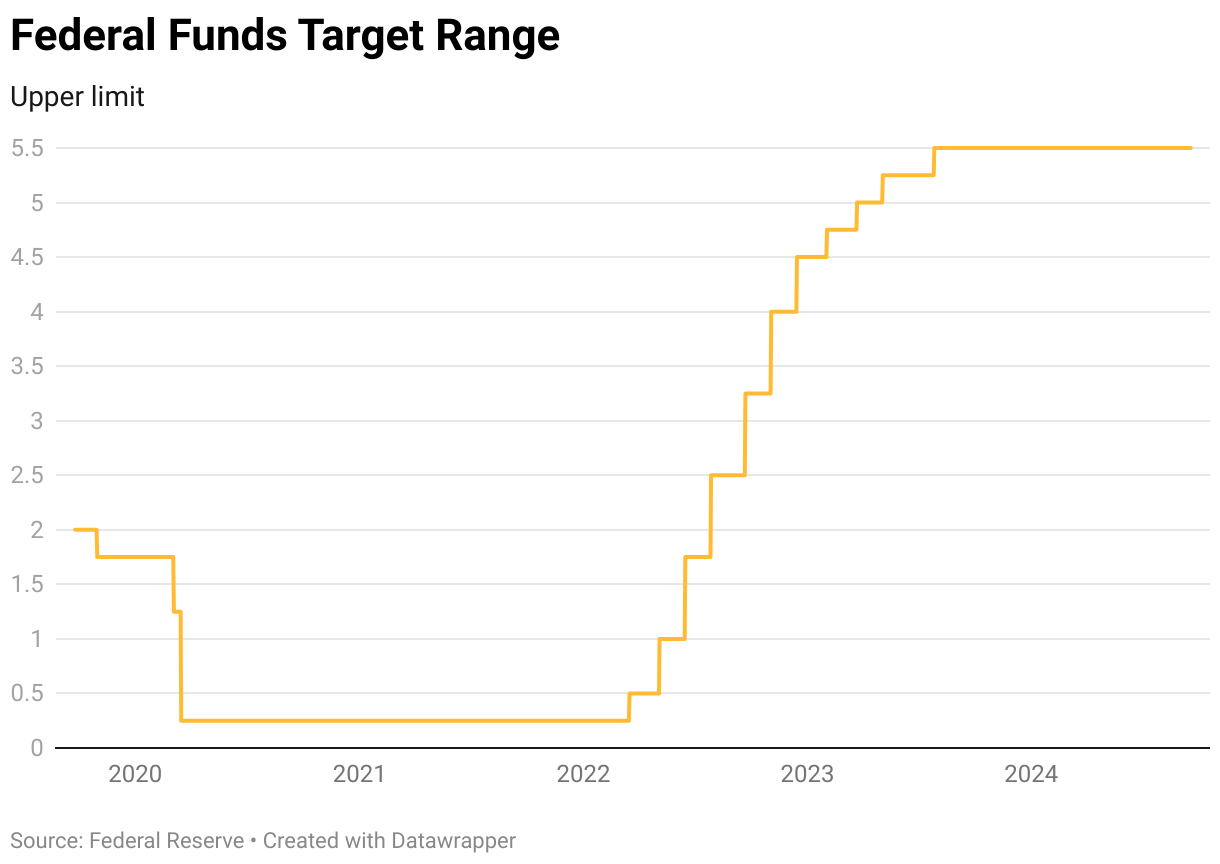

The federal funds rate now sits between 4.75%-5%, down from 5.25%-5.5%. This marks the first rate cut in four years after inflation spiked amid the COVID-19 pandemic.

“Recent indicators suggest that economic activity has continued to expand at a solid pace,” The Federal Open Markets Committee said in a statement. “Job gains have slowed, and the unemployment rate has moved up but remains low. Inflation has made further progress toward the Committee’s 2% objective but remains somewhat elevated.”

Inflation cooled for the fifth straight month in August at 2.5%, inching closer to the Federal Reserve’s target of 2%. But core prices, which strip out food and energy, stayed stagnant at 3.2%.

“In considering additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks,” the statement read. “The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2% objective.”

