California winery owner fined $120K for letting worker live in trailer on his land

A winery owner in California faces a $120,000 fine for allowing an employee and his family to live in a trailer on his private property. The move violated a Santa Clara County ordinance that prohibits recreational vehicles from being used as dwelling units.

For years, the county issued daily fines to the Ballard family until they either remove the trailer or evict their worker, Marcelino Martinez. The Ballard family is now suing with the help of the Institute for Justice.

“Marcelino has been our vineyard manager for over 20 years,” Michael Ballard said. “Somehow, the Martinez family living in a trailer on the back of 60 acres, where no one can see them and they don’t come into contact with anyone else, can be interpreted as a public nuisance. That made little sense to us at all.”

In Santa Clara County, housing costs are high. The average home prices sit around $1.5 million and median rent for apartments hover around $3,200. The Ballard family allows Martinez and his family to live in the trailer rent-free as part of his work agreement.

“It’s very hard to live in San Jose, paying rent and buying food is very expensive,” Martinez said. “If I have to leave, I don’t have another choice but to look for another job.”

In 2017, a county code enforcement official visited the property and stated that the trailer could not be used as a home. In response, the Ballard family decided to construct an accessory dwelling unit, which is approved by the county as a lawful place for Martinez to stay.

However, the slow permit process delayed the construction. Until the new unit receives final approval, the Ballard family will continue to incur daily fines, resulting in the $120,000 figure.

The Institute for Justice argues that the fines violate the Eighth Amendment of the U.S. Constitution, which prohibits excessive fines. They contend that treating each day as a new violation inflates the penalty dramatically.

“The fines — I don’t understand. I want them to stop fining Mike,” Martinez said.

“I hope the county recognizes that good Samaritan behavior should not be penalized, it should be encouraged,” Ballard said. “If everyone in a better position helped those less fortunate, it might actually solve some of the homeless problems in this county.”

The county has not responded to recent media requests for comment on the lawsuit.

Does Fed rate cut plus falling mortgage rates equal more affordable housing?

Falling interest rates may pique the interest of prospective homebuyers but experts don’t necessarily think it is going to loosen the market anytime soon. The rate for a 30-year fixed mortgage averaged 6.09% for the week, according to Freddie Mac. The dip comes as the Federal Reserve cut its benchmark interest rate by 50 basis points on Wednesday, Sept. 18.

Mortgage rates have been slowly declining since hitting a 23-year high of 7.79% in October 2023. Though rates may still seem pretty high, every percentage point makes an impact. For every one percentage point mortgage rates increase, buying power lowers by 10%.

At the same time rising mortgage rates decreased buying power, housing prices skyrocketed. Even with recently falling mortgage rates in anticipation of the Fed cutting its key rate, the housing market has barely budged.

Existing home sales fell 2.5% in August, according to a release from the National Association of Realtors.

This transcript has been edited for length and clarity. Watch the full interview in the video above.

Simone Del Rosario: Homeowner hopefuls have been putting off plans to buy for years. Are these lower rates going to be the entrance point they’re looking for?

Selma Hepp: I think the lower mortgage rates are certainly helping. Every time we saw mortgage rates come down, it did help spur some buyer demand. For example, when you think about what happened after the Fed meeting last December, mortgage rates came down. That certainly spurred housing market demand; same thing the year prior.

So whenever we move closer to 6% and further away from 7% and even come down to the 5% range, it does help with affordability. It helps with a buyer’s budget and it brings back that demand that we desperately have been needing in the housing market.

Simone Del Rosario: Is it possible that more affordable mortgage rates could actually drive up housing prices since more buyers would be trying to enter the market?

Selma Hepp: Yeah, that’s a question that keeps coming up because everybody’s worried that there’s so much pent up demand and not enough supply, meaning that as soon as mortgage rates come down, you’ll see more buyers coming in and pushing those prices higher. That’s certainly a possibility, but what we did see over the course of this year is more inventory of existing homes for sale, and that has helped put a lid on home price appreciation.

And the other thing is, when you think about mortgage rates further coming down, it’s going to unlock some of that inventory that’s been locked in because the difference was so high between where people locked in and where mortgage rates were.

So with that spread coming lower, I think we’re going to see unlocking of some of that inventory, so the balance between buyers and sellers is going to be better, and it’s going to keep the lid again on the rate of home price appreciation. So we certainly hope for that going forward.

Simone Del Rosario: For sellers looking at the market right now, when would be an optimal time for sellers to enter the market?

