There’s a new term to describe this job market’s vibes

Despite a strong jobs report for November, the job market vibe is mixed. The number of Americans reporting they want a new job is at a 10-year high, but many feel they have nowhere to go.

Gallup is calling it the “Great Detachment,” years after the “Great Resignation” took hold. In workplaces around America, employees feel stuck.

“People are aware that it’s harder to find a job than it was a few years ago, and that if they have a job, their layoff risks are actually very low, so it’s worth holding tight, not worth jumping ship,” said Guy Berger, director of economic research at Burning Glass Institute. “Simultaneously with that, I think there’s some evidence people are much more frustrated in their current jobs.”

According to a recent Gallup poll, more than half of U.S. workers say they are watching for or actively seeking a new job, a 10-year high. Meanwhile, the share of people who report being “extremely satisfied” with their work is 18%, a 10-year low.

“I think until hiring starts picking up a little bit, which may happen next year, or at least stops falling, I think people are going to feel a little like, ‘I want to get out, I want to find something else, but I can’t,’” Berger said.

While employers may be relieved the age of high turnover is over, Gallup warns this period of detachment can come with productivity concerns and future talent loss. They say employees are more likely to resist or be indifferent to organizational changes.

An interesting thing happened when the “Great Resignation” kicked off. The connection employees felt to their workplace’s mission or purpose plunged, and there’s still no sign of recovery, Gallup data shows. Less than half of employees say they even know what’s expected of them at work. But still, employees are hanging on.

“There’s probably some chunk of people that are like, ‘You know what? My pay has gone up. I’m very happy at my job. I’m at low risk of layoffs … They might say this is a really good labor market,” Berger said. “And then you have people in the middle that have a job, they’re at low risk of being laid off, but might want something different. And there’s not a lot of stuff out there. And for them, this is a good, but not great, job market.”

“And that’s probably the biggest chunk of people out there. They’re not worried, but they would like something else, and there’s not something out there, and maybe they’re growing increasingly frustrated. As long as layoffs don’t pick up, they’re in a decent, cushy spot,” he continued.

And then there are people who are out of the labor force. The Labor Department says the unemployment rate is 4.2%. It’s historically on the lower side, though much higher than a year ago.

“The mix of unemployment has gotten a little worse,” Berger explained. “We have more people that are permanently laid off than we did before, and fewer people that are quitters.”

Berger said for those who can’t find a job, the market is more reminiscent of the early 2010s, when the Great Recession still had a grasp on the economy.

“And I think in some senses, maybe more isolating, because these people that are unfortunate enough to have been laid off and are having trouble getting hired, they keep hearing, ‘Oh, this is a good labor market, that employment rates are low, etc,’ and their experience is quite different,” Berger said.

X is worth 79% less than when Elon Musk bought it for $44 billion: Report

Elon Musk’s contention in 2022 that he and his fellow investors were overpaying when they bought the social media platform formerly known as Twitter seems to be spot on. Fidelity said the value of its investment in X dwindled by nearly 79%.

Asset managers at Fidelity’s Blue Chip Growth Fund say the value of its investment into X has fallen by 78.7% as of the end of August. The fund invested $19.66 million in the social media company in October 2022. By July of this year, it said its investment was worth $5.5 million. By the end of August, it valued the investment at $4.19 million, according to recent disclosures.

This isn’t the first time the value of the company has been called into question. In October of last year, X issued stock grants to employees at a price of $45 per share. That put the price at around $19 billion.

Meanwhile, the Wall Street Journal said the $13 billion Musk borrowed to buy the company has become the worst buyout situation for banks since the Great Recession.

When banks loan money for takeovers like this one, they typically sell the debt to other investors so they can collect fees instead of it sitting on their books. But banks haven’t been able to do that with the X debt without taking losses because it isn’t making money.

The Twitter loans have hung longer than similar deals in 2008-2009. Banks call loans stuck on their balance sheets “hung.”

While the Great Recession created more hung loans, banks were generally able to offload the debt within a year, something that hasn’t happened in the case of X, according to analysis from Pitchbook LCD.

Despite Musk saying in October 2022 that he and his other investors were “obviously overpaying for Twitter,” seven banks, including Morgan Stanley, Bank of America, and Barclays, still approved the loans.

But it’s not all downside for the banks involved. They’ve been able to rake in massive amounts of interest off the acquisition. Musk previously said he is paying $1.5 billion per year on those loans, which have significantly higher rates than other loans used for acquisitions.

‘Recession pop’: Can great music signal an economic downturn?

It’s tough to identify if the economy is in a recession. Economists toil over economic data to try to find the most accurate indicators. Gross domestic product and unemployment numbers are great data points, but what does the state of pop music tell us about economic conditions?

Traditionally, two consecutive quarters of negative growth is the preferred method to tell a recession took place. When it comes to unemployment, the Sahm Rule is triggered when the three-month moving average of the unemployment rate is half a percentage point above the 12-month low. The McKelvey Rule is essentially the same but is triggered when the unemployment rate is 0.3 percentage points above the 12-month low. The inverted yield curve, when short-term Treasury yields exceed long-term yields, is also a recession indicator.

