State Farm pulls Super Bowl ad, redirects focus to Los Angeles wildfires

As the Super Bowl draws near, companies are gearing up to unveil their most exciting ads for sports fans and consumers. State Farm, however, won’t be one of those companies.

The price for a 30-second Super Bowl commercial can top out at $7 million. Instead, the insurance giant says they will focus on helping those impacted by the ongoing wildfire crisis in Southern California.

A spokesperson for the company said, “Our focus is firmly on providing support to the people of Los Angeles. We will not be advertising during the game as originally planned.”

The decision comes shortly after State Farm offered renewals to policyholders affected by the Los Angeles County fires. The announcement reversed its initial plans last March to not renew 30,000 property policies in California last year. It included 69% of policies in the Pacific Palisades area –– which has been ravaged by the fires since Jan. 7.

At the time, State Farm cited increasing construction costs and an increasing frequency of natural disasters, including wildfires that pose a major risk to policyholders, for the decision to drop coverage.

Right now, more than 170,000 people still remain under evacuation orders. Officials say they must remove hazardous materials before residents can safely return.

Thanks to calmer winds over the past few days, firefighters are making headway against two major blazes in Los Angeles. The Palisades Fire, which is still the largest, has burned nearly 24,000 acres, while the Eaton Fire is 65% contained and has consumed more than 14,000 acres.

As of Friday, Jan. 17, State Farm says they received over 8,300 home and auto claims in affected areas. The insurance giant also says they have paid out over $50 million to policyholders who have filed claims since the fires began.

The company expects this number to rise once evacuation orders are lifted and residents can assess the damage to their properties.

Newsom bans some offers to buy destroyed Calif. properties after fires

California Gov. Gavin Newsom, D, signed an executive order this week to stop what he calls predatory real estate investors from taking advantage of wildfire victims. The order makes it illegal for anyone to make an unsolicited offer on property for an amount less than the fair market value in areas impacted by the Palisades and Eaton Fires for the next three months.

Newsom said the ban comes after hearing from people in the community who’ve received unwelcome and unfair offers.

“This predatory behavior is disgusting at the best of times and of course here in the midst of this tragedy, it’s disgraceful,” Newsom said in a video posted to X.

Today, I signed an executive order prohibiting greedy land developers from ripping off LA wildfire victims with unsolicited, undervalued offers to buy their destroyed property.

The ban, which is modeled after a similar order made by Hawaii Gov. Josh Green, D, for the Lahaina wildfires, is getting some criticism from Sen. Ted Cruz, R-Texas.

“Now, Dem politicians are making it harder for those devastated by the wildfires to sell their destroyed properties. This will only hurt the victims,” Cruz said on X.

Misguided CA policies (1) limited fire mitigation efforts, (2) produced water shortages & (3) under-funded fire fighters.

Now, Dem politicians are making it HARDER for those devastated by the wildfires to sell their destroyed properties.

Newsom responded to Cruz, “Our executive order doesn’t prevent anyone from selling their property. It prohibits scammers from making unsolicited offers to buy property for pennies on the dollar.”

Openly shilling for scammers and bottom feeder land speculators is a weird play — even for you, Ted.

Our Executive Order doesn’t prevent anyone from selling their property.

It prohibits scammers from making unsolicited offers to buy property for pennies on the dollar. https://t.co/agSnPwT1d4

The disaster left homeowners with several questions about insurance coverage.

State Farm reversed its initial plan to cancel hundreds of policies for homes in the Pacific Palisades over the summer to avoid “financial failure,” but is now offering renewals for policy holders in the Los Angeles area.

AccuWeather estimates the total damage and economic loss from the wildfires is at least $250 billion.

State Farm offers renewals for people affected by LA fires it planned to drop

State Farm says it will offer renewals to policyholders affected by the Los Angeles County fires. The announcement reverses its initial plans to drop coverage.

The decision affects policies for homeowners, renters and condo associations. It includes about 70% of the residential policies it has in Pacific Palisades.

The coastal community has suffered significant destruction in this month’s fires, with widespread damage and most residents forced to evacuate their homes.

Thousands of other policyholders around LA County will also be able to renew. However, the offer will not apply to policies that lapsed before Tuesday, Jan. 7.