Selma Hepp: That’s usually very individual decision. It depends on how long you’ve owned the home. Are you moving to another place where home prices are more affordable or not; are you staying in the area? And it depends also, on what your family situation is.

A lot of time sellers are driven by a change in family status. So they are either selling because they need a bigger home or there is a divorce situation, or maybe somebody is no longer around, and so that’s usually what drives sales.

That’s the most frequent reason for sales, but sometimes lower mortgage rates are helping. They do help sellers sort of feel better about their next purchase because it’s more affordable again. And I think definitely with mortgage rates coming down, it’s going to help with that sense of, ‘How much am I giving up to buy my new home?’ So yeah, I think it will help the number of sellers in the market as well.

Simone Del Rosario: Yes, selling a home is an individual decision and has to do with your personal life. But what we’ve seen over the past couple of years is people holding onto their low interest mortgage rates and not moving on to the next home when they typically would.

So this could unleash sellers, but at the same time, I believe the sellers would want to have the best price they can get for their house since they’ve waited so long to be able to sell it.

Selma Hepp: That’s often an interesting dilemma because you want the most you can get for your home, but then you also think about, with next home that you’re purchasing, that next seller is gonna want for the most for their home as well.

That’s always a dilemma that sellers find themselves in, but you’re absolutely right in terms of length of tenure for sellers. Over the course of the last couple of decades, we’ve seen people staying in their home longer and longer because homes have become increasingly more unaffordable and there are fewer homes available for sale.

So oftentimes what I hear sellers say is, ‘I do want to sell. I do want to move, but where am I going to move? There’s no inventory. There’s not something that fits what I’m looking for.’ And so they just end up staying put.

Simone Del Rosario: Obviously, these mortgage rates have been a large part of people’s decision-making process. But as you just pointed out, that’s not the only thing that is stalling the housing market. What are the other things that are making the housing market more sticky?

Selma Hepp: Affordability is the biggest one. But affordability, the lack of affordability, comes from the fact that we’ve under built for so long, particularly first-time or entry-level homes. So when people are trying to think about their first home or thinking about moving to another home, there are fewer homes to choose from. So that’s holding people back a lot.

We definitely saw that. For example, mortgage rates came down in early spring of 2023 and we saw a burst of buyers coming into the market, but there were not enough homes for sale. And that’s when home prices surged again and we saw significantly more appreciation in the market because of that imbalance.

Markets are betting on a supersized rate cut. Why the Fed may disappoint.

Markets are increasingly betting the Federal Reserve will make a supersized rate cut at this week’s meeting. There are two camps: Those who believe the Fed will cut interest rates by 25 basis points and those who believe the Fed will double up to 50 basis points.

A week ago, 2 out of 3 futures traders were betting the Fed would do a 25 basis point cut, according to CME FedWatch.

But by the time the Fed started its two-day meeting the morning of Tuesday, Sept. 17, odds had switched. As of 10 a.m. ET, 2 out of 3 futures traders were betting on a jumbo cut to kick off this rate-cut cycle.

“The market is thinking this because the market is sniffing out some economic weakness,” Fed Guy and CIO of Monetary Macro Joseph Wang told Straight Arrow News. “They’re noticing that the unemployment rate has gone up. It seems like there are a lot of indicators that the Fed might be over-tightening, and so in order to get ahead of this, the Fed might want to do with a supersized cut. Now I’m not in that camp, because so far, what I hear from Fed speakers is that it’s more likely that the economy is normalizing.”

Wang is in the 25-basis-point camp, joined by former Fed adviser and QI Research CEO Danielle DiMartino Booth.

“They want to be measured and gradual,” DiMartino Booth told Straight Arrow News. “They want to be Greenspan-esque. [Former Fed Chair Alan] Greenspan had 17 25-basis-point rate hikes in a row. So it was a little bit different dynamic. It was a tightening campaign, but they want to be as measured. They want to be able to say, ‘We’re going to engineer a soft landing. We’re going to be taking interest rates down at a very slow pace.’”