Exploring Recession Pop: A Journey Through Music and Hardship * Recession Pop, characterized by its upbeat and escapist dance music, emerges during times of economic turmoil as a form of distraction and catharsis. * This phenomenon is not new, with historical examples dating back to the Great Depression and recurring during subsequent periods of hardship. Pre-Recession Examples: * Dance music as a form of escapism can be traced back to the Great Depression era, where swing and jazz provided solace amidst economic struggles. * In the UK, the Winter of Discontent in 1978/1979 saw the rise of ABBA’s albums, offering a similar escape during a period of social and economic unrest. The Great Recession (2000s): * The late 2000s Great Recession saw a surge in dance-pop music, offering a distraction from economic woes. * Artists like Black Eyed Peas, Rihanna, Katy Perry, and Lady Gaga dominated the charts with infectious hits. * Songs like Flo Rida’s “Club Can’t Handle Me” provided a sense of camaraderie and hope amid uncertainty, embodying the spirit of Recession Pop. * Dance music acts as a survival mechanism, providing a temporary reprieve from the harsh realities of the world. Post-Pandemic (2020s): * The COVID-19 pandemic brought about a resurgence of dance-pop and disco music, echoing the Recession Pop trend. * Artists like Dua Lipa, Doja Cat, and Beyoncé spearheaded this revival, offering upbeat and nostalgic tunes during difficult times. * Sample-heavy tracks and uplifting beats became prevalent, serving as a source of comfort and nostalgia for listeners. * Despite the challenging circumstances, the music industry continued to thrive, providing a beacon of light in dark times. * Recession Pop reflects the resilience of music as a form of escapism and catharsis during times of hardship. * Despite economic downturns and global crises, dance-pop music remains a source of joy and unity for listeners worldwide. * As we navigate through uncertain times, the enduring popularity of Recession Pop serves as a reminder of the power of music to uplift and inspire in the face of adversity. #JoesAlternativeHistory#RecessionPop#MusicHistory#GreatRecession#LadyGaga#2000sPop#BlackEyedPeas#BoomBoomPow#WinterOfDiscontent#GreatDepression#DuaLipa#Beyonce#DojaCat#ABBA#PopCulture#PopCultureHistory#recession

But then there is the notion that “pop music is brilliant” when the economy is about to face serious problems. That is where the idea of “recession pop” comes into play.

What is recession pop?

In short, recession pop is seen as the Top 40 hits that are released during an economic downturn. The most clear example was during the Great Recession.

“I would define recession pop from the years just leading up to the recession, so the end of 2007 probably at least through 2012,” Charlie Harding, an NYU Professor and co-host of the podcast “Switched on Pop,” said.

Meanwhile, Joe Bennett, a musicologist and professor at Berklee College of Music, said it’s a label that applies “to a particular body of work, which I would broadly describe as super cheerful dance floor bangers that came out sometime between 2008 and 2011.”

Super cheerful dance floor bangers that came out sometime between 2008 and 2011.

Musicologist Joe Bennett describing recession pop

Since it is not a particularly scientific indicator, Harding said the recession pop label could even go all the way into 2014 because “lots of people were still really feeling that recession well into the early 2010s.”

Is recession pop a real thing?

It’s hard to officially quantify whether pop music really reflects the economic times, but both Harding and Bennett said the interpretation is often up to the listener.

“You can find what we might say are reflective songs, where the dark times people are experiencing are indeed dealt with within the song lyric,” Bennett said. “And we might also find what you might call escapist songs. ‘What the heck, let’s party.’”

“So songwriters are not necessarily social commenters, but like all of us, everyone who creates popular culture, they are living in that culture at the time they are making the object and the market that is the pop music fans who are buying or streaming the single are also in that social context and liking what they like in the context that they’re in,” he continued.

“As much intention as a songwriter might have, whatever they might intend, the listener is going to take it and do what they want with it,” Harding added. “A great example of listeners completely misusing a song would be ‘Hey Ya’ by OutKast, which is one of the most requested songs at weddings, and yet the song is about relationships that never last.”

“The recession affected different people very differently,” Harding said. “If you lost your home, you’re gonna remember what that song is on the radio when you had to pack up and leave. It’s really different than maybe someone for whom their family got through it okay, and they’re just like, ‘I just love my recession pop bops.’”

The history of popular music is littered with songs known as “party anthems.” But the recession pop era may have had less economic-based reasons for those hits.

“I think there’s ways in which the music was great, and I think there’s other ways in which it feels a little bit reductive,” Harding told Straight Arrow News. “We’re talking about a period in which the digitization of music was fully taking over.”

Despite the idea that recession pop is specific to the Great Recession, Bennett points to music that came out amid the Great Depression to illustrate how music reflects the times.

“Bing Crosby’s ‘Brother Can You Spare a Dime?’: it was a big hit in the early ’30s, and that’s a song about a returning war veteran who’s homeless and looking for money,” he said. “In 1933, Ginger Rogers has a hit with ‘We’re in the Money.’ Is that sort of an ironic title? It’s certainly a very cheerful lyric. Maybe it’s a fantasy about having money, because a lot of people wouldn’t have in the U.S. in the early 30s.”

Nostalgia effect

With all the evidence to support the idea of recession pop, it’s hard to say one era’s music is better than another, which can make it a particularly difficult economic indicator to nail down.

“If recession pop is a nostalgic way of looking back and trying to make sense of this period of total dislocation and fragmentation, all the power to listeners to call this stuff recession pop, even if it just happened to be the upbeat, fun thing that was occurring at that time,” Harding said. “People are trying to make this connection to music that happened 10 to 15 years ago.”

There is good reason for music dubbed recession pop to be resonating with people in their 30s that may have nothing to do with the quality of the tunes or state of the economy.

“It fits with the general cycle of popular music nostalgia,” Bennett said.

Bennet added most people believe the best music was released when they were 17 years old.

“A lot of the psychology research into nostalgia suggests that it works on something like a 15-year cycle,” Bennet continued.

“It’s more of an after-the-fact analysis, which is a fun and useful way of creating playlists: being nostalgic, digging into our memory, perhaps making sense of an era that was really dark and challenging for people and making light of it after the fact,” Harding said.