The Illinois-based insurance giant drew criticism in California for its decision last March to not renew thousands of insurance policies in the state, as many areas in California face increased risk of natural disasters.

State Farm’s decision comes after the California state insurance commissioner’s office pushed insurers to hold off on not renewing policies for people in fire zones.

A spokesperson for the insurance commissioner said the office is working with State Farm to get more information.

Total estimated cost of California wildfires triples to $150 billion as blazes rage on

The estimated total cost of the destructive southern California wildfires has nearly tripled as first responders struggle to contain the largest blazes. The economic toll could reach $135 billion to $150 billion, according to experts at AccuWeather, up from their previous high estimate of $57 billion.

“Hurricane-force winds sent flames ripping through neighborhoods filled with multi-million-dollar homes,” AccuWeather Chief Meteorologist Jonathan Porter said in a statement. “The devastation left behind is heartbreaking and the economic toll is staggering. To put this into perspective, the total damage and economic loss from this wildfire disaster could reach nearly 4 percent of the annual GDP of the state of California.”

As officials work to contain the fires, which continue to grow in size, AccuWeather experts say the estimate for “total damage and economic loss may be revised upward, perhaps even substantially.”

The area from Malibu to Santa Monica has some of the most expensive properties in the United States. The median home value in the area is more than $2 million, with Pacific Palisades sitting right in the middle of the region.

If AccuWeather’s estimates ring true, these fires will become the most costly natural disaster in U.S. history.

Hurricanes tend to be the most costly natural disasters in the U.S. Hurricane Katrina in 2005 is currently the most costly in history, according to Kiplinger, which compiled data from NOAA and adjusted for inflation.

Most expensive natural disasters in U.S. history

5. Superstorm Sandy (2012), $82.0 billion.

4. Hurricane Maria (2017), $107.1 billion.

3. Hurricane Ian (2022), $112.9 billion.

2. Hurricane Harvey (2017), $148.9 billion.

1. Hurricane Katrina (2005), $186.3 billion.

Meanwhile, insured losses from the southern California fires could reach $20 billion, according to JPMorgan. Analyst Jimmy Bhullar said that number could rise “even more if the fires are not controlled.” Raymond James issued a similar estimate, saying insured losses could range from $11 billion to $17.5 billion. Morningstar analysts estimated insured losses will exceed $8 billion.

“When you have these things like wildfires or hurricanes or floods, and the loss affects a large portion of the population, especially in a very small geographical area at the same time, insurance works, but it doesn’t work as well,” said Chuck Nyce, a professor of risk management and insurance at Florida State University. “It becomes more expensive, and the losses to the insurance company, when they become what they call ‘correlated,’ it makes insurance companies’ cost of capital higher, it makes their losses higher, it makes them more reluctant to do a large volume of business in a specific area.”

As insured losses mount, homeowners in the area will face an uphill battle to rebuild.

State Farm, a major insurer in the state, reportedly canceled hundreds of policies for homes in the Pacific Palisades over the summer to avoid “financial failure.” But there are options for those who can’t find private coverage in their communities.

“People forget that if you look across the United States, if you look at the first three quarters of 2024, there were 25 different events in the United States that caused more than a billion dollars in damage to properties,” Nyce told Straight Arrow News. “When we think about these disasters, we think of these areas like, ‘Oh, Florida is the problem,’ or, ‘Oh, California is the problem.’ They are much more widespread than people realize.”

In California, Fair Access to Insurance Requirements (FAIR) “is a syndicated fire insurance pool comprised of all insurers licensed to conduct property/casualty business in California.” It is an insurer of last resort, when homeowners can’t get policies from private companies.

The program uses no public or taxpayer funding, but that doesn’t stop the cost from being spread to policyholders throughout the state.

As estimates of the total economic toll and insured losses continue to rise, a number of major players in insurance saw their stock slide to open trading on Friday. This includes firms like Travelers, Allstate and AIG.

California wildfires causing $57 billion in damage as providers canceled insurance

The devastating southern California wildfires could cause between $52 billion and $57 billion in economic losses, according to experts at AccuWeather. But homeowners affected have unique insurance factors in play as they try to put their lives back together. In the months leading up to the disaster, many affected homeowners lost their original insurance coverage.