The S&P 500, NASDAQ and Dow notched gains in immediate response to news of the rate cut.

The Federal Reserve has a dual mandate of full employment and price stability. To keep those numbers in line with a strong economy, they use tools like adjusting the federal funds rate, which is the overnight lending rate for banks but in a downstream way affects interest rates on everything from mortgages to car loans.

Hezbollah blames Israel for deadly pager explosions

Hezbollah is blaming Israel after pagers used by the militant group exploded killing at least nine people and injuring thousands. And former President Donald Trump holds his first campaign event since the second apparent assassination attempt on his life. These stories and more highlight your Unbiased Updates for Wednesday, Sept. 18, 2024.

Hezbollah blames Israel for deadly pager explosions

Multiple explosions in Lebanon have killed at least nine people and left nearly 3,000 injured. Explosives inside pagers used by the militant group Hezbollah were set off Tuesday afternoon, Sept. 17.

The Iran-backed group blames Israel for the attack. Hezbollah said an 8-year-old was among those killed and Iran’s envoy to Beirut was among the injured.

Sources told Reuters Israel’s Mossad spy agency had planted the explosives inside 5,000 pagers. An American source and other officials confirmed to the New York Times that Israel was behind the operation.

The pagers appeared to be from Taiwan-based Gold Apollo. In a statement released Wednesday, Sept. 18, Gold Apollo said they were manufactured by another company based in Budapest that was authorized to use Gold Appollo’s brand.

Hezbollah fighters have been using pagers to bypass Israeli location-tracking following a warning by group leaders earlier this year saying cell phones were more dangerous than Israeli spies.

Hezbollah has vowed to retaliate against Israel.

Hezbollah and Israel began exchanging strikes shortly after Hamas’ deadly terrorist attack on Israel on October 7, 2023. Tuesday’s blasts add to the growing concern over a larger war in the Middle East.

Secretary of State of Antony Blinken will be in Egypt Wednesday to work on securing a cease-fire agreement to put an end to the conflict between Israel and Hamas and see the release of the hostages who remain in Gaza.

Trump, Harris both use assassination attempt to highlight policy proposals

Former President Donald Trump was back on the campaign trail Tuesday, holding his first event since the second apparent attempt on his life over the weekend. During a town hall in Flint, Michigan Trump told Arkansas Gov. Sarah Huckabee Sanders the assassination attempts are proof his policy proposals are powerful.

“It’s a dangerous business however, being president,” Trump said. “It’s a little bit dangerous. It’s, you know, they think racecar driving is dangerous. No. They think bull-riding, that’s pretty scary, right? No, this is a dangerous business and we have to keep it safe.”

He later added, “You know, only consequential presidents get shot at.”

Trump also said both President Joe Biden and, his opponent in the 2024 presidential race, Vice President Kamala Harris called him after the assassination attempt, saying it was “very nice” and he appreciated it.

“Not everybody has Secret Service,” Harris said, “and there are far too many people in our country right now who are not feeling safe. I mean, I look at Project 2025 and I look at the ‘don’t say gay laws’ coming out of Florida. Members of the LGBTQ community don’t feel safe right now. Immigrants or people with an immigrant background don’t feel safe right now. Women don’t feel safe right now.”

Both candidates are focusing on swing areas that could decide the election, which is expected to be a close one.

Trump is set to campaign in New York, Washington, D.C., and North Carolina this week. Harris will also stop in Washington as well as Michigan and Wisconsin in the coming days.

Speaker Johnson to bring spending bill up for vote

House Speaker Mike Johnson is expected to put his short-term spending plan up for a vote Wednesday, though there are signs it will not get the GOP support needed to pass.

Johnson previously pulled a stopgap bill that was coupled with the SAVE Act — which would require proof of citizenship to vote in federal elections — after it became clear it was unlikely to get enough Republican approval to pass. House Democrats also opposed the plan, though it would keep the government funded through most of March.

Congress has until the end of September to pass at least a temporary measure keeping the government open, otherwise a shutdown looms Oct. 1.

Federal Reserve expected to cut interest rates for first time since 2020

The Federal Reserve is expected to cut interest rates for the first time since 2020. However, it’s not yet known by how much.