Pop music today

While recession pop is likely just a label put on music after the fact, it gives us an opportunity to look at what makes a hit song and how that has changed in the last 15 years.

“I think what makes a great pop song is accessibility,” Bennett said. “Particularly if you’re releasing a single, you want it to appeal to millions of people.”

“It has to have an amazing concept,” Harding added. “[It] has to have a memorable hook, and it has to capture the zeitgeist.”

Harding likens making a great pop song to winning the lottery. Many wonder how some artists have been able to hit the jackpot over and over again. But what makes a great pop song has changed over time. Today, more and more records are being discovered on short-form video apps like TikTok and Instagram.

“TikTok is a much faster-moving medium so people need to grab their audience’s attention to stop them from vertically scrolling onto the next thing,” Bennett said of the app that broke artists like Lil’ Nas X. “As we know from TikTok, that sort of meme community will often seize on a particular part of the song, a particular audio excerpt, and use that to make its meme, its dance routine, whatever it is.”

But even though artists need to get to the hook quicker than ever before, Harding said they have more to say than ever before.

“There is this expectation that we are more giving of ourselves in our lyrics today,” Harding said. “And so I think of an artist like Charlie XCX, who, on ‘Brat,’ talked about how she wanted to write lyrics that were as if she was just texting a friend. And this is the album that has broken through for her, because some of these lyrics, they don’t have these perfect rhymes. They have the perfect imperfections.”

And there’s no bigger artist giving themselves to their music than Taylor Swift.

“I think on a lot of metrics, Taylor Swift is the biggest artist to have ever lived, in terms of the longevity of her career; the fact that she is what should be a late-stage career artist, and yet she is at her peak,” Harding said. “She has had multiple peaks that just keep getting bigger and bigger and bigger.”

Meanwhile, Bennett pointed out that Swift herself was not immune to the recession pop movement.

“Her two significant albums at that time would have been ‘Fearless,’ which came out in 2008 and then ‘Speak Now,’ which originally came out in 2010,” Bennett said. “And of course, both of those contain a whole bunch of songs in that vein: ‘Love Story,’ ‘You Belong with Me,’ ‘White Horse,’ ‘The Story of Us.’”

In the end, while there may not be a deliberate intention to make music that makes listeners feel good or sad during tough economic times, it’s clear music resonates with people and reminds them of those snapshots in time.

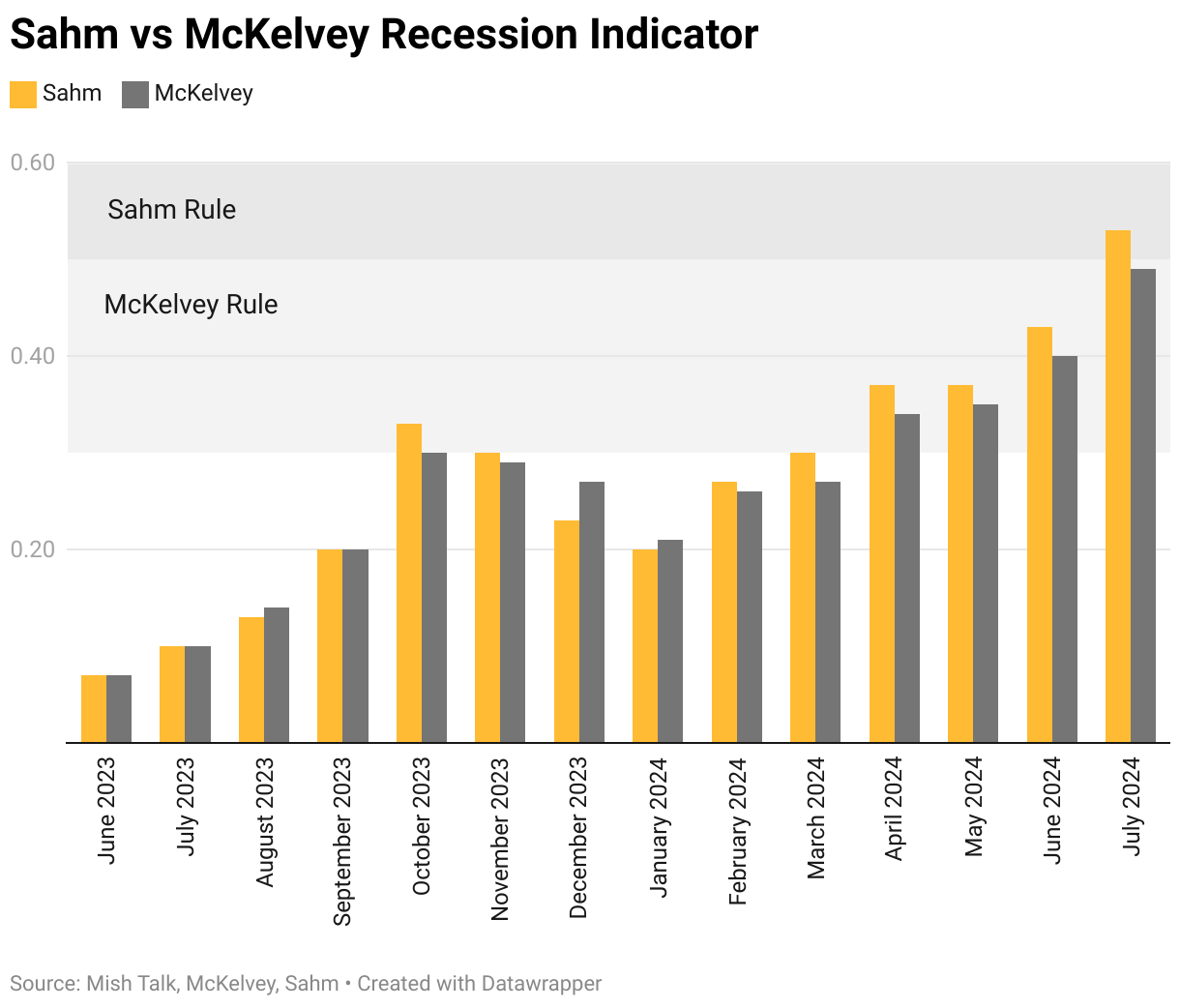

Here’s why this former Fed adviser says we are already in a recession

The creator of a recession indicator that was triggered this past week said her rule is broken this time around and there’s no recession right now. But not everyone agrees. In fact, a different recession indicator points to the U.S. having entered a recession in October of last year.