There are at least five fires covering more than 45 square miles affecting the region. The Palisades Fire is the biggest, burning through nearly 27 square miles and destroying more than 1,000 buildings. As of the morning on Thursday, Jan. 9, it was zero percent contained and being called the most destructive fire in Los Angeles’ history.

“Should a large number of additional structures be burned in the coming days, it may become the worst wildfire in modern California history, based on the number of structures burned and economic loss,” AccuWeather Chief Meteorologist Jonathon Porter said.

In the wake of the devastation, homeowners in the area will face an uphill battle to rebuild. State Farm, a major insurer in the state, reportedly canceled hundreds of policies for homes in the Pacific Palisades over the summer to avoid “financial failure.”

“Insurance is a social good,” said Chuck Nyce, a professor of risk management and insurance at Florida State University. “It is really good at covering a loss that you may have when a bunch of other people who have the same exposure to it don’t have the loss at the same time. For one person who has an auto accident, there are hundreds of people who are insured who don’t have an accident at the same time.”

“When you have these things like wildfires or hurricanes or floods, and the loss affects a large portion of the population, especially in a very small geographical area at the same time, insurance works, but it doesn’t work as well,” Nyce said. “It becomes more expensive and the losses to the insurance company, when they become what they call ‘correlated,’ it makes insurance companies’ cost of capital higher, it makes their losses higher, it makes them more reluctant to do a large volume of business in a specific area.”

Filling the insurance void

Insurers have been backing out of the area as wildfires become more frequent and destructive. But there are options for those who can’t find private coverage in their communities.

“Every state has some type of a residual market called a FAIR plan. In most states, that will enable you to get access to that insurance, even if the private market is not willing to provide it,” Nyce said.

In California, Fair Access to Insurance Requirements “is a syndicated fire insurance pool comprised of all insurers licensed to conduct property/casualty business in California.” The program uses no public or taxpayer funding. But that doesn’t stop the cost from being spread to policyholders throughout the state.

“States have a variety of different ways in which they fund their FAIR plans. Some of them just allocate those policies to insurance companies,” Nyce said. “Other ones, what they’ll do is they will bill the insurance companies for losses that the FAIR plan absorbs. And if that’s the case in many states, what those insurance companies do, they can pass through those additional losses that they’re paying to the FAIR Plan to their current policyholders. So even though the state’s not paying for it, the citizens of that state are paying for it.”

The number of California FAIR policies has doubled between 2020 and 2024, reaching more than 450,000 customers, as insurers dialed back coverage in fire-ravaged regions. Since 2020, FAIR’s insurance exposure has surged from $153.43 billion to more than $458.08 billion, a 200% increase.

Nyce said all of this will eventually result in a secondary problem for people seeking homeowner policies.

“Price, availability, affordability, these are all issues that are going to be on the docket for California, probably for the next 10 or 20 years, with regard to insurance.”

“Sitting with my family, watching the news, and seeing our home in Malibu burn to the ground on live TV is something no one should ever have to experience,” she wrote in an Instagram post. “This home is where we built so many precious memories … My heart and prayers are going out to every family affected by these fires.”

Despite the fact that many homeowners in the Palisades Fire have the means to recover, Nyce still says it’s not a good idea to go without insurance.

“These are some of the wealthiest homes in the country, some of the most expensive homes in the country, they can afford it, then they should be able to afford their insurance premiums,” he contended.

California to require insurers to offer policies in fire-prone areas

In recent years, destructive wildfires across California prompted some insurance companies to stop writing new policies for high-risk areas. Now, California is implementing a new regulation requiring home insurers to offer new policies in fire-prone areas if they want to remain in the state, California Insurance Commissioner Ricardo Lara announced Monday, Dec. 30.

This is the first regulation of its kind in California.

“Californians deserve a reliable insurance market that doesn’t retreat from communities most vulnerable to wildfires and climate change. This is a historic moment for California,” Lara said in a statement.

Insurers must cover at least 85% of their statewide market share in those high-risk regions, gradually increasing coverage by 5% every two years until they reach the target, according to a news release from Lara’s office.

In exchange, California will modernize reinsurance regulations to help insurance companies expand coverage and offer more policies in high-risk communities –– something the commissioner believes will boost stability and resilience in the market.