Straight Arrow News Business Correspondent Simone Del Rosario has a closer look here.

Sean ‘Diddy’ Combs denied bail in racketeering, sex trafficking case

Sean “Diddy” Combs has been denied bail and will remain in custody as he faces serious charges, including sex trafficking, racketeering, conspiracy, and transportation to engage in prostitution.

Authorities say Combs will be held by himself at a “special housing unit” in a detention center in Brooklyn.

In a federal courtroom in New York City on Tuesday, Combs pleaded not guilty to the charges he’s facing. Prosecutors allege that Combs used his business empire to force women into engaging in sexual acts with professional sex workers and himself.

Prosecutors allege that in late 2023, following public accusations of these crimes, Combs and his associates attempted to pressure victims into silence through bribery.

If convicted on all charges, Combs faces decades in prison.

Billie Jean King to make history as Congressional Gold Medal recipient

Tennis hall of famer Billie Jean King is being recognized with a prestigious Congressional Gold Medal for her efforts on and off the tennis court.

The measure had already passed the Senate and on Tuesday night, it passed the House, making Billie Jean King the first individual female athlete to ever receive the congressional honor.

🚨 History made! 🚨 The House just passed my bipartisan, bicameral bill to award my friend, @BillieJeanKing, legendary athlete, and ardent advocate, the Congressional Gold Medal, making her the first female athlete to ever receive this honor—yet another iconic trailblazing moment… pic.twitter.com/kbkkym0aVN

“Mister speaker, it is now time to enshrine Billie Jean King’s legacy as not only a champion of tennis, but a champion of equality whose impact will continue to inspire women and girls and people across America and across the world,” Rep. Brian Fitzpatrick (R-PA) said before the measure was passed.

After receiving the news that she would receive the Congressional Gold Medal, King took to X to say, “Thank you. I am deeply humbled and honored.”

Markets are betting on a supersized rate cut. Why the Fed may disappoint.

Markets are increasingly betting the Federal Reserve will make a supersized rate cut at this week’s meeting. There are two camps: Those who believe the Fed will cut interest rates by 25 basis points and those who believe the Fed will double up to 50 basis points.

A week ago, 2 out of 3 futures traders were betting the Fed would do a 25 basis point cut, according to CME FedWatch.

But by the time the Fed started its two-day meeting the morning of Tuesday, Sept. 17, odds had switched. As of 10 a.m. ET, 2 out of 3 futures traders were betting on a jumbo cut to kick off this rate-cut cycle.

“The market is thinking this because the market is sniffing out some economic weakness,” Fed Guy and CIO of Monetary Macro Joseph Wang told Straight Arrow News. “They’re noticing that the unemployment rate has gone up. It seems like there are a lot of indicators that the Fed might be over-tightening, and so in order to get ahead of this, the Fed might want to do with a supersized cut. Now I’m not in that camp, because so far, what I hear from Fed speakers is that it’s more likely that the economy is normalizing.”

Wang is in the 25-basis-point camp, joined by former Fed adviser and QI Research CEO Danielle DiMartino Booth.

“They want to be measured and gradual,” DiMartino Booth told Straight Arrow News. “They want to be Greenspan-esque. [Former Fed Chair Alan] Greenspan had 17 25-basis-point rate hikes in a row. So it was a little bit different dynamic. It was a tightening campaign, but they want to be as measured. They want to be able to say, ‘We’re going to engineer a soft landing. We’re going to be taking interest rates down at a very slow pace.’”

When inflation started getting out of hand in 2022, the Fed began its rate-hike campaign to tighten monetary conditions and get people and businesses to spend less. It hoped the move would bring down prices.

The team hiked the Fed funds target range all the way to 5.5%. They’ve held it there for more than a year now. This is the highest the rate has been since early 2001.

But now inflation is much closer to the Fed’s 2% target, the unemployment rate is rising. Therefore, a soft landing is getting more elusive.

Markets are betting that the Fed funds rate will go down to below 3% by next summer. That would mean cutting 250 basis points in less than a year.