“We’re not in a recession,” Sahm Rule creator Claudia Sahm told Straight Arrow News. “It’s never time to panic, but it’s also not recession time either. So it’s not a recession. And yet the risks are there.”

Recessions are declared by the National Bureau of Economic Research in hindsight by looking at the economy’s growth over previous quarters. Recession indicators like Sahm’s look at rising unemployment rate trends for more immediate indications the country has entered a recession.

While Sahm’s rule was triggered by last week’s release of July’s jobs data, a different recession indicator was set off last October. In simple terms, the McKelvey Rule hits when the three-month average rise in unemployment hits 0.3 percentage points above the year’s low, compared to Sahm’s 0.5-percentage-point threshold.

The following transcript has been edited for length and clarity. Watch the full interview in the video above.

Danielle DiMartino Booth: I do think we’re in recession. Everything that we’ve seen from the Bureau of Labor Statistics with regards to the fourth quarter of 2023 indicates that they’re going to be revising into negative territory the final three months of 2023.

So that would stretch job losses from the third quarter of 2023 – when there were 192,000 jobs lost in the United States – that would stretch that into the fourth quarter and give us a six-month stretch of job losses upon revising the Bureau of Labor Statistics survey data with the hard data that we get from the Census Bureau, where companies are legally obligated once a quarter to report their headcount.

And that’s kind of the ultimate decision. That’s when the ink dries, if you will, on the payrolls data that we see the Bureau of Labor Statistics release.

Simone Del Rosario: So we’re looking at a recession that would have started in October of last year?

Danielle DiMartino Booth: I personally see the recession as having started in October 2023 because that’s the first time that the McKelvey Rule, which is less arduous than the Sahm Rule – and it doesn’t date back to 1948, it dates back to 1968 – but it has not missed a single recession since then.

Rather than a 0.5-percentage-point increase in the unemployment rate off of its lowest level in the prior 12 months, it is a 0.3-percentage-point increase in the unemployment rate over the prior 12-month period’s low.

Again, it has a spotless track record since 1968. It was triggered in October of 2023. The Bureau of Labor Statistics said that we lost 192,000 jobs in the three months ending Sept. 30, 2023. So the National Bureau of Economic Research could theoretically backdate it further, but again, the McKelvey Rule is what I’ve relied on.

The former chief economist at Goldman Sachs, he was interviewed by the Wall Street Journal in January 2008 when his rule was triggered, and he was asked the same question: ‘Well, your McKelvey Rule was triggered in December of 2007. Do you think we’re in recession?’ And he said, ‘Well, you know, my rule might be broken,’ basically.

But of course, the NBER did backdate that recession to December 2007 and the McKelvey Rule was not broken. Luckily, the Bloomberg Economics team agrees with me that recession, that job losses started in October 2023.

Simone Del Rosario: Why isn’t the Federal Reserve looking at these data points?

Danielle DiMartino Booth: I think the Fed is choosing to look the other way in this instance. There are some regulations that the Fed has been working on that could really define Chair Powell’s legacy – that would begin to regulate the private equities, the hedge funds, the BlackRocks of the world that are in some cases larger than banks if you consider the trillions of dollars that they have under management – and in order to push through with some of these regulations, he really does need higher-for-longer [rates] on his side.

He needs the higher-for-longer policy enough to go with what the Bureau of Labor Statistics first reports, even though we know that since January 2023, we’ve seen one downward revision after another to the data. It’s become systematic, in fact, the persistence with which we’ve seen downward revisions to what’s first reported. But again, I think [Fed Chair Jerome] Powell’s got his own reasons.

Simone Del Rosario: How do you square this idea that we could be in a recession right now with the GDP numbers that we’re seeing? The latest reading, the advance estimate, showed an annual growth rate of 2.8%.

Danielle DiMartino Booth: So we had 2-point-something percent in 2001 when it was first reported. Of course, it was another six quarters later that we revised it and found out that it was a negative number.

It takes magnitudes of the amount of time to get correct unemployment data, correct payrolls data. You can double the time that it takes to figure out what the actual GDP is that’s associated with that time frame.

If you find out that you’re 830,000 jobs shy of what you thought you were, which is what we found out in the third quarter of 2023 looking backward with hard data in hand, then you have to subsequently go back and back out. Well, 830,000 people were not actually working; 830,000 people were not actually producing the economic output that we thought we were. So you’ve got to back that out.

It takes a lot of time for the Bureau of Labor Statistics data to work its way into subsequent revisions for the Bureau of Economic Analysis data, for GDP.

It’s at inflection points. It’s when contractions become expansions, when expansions become contractions, that these big statistical agencies have trouble seeing the turning point, given their modeling.

But it wasn’t until 2018 that we saw the final GDP revision from the Great Recession that ended in June 2009. Again, the recession ended June 2009. We didn’t get the final revision for GDP for that recession until 2018.