Reinsurance is insurance for insurance companies that provides support in the event of large-scale losses.

Opponents of the new regulation disagree.

Consumer Watchdog President Jamie Court spoke to KTVU News and said rates are on track to rise by 40%.

“There is no legally binding commitment in this document that they have to cover more people, but we’re all going to be paying more,” Court said. “There is nothing in these, like, you know, 72 pages of regulation and explanations about the cost impact on consumers.”

Consumer Watchdog says it will sue to block or overturn the new regulations, KTVU reports.

Insured losses from natural disasters top $100B for 5th straight year

Hurricane season in the United States has been over for about two weeks but the damage totals are still coming in. Around the world, disaster costs have mounted.

For the fifth straight year, insured losses have topped $100 billion globally, according to the Swiss Re Institute. Those are financial damages covered by an insurance policy.

The institute says two-thirds of the $135 billion in insured losses came as a result of Hurricanes Helene and Milton, as well as a high frequency of thunderstorms in the U.S.

Helene was a Category 4 storm in September. It pounded the Southeast with more than 40 trillion gallons of rain, according to AccuWeather. That led to destructive flooding that washed away roads, bridges and buildings in mountain towns in western North Carolina.

Hurricane Milton came next in early October, roaring ashore just south of Tampa, Florida. Massive flooding, storm surge and vicious winds did the most damage. The chief economist at Swiss Re says economic development continues to be the main driver of the rise in insured losses from floods.

The Biden administration has sent a $100 billion request to Congress to help Americans affected by the major disasters in 2024 and 2023. However, the legislative year is winding down with the Senate slated to adjourn next Friday, Dec. 20.

It’s not just the United States. The Institute says $10 billion in insured losses were attributed to Europe, where storms led to flooding in places like the Czech Republic, Poland, Austria, Spain, Romania and Italy.

Florida officials put out warning over scammers impersonating FEMA agents

As thousands of people look to rebuild their lives after Hurricanes Helene and Milton, Florida officials are putting out a warning about scammers impersonating Federal Emergency Management Agency (FEMA) officials. Sarasota County’s emergency management chief announced on Thursday, Oct. 17, that imposters with fake FEMA badges were asking residents for their bank account information.

The agency advises individuals to never give out their bank account information nor give cash to anyone claiming to be a FEMA agent.

FEMA also notes that natural disaster survivors should be aware of online scammers. The agency advised people to avoid sharing personal or financial information online, as well as following links promising offers for FEMA disaster assistance.

FEMA maintains it does not “endorse any commercial business, products or services.”

If a person has any concerns about potential scams, the agency advises people to call local law enforcement or report any suspicious or fraudulent activity to the National Center for Disaster Fraud’s website.

Insurance analysts estimate recovery from Hurricanes Helene and Milton could soar past $100 billion.

Zillow adds climate-risk tool to listings, researchers weigh in on viability

The recent hurricanes in Florida have some people thinking about the possible threats extreme weather can have on their homes. In addition, recent numbers show climate risks have become a critical consideration in buying homes, which led to Zillow launching a climate-risk tool. But, how reliable is the new tool?

The real estate website teamed up with First Street, a climate risk financial modeling company, to create an interactive platform that gives insight into hazards from floods, wildfires, wind, heat and air quality.

It shows the risk percentages estimated 15 years and 30 years into the future, the standard lengths of time for fixed-rate mortgages.

A September 2023 Zillow survey found that 83% of people considered climate risks when looking at homes. But, according to Heatmap News, there are a few things to keep in mind when using Zillow’s tool.

Climate-risk tool tips

A Bloomberg investigation found tools like First Street may be questionable because different climate risk models could give very different estimates for the same property.

One tip is to use Zillow’s flood risk assessment as a starting place, but contact the local government to learn more. That’s because the ability to figure out whether a house will flood depends on knowing the local infrastructure including stormwater drains, which does not exist on climate risk models.

Climate experts said to take it seriously if Zillow lists that a property flooded recently, because that data is typically reliable and should be a red flag.

Another note from researchers is that Zillow’s tool will likely underestimate a home’s wildfire risk, especially in the Western U.S. That’s because computer models that estimate wildfire risk are in an early stage of development.