“The pricing in the market seems to be pretty aggressive,” Wang said. “From my perspective, I think there’s too much doom and gloom being priced in. My base case expectation is that rather than having a series of huge cuts that the market is assuming that we have, some steady 25 basis point cuts, and maybe the cut cycle ends, let’s say around 3.5%, rather than below 3%.”

Wherever it lands, Americans will see a change in what it costs to borrow money. In the same way as when the Fed was hiking rates and mortgage rates, auto loans and credit card interest rates soared, this time those interest rates will also go down.

In fact, it’s already happening. Ahead of Wednesday’s Fed cut, mortgage rates fell to levels not seen since early 2023. If the Fed cuts rates by 25 basis points following its meeting, that cut is likely priced into the current mortgage rates. But if they go jumbo-sized to 50 basis points, mortgage rates could go down even more.

Subscribe to the Straight Arrow News YouTube page and tune in Wednesday, Sept. 18, at 2:10 p.m. ET, where SAN will have a live report of the Fed’s final decision and comments from Fed Chair Jerome Powell.

Fed expected to slash rates by 25 bps in September. What’s next?

After the Wednesday, Sept. 11, inflation report came in on target, markets are even more confident the Federal Reserve will cut its rate by 25 basis points following its policy meeting next week. In August, Fed Chair Jerome Powell said it was time for policy to adjust after an “unmistakable” weakening in the labor market. But how much adjusting is coming down the pike after September?

The federal fund target range is a benchmark rate for lending. Since July 2023, the Federal Open Market Committee has held the range between 5.25% and 5.5%, its highest level in more than two decades.

Markets initially expected rate cuts to come much earlier in the year, but after inflation remained stickier than anticipated, September would mark the first rate cut since early 2020 after five straight months of cooling consumer price inflation.

If the Fed decides to cut in September, it will mark the beginning of a rate-cut cycle. After the Fed’s decision on Sept. 18, the committee will meet two more times in 2024, the two days after the November election and Dec. 17-18. For more on how much the Fed may cut this year and next, Straight Arrow News spoke with the Fed Guy Joseph Wang.

The following transcript is edited for length and clarity. Watch the full clip in the video above and catch the entire interview on Straight Arrow News’ YouTube page.

Joseph Wang: So the market is pricing in a very, very aggressive Fed cut cycle, so aggressive that the market is pricing by the end of next year, the overnight rate will be below 3%. So that’s from 5.5% today to below 3% next year.

Now that’s a very aggressive rate path, expected policy pricing by the market, and that seems to assume a significant deterioration in the economy.

Let’s look at the big picture, though. The most recent GDP statistics in the US were revised upwards from 2.8% annual growth rate to 3%, so the economy is actually growing fine. There’s really no indication that we would just suddenly go from 3% to a recession where we don’t grow, we shrink.

Jobs reports, again, slowing, but we’re still creating over 100,000 jobs a month. When we’re in a recession, we don’t create 100,000 jobs a month, we lose 100,000 jobs a month. And so the pricing in the market seems to be pretty aggressive from my perspective, I think there’s too much doom and gloom being priced in.

My base case expectation is that rather than having a series of huge cuts that the market is assuming that we have, [we have] some steady 25-basis-point cuts, and maybe the cut cycle ends, let’s say around 3.5%, rather than below 3%. I say this because, by all indications, the economy continues to have momentum and there’s a good case to be made that rather than falling into recession, we really are just normalizing now.

One other thing that I would mention is that something that’s happening today that hasn’t happened before is that we have tremendous amounts of fiscal spending. The government is expected to have a fiscal deficit of about a couple trillion dollars, basically forever, and when you have the government spending so much each year, that’s very supportive of demand. It’s upward pressure on inflation. It’s not a very good management of the currency, but it is supportive of demand.

And so when you have that kind of fiscal spending, I think that’s a good tailwind. Now, one other thing to keep in mind is that what happens in November could have very big implications for macro policy. We have two candidates with very, very different visions of the world. We also have to look at Congress to see whether or not they are able to carry out their different visions of the world.

So there’s a lot of uncertainty there. But based on what I see right now, the economy is still okay, and the rate cuts in the markets are too aggressive. We’ll have some, but it doesn’t seem like we would have so many, because it doesn’t seem like at the moment that we are tumbling into recession.