Simone Del Rosario: On one hand, this can seem incredibly frustrating if people feel like we’re in a recession, they feel like the economy’s not good, and yet we continue to get, on the surface, economic releases that show a pretty strong economy. But that said, if, to your point, we are already in a recession, does that take some of the panic away since we’ve already been going through it, or is it going to get worse? What’s your read on that?

Danielle DiMartino Booth: Well, your average recession is 10 months long in the post-war era. So using that average length of time, we should theoretically be starting to recover and coming out of recession.

That being said, the Federal Reserve has waited now 12 months, now longer than 12 months, and the longer it waits, typically the deeper and longer the recession is as a result.

There have been some great studies that empirically demonstrate this. The period leading up to the Great Recession, 2007-2009, the Fed waited 15 months. It’s the longest the Fed’s ever waited.

So we’re just at the 12-month mark now. But it certainly looks like we’re going to get to the 14-month mark if it’s Sept. 18 that we can anticipate that first rate cut. So that’s about as long as the Fed has ever waited to provide relief in the form of the beginning of an easing cycle.

How will banks hold up against stress test that mimics 2008 financial crisis?

Doctors use stress tests to find out how well one’s heart works when pumping harder than normal. The Federal Reserve does the same for banks and this year’s health results will be released Wednesday, June 26, after markets close.

After the 2008 financial crisis, the Fed determined it was a good idea to test how banks would hold up in the face of a severe global recession. Now, the Fed runs these stress tests annually on the nation’s biggest banks.

In this year’s fictional scenario, the unemployment rate peaks at 10%, which is what it peaked at during the Great Recession. Housing prices fall 36% and commercial real estate prices tank 40%. The largest banks are also subject to hypothetical global market shocks. In all, the Fed stress-tested 32 banks this year.

Straight Arrow News interviewed former Fed adviser and founder and CEO of QI Research, Danielle DiMartino Booth, ahead of the stress test results.

The following has been edited for length and clarity. You can watch the interview in the video at the top of this page.

Simone Del Rosario: Why should the average American care about how banks perform on these tests?

Danielle DiMartino Booth: I think what’s critical is to not have too short of a memory. I realized that 2008, 2009, at this point we’re talking almost 20 years ago. But it was very disruptive to the U.S. economy when the banks in the country were lining up like dominoes, one after the other, and effectively failing and requiring bailouts of some semblance. It was extremely disruptive to the economy.

Credit to households and businesses was abruptly cut off. That is going to be a huge impairment whether you’re running a business or if you’re trying to buy a car. We’ve seen that a hacking exercise that really run amok with the nation’s automobile dealerships was enough to kind of bring auto to its knees.

A similar set of circumstances can certainly unfold if banks end up being weaker than what we think they are and lending comes to a halt.

Simone Del Rosario: How do you think banks are going to fare when we get the results on Wednesday?

Danielle DiMartino Booth: We really are talking about the nation’s 32 largest banks. And if you could carve out the largest four banks, they have been very aggressive in recognizing losses and actually going so far as to push through charge-offs for some of their more problematic commercial real estate loans. I think that that is going to leave the very biggest U.S. banks in a good position to pass these stress tests.

When it comes to some of the mid-sized banks, I would say that’s where things might get a little bit more treacherous because some of your smaller banks that are still, nonetheless, multi-billion-dollars-in-assets banks, some of them haven’t really had the wherewithal, the ability to be that aggressive with their write-offs. So we’re kind of in a wait-and-see mode there. And we’ll see what those stress tests look like for them.

Overall though, one of my greater concerns is credit cards. I think banks have been a little bit more aggressive, surprising me, as the U.S. consumer has weakened. So I’ll be interested to see how their credit card loan books fare in the aftermath of these stress tests.

Simone Del Rosario: What are you concerned about when it comes to credit cards?

Danielle DiMartino Booth: Banks continue to grow their credit card loan books long after they had really clamped down and stopped growing their automobile loan books. And if you think about it, they walk hand in hand. If somebody is going to have trouble paying on their car loan, in many cases, they’re also going to have trouble making good on their other obligations that are in the form of debt.

And yet banks continue to increase the size of their loan books as if this fairly new phenomena of “buy now, pay later” was not running in the background and racking up about a third of whatever we were seeing increases in credit card debt on a per month basis. Buy now pay later was increasing by about a third of that growth rate, yet it’s not reflected on bank balance sheets. It’s not reported to credit agencies.

And that was really what surprised me with banks becoming as aggressive as they have their first quarter bank call sheets. It looks like they finally may have taken a step back, a little bit more risk averse on that front. I’ll be anxious to see what the Fed has to say about their credit cards.

Simone Del Rosario: Banks have gotten a lot better at passing these stress tests. Do you think there’s a chance they are too backward-looking? Let’s hope we don’t repeat the mistakes that led to the 2008 financial crisis, but are we accounting enough for future risks that are more indicative of the time that we’re living in?

Danielle DiMartino Booth: Things indeed are different. I just mentioned buy now, pay later, which certainly was not around 10, 15 years ago. And you’re right, driving through the rearview mirror can be very problematic, fighting the last war.

It remains to be seen where the true stress lies in the system. The fault lines have decidedly moved. We are a much more global and interconnected banking system than we were.

Prior to the pandemic, we heard a lot every day about de-globalization. But in the aftermath of the great financial crisis, there were a lot more entities, countries, banks and firms internationally that took out debt that was dominated in dollars. And that’s just one example that I can think up of where we might not know where the stresses lie.

We just had a very large Japanese bank declare that it was going to be sustaining very large losses based on its holdings of U.S. Treasuries.