Also, when assessing whether a home faces wildfire or flood risk, a buyer should factor in the whole neighborhood. That includes considering whether the roads would still be drivable if power lines fell, which is not detected on Zillow’s tool.

Main takeaway

Overall, the experts cited by Heatmap News said using climate-risk tools like this can be helpful, but to do your own research, too.

Some believe community officials should be investing in climate-risk tools, so it’s not only up to the consumer to look for data.

For example, the state of California invested in a public wildfire catastrophe model so it can figure out which homes and towns face the highest risk.

How Florida’s state-backed insurance went from last resort to largest provider

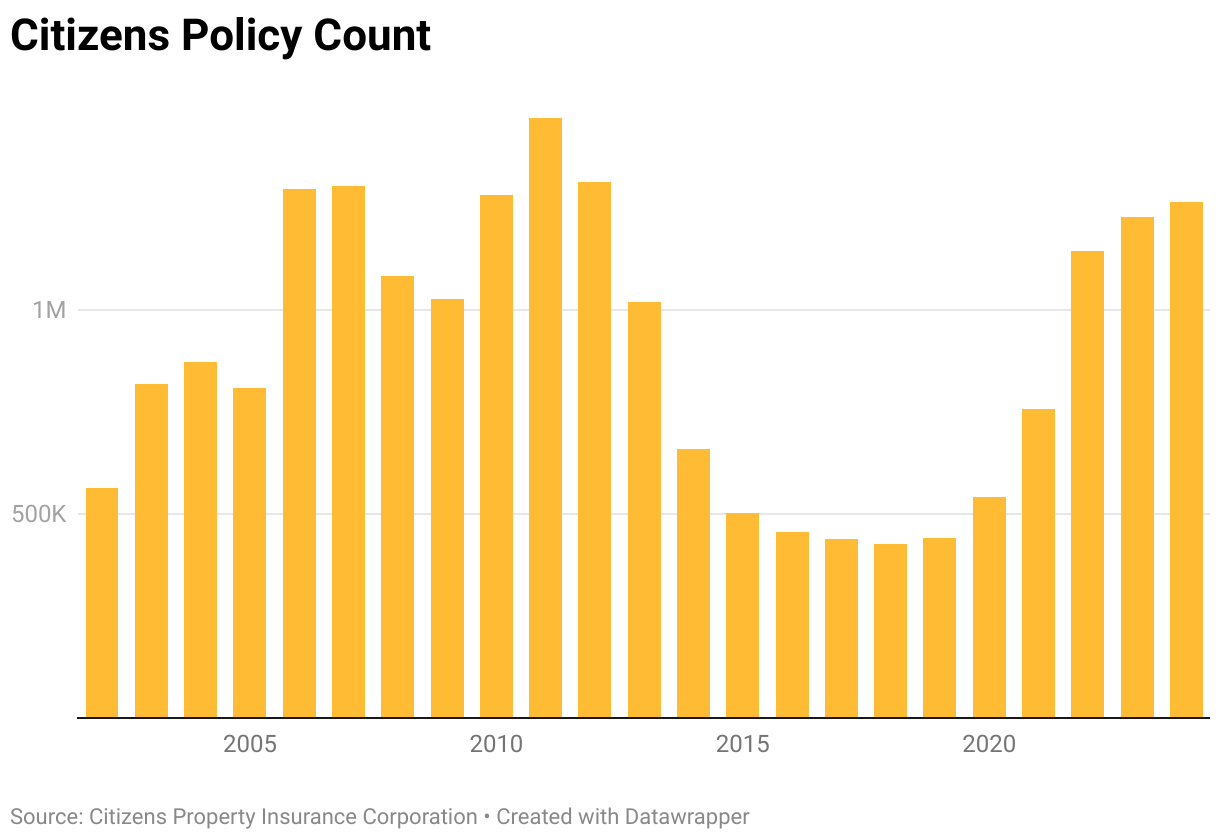

It was meant to be the insurance of last resort. But along the way, Florida’s government-backed Citizens Property Insurance Corporation became the largest insurance provider in the state.

“Citizens Property Insurance, which was created decades ago, it is not solvent, and we can’t have millions of people on that, because if a storm hits, it’s going to cause problems for the state,” Florida Gov. Ron DeSantis said in February 2024.