Simone Del Rosario: Separate from these stress tests, large banks also undergo living will exercises, which test how quickly the largest banks could unwind Wall Street contracts in the event of a catastrophe. Four of the eight largest banks fell short this time around. What does that tell us?

Danielle DiMartino Booth: That tells you that bankers are really being bankers. It is a bank’s business model to have as much of their capital deployed, working for the bank, making loans, growing the asset base. That is what banks do.

It does not necessarily surprise me to hear that they have failed in writing their own wills. They have shareholders that they have to look out for, and you would normally want to see something of the nature of a will be more of a back and forth, something that is apt to be negotiated after the fact until regulators are comfortable that banks are where they need to be.

But does it surprise me that banks have not been aggressive enough? Absolutely not.

Is higher credit card debt actually good for the economy?

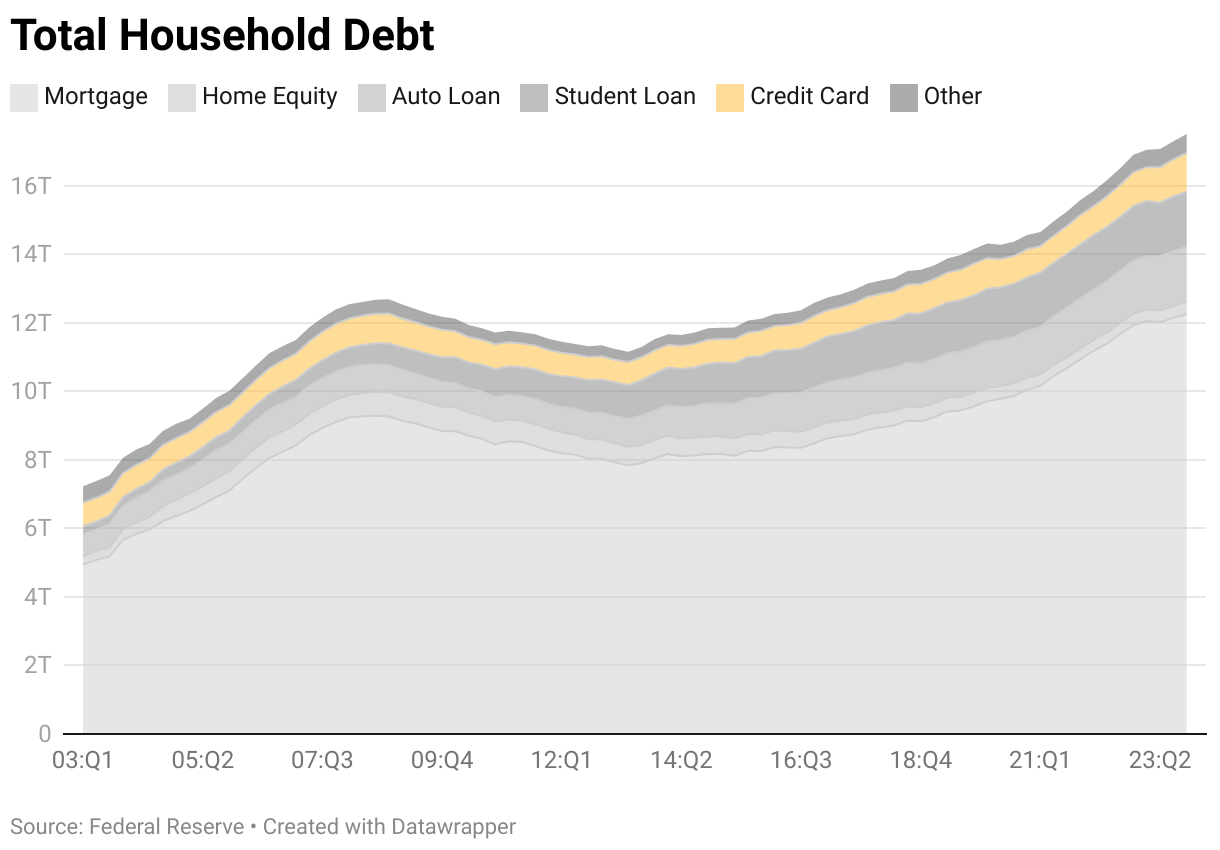

Americans are facing a record amount of credit card debt in 2024 at more than $1 trillion total. Adjusted for inflation, WalletHub says credit card debt is about 10% below its peak, which Americans hit in 2008 during the Great Recession. However, WalletHub estimates growing balances this year could put the inflation-adjusted record in striking distance.

While Americans set the inflation-adjusted record during a dire economic time for the country, higher debt levels do not always spell trouble. In fact, rising debt can boost economic growth, at least for a while.

When higher household debt is a boon

Economists measure the health of a country’s economy by calculating its gross domestic product, which is essentially adding up all of the economic activity in the country. The single most influential part of that equation is consumer spending. It makes up about two-thirds of U.S. GDP.

And though consumers are starting to charge more purchases – credit card debt went up more than 14% in the past year – spending has yet to take a major hit. Economists point to the strong labor market as one reason why.

If the job market takes a turn, Americans may start to rein in that spending. But for now, they seem willing to take on more debt.

In fact, the Federal Reserve reported household debt is at a record high of $17.5 trillion. Most of that is made up of mortgages but also includes auto loans, student loans, and credit card debt. Credit cards, far and away, experienced the biggest percentage increase year over year.

A study by the Bank for International Settlements analyzing dozens of economies found that rising household debt boosts a country’s GDP growth, at least in the short term. In the longer run, they found that a 1 percentage point increase in the household debt-to-GDP ratio tends to lower growth by 0.1 percentage point.

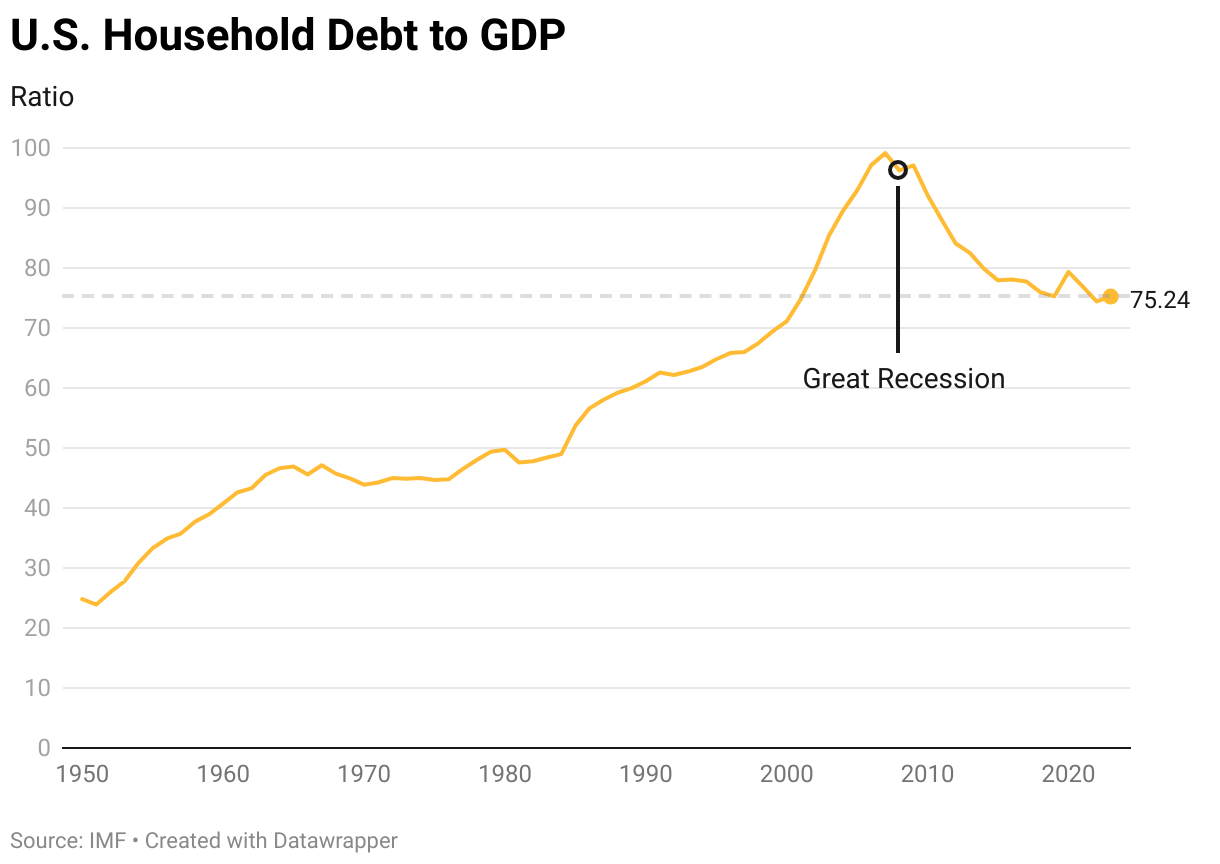

Household debt low when compared to GDP

Household debt as a percentage of GDP is pretty close to the bottom of levels the country has experienced since 2001.

“Debt level growth in recent months appears to be in line with wage growth, so at this point, it doesn’t seem to be raising a red flag,” said Rob Haworth, senior investment strategy director at U.S. Bank Wealth Management. “If people are borrowing more money, the question is whether they are in a position to pay it back.”