“They are actually very financially secure this year,” Proffesor Charles “Chuck” Nyce, who serves as department chair of Florida State University’s Risk Management and Insurance, said. “I believe what Gov. DeSantis was trying to say is that we don’t want Citizens having this type of exposure and having the need to do assessments.”

Assessments happen when Citizens does not have enough money to pay its claims. First, it applies a surcharge to its own policyholders. But if that is not enough, the state requires Citizens to charge a premium to insurance holders statewide, whether with Citizens or not. Citizens will have to do this for as many years as it takes to plug the deficit.

They were designed to be the market of last resort…For 2021, 2022, 2023, Citizens was becoming the option of first resort.

Chuck Nyce, expert in risk management and insurance

Citizens told Straight Arrow News it “has the financial capability to handle a 1-in-82-year storm without having to levy assessments on non-Citizens policyholders.” For context, Citizens says 1992’s Hurricane Andrew was a 1-in-43-year event.

“Hurricane Andrew is what we kind of describe as a wake-up call,” Nyce said. “It was really the first experience for the insurance industry of what a large-scale catastrophe could look like in the United States. I started graduate school the year after Hurricane Andrew. So my entire academic career has been trying to figure out how to pay for catastrophes that can occur.”

Hurricane Andrew bankrupted several insurance companies, leaving hundreds of thousands in Florida without insurance. Other major insurance providers dramatically mitigated their risk in the state by shifting their focus more inland.

“Now the problem is, for the state of Florida, we have a lot of coastal exposure, so we had to find a way to still insure those properties that were out there,” Nyce said.

If we can solve it in Florida, it’ll be a great lesson to take to other states.

Chuck Nyce, expert in risk management and insurance

Local companies popped up to fill the gaps, while the state created two insurers of last resort that later merged in 2002 to become Citizens Property Insurance Corporation. Nyce said the system worked well until 2004 and 2005, when storms repeatedly hit the Sunshine State, causing tens of billions in losses.

For Florida’s insurance landscape, it was Groundhog Day. Insurance companies dried up and more left the state. But this time, they had a backstop in Citizens, and Citizens’ policies ballooned.

“They were designed to be the market of last resort,” Nyce said. “By 2010, 2011, there were 1.4 million policyholders in Citizens. The good news for the state is from 2005 through 2016 we didn’t have any landfalling storms.”

Citizens successfully shed policies back into the private market until it was down to a little more than 400,000 by 2019. But more storms and litigation costs again broke the private market.

“For 2021, 2022, 2023, Citizens was becoming the option of first resort,” Nyce said. “There was a number of areas where insurance was not available and not available at a fair price. So Citizens became the option.”

Policies swelled back to over 1 million in 2022 and now sit at 1.265 million as of Oct. 4, 2024.

In order to get customers off the state-backed Citizens and back into the private market, a private insurance provider must be willing to underwrite the client at a price that is no more than 20% higher than what they pay at Citizens. At that point, Citizens can “depopulate” that customer.

Depopulation is “trying to push Citizens back to a market of last resort rather than a first choice,” Nyce explained.

“I think it’s more attractive today to offer policies than it was over the last 20 years,” DeSantis said in February. “But, you know, Rome wasn’t built in a day.”

Citizens told SAN that before Hurricanes Helene and Milton, it expected to dip below 1 million policies by the end of 2024. These storms could put that goal in jeopardy.

“When losses get really bad, that’s when the state should come in,” Nyce said. “When they get really, really bad, that’s when the federal government should come in. But for the storms like Helene, that should be private market stuff that’s handling those types of things. But it’s an issue we have.”

Nyce said from an insurance perspective, homeowner policies used to be considered low-risk and relatively stable. But that’s no longer the case in much of the United States, andnd that’s when states see the private market disintegrate.

“If we can solve it in Florida, it’ll be a great lesson to take to other states,” Nyce said.

When it comes to insurance risks, it’s not just hurricanes in Florida and Louisiana. It’s wildfires in California, tornadoes in the Midwest and severe convective storms hitting everywhere in between. Florida may be the tip of the spear for storm exposure, but it does not stand alone.