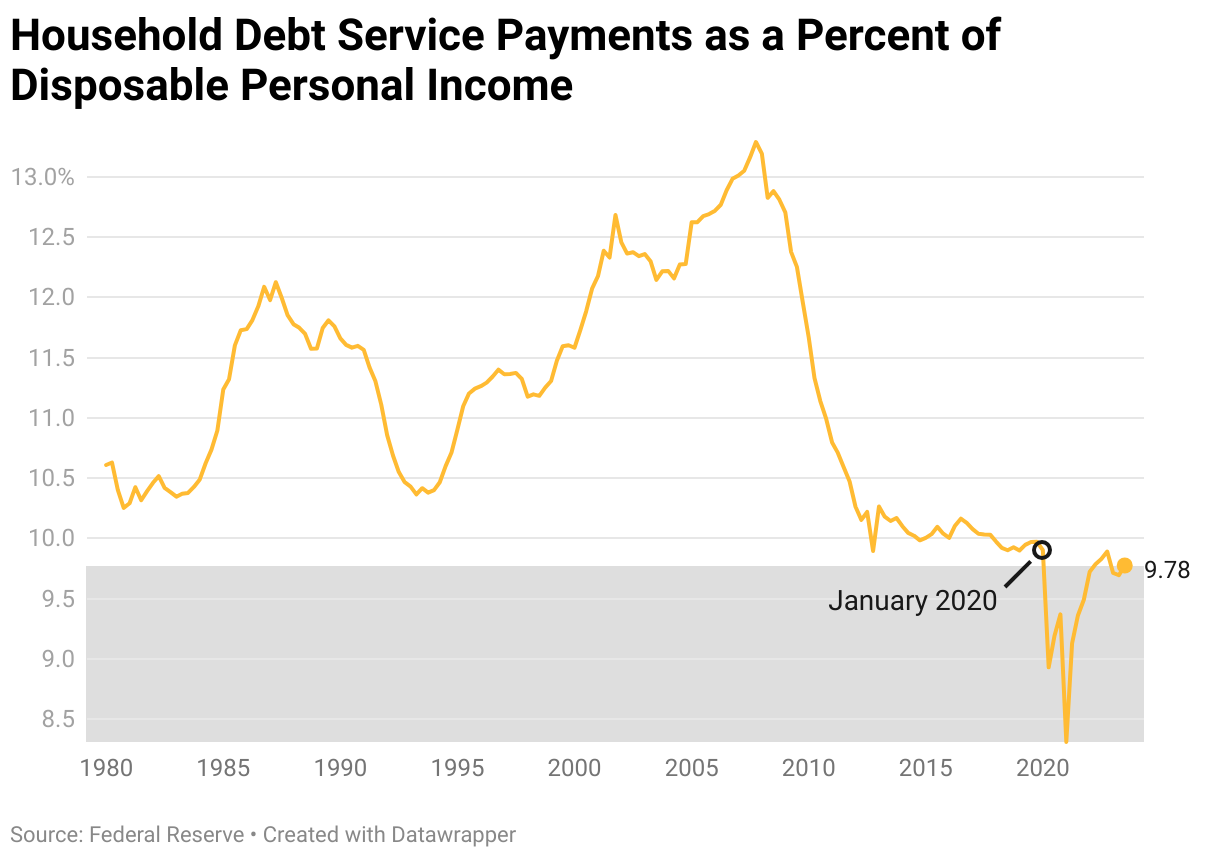

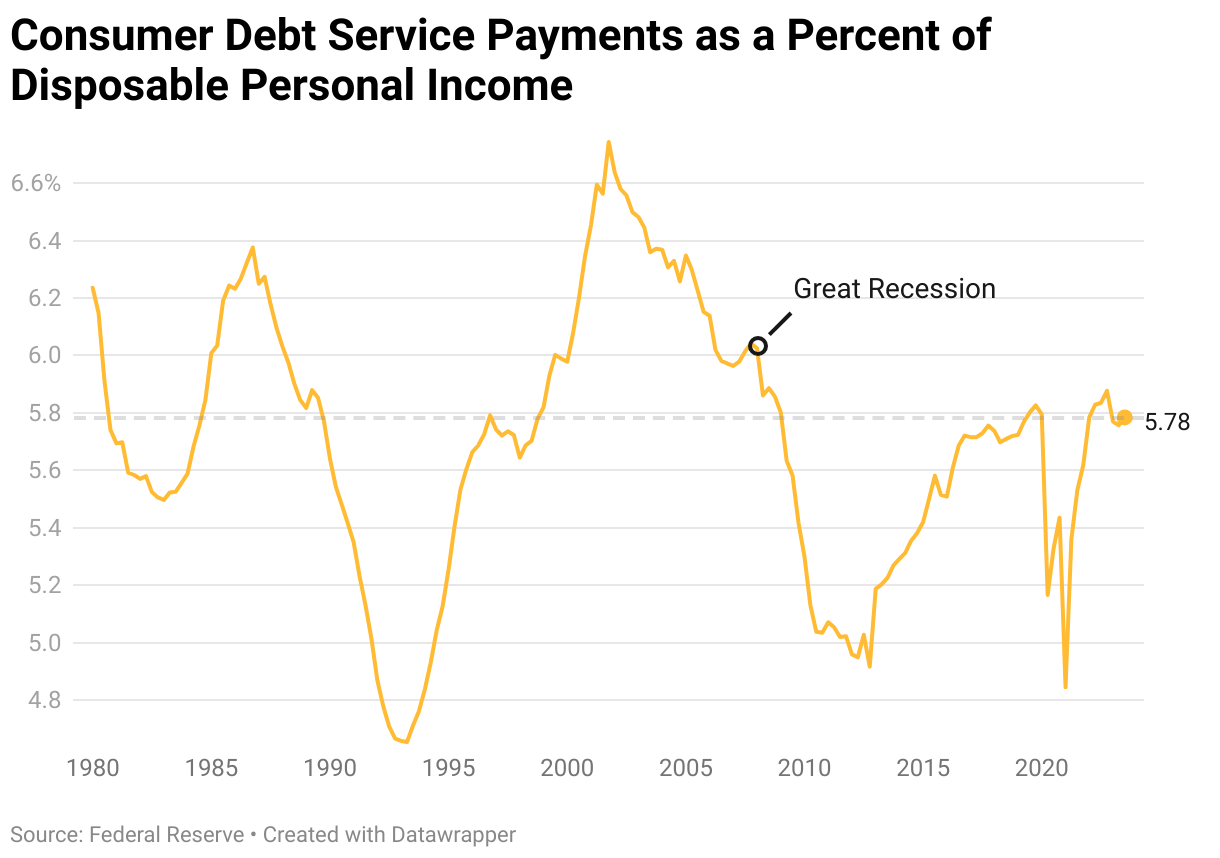

Can Americans afford debt payments?

Economists measure whether society as a whole can afford debt payments by calculating those service payments as a percent of disposable income, which is income after taxes. The only time in recent history this has been lower than now was during the COVID-19 pandemic when people got stimulus checks and didn’t have many places to go to spend money.

If you strip out mortgage debt from this equation, the percentage is sitting a bit higher historically, but it’s still well below the levels that spelled trouble ahead of the Great Recession.

This doesn’t mean individuals are not struggling with credit card debt. Half of credit card users are carrying a balance month to month, and a third of those believe they’ll be in credit card debt forever. We dig into why more people are charging purchases today and what they’re buying here.