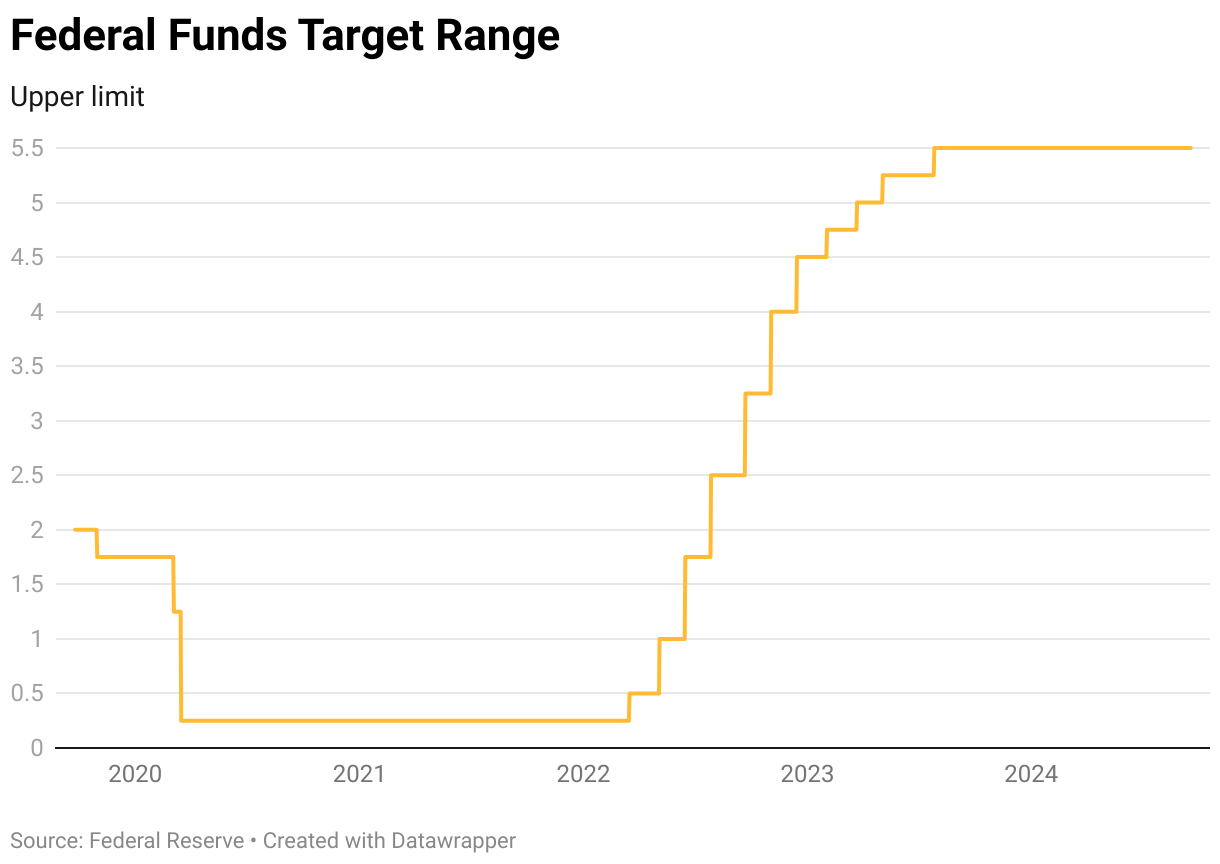

When inflation started getting out of hand in 2022, the Fed began its rate-hike campaign to tighten monetary conditions and get people and businesses to spend less. It hoped the move would bring down prices.

The team hiked the Fed funds target range all the way to 5.5%. They’ve held it there for more than a year now. This is the highest the rate has been since early 2001.

But now inflation is much closer to the Fed’s 2% target, the unemployment rate is rising. Therefore, a soft landing is getting more elusive.

Markets are betting that the Fed funds rate will go down to below 3% by next summer. That would mean cutting 250 basis points in less than a year.

“The pricing in the market seems to be pretty aggressive,” Wang said. “From my perspective, I think there’s too much doom and gloom being priced in. My base case expectation is that rather than having a series of huge cuts that the market is assuming that we have, some steady 25 basis point cuts, and maybe the cut cycle ends, let’s say around 3.5%, rather than below 3%.”

Wherever it lands, Americans will see a change in what it costs to borrow money. In the same way as when the Fed was hiking rates and mortgage rates, auto loans and credit card interest rates soared, this time those interest rates will also go down.

In fact, it’s already happening. Ahead of Wednesday’s Fed cut, mortgage rates fell to levels not seen since early 2023. If the Fed cuts rates by 25 basis points following its meeting, that cut is likely priced into the current mortgage rates. But if they go jumbo-sized to 50 basis points, mortgage rates could go down even more.

Subscribe to the Straight Arrow News YouTube page and tune in Wednesday, Sept. 18, at 2:10 p.m. ET, where SAN will have a live report of the Fed’s final decision and comments from Fed Chair Jerome Powell.

Core inflation is still above 3%: Is it time for the Fed to move its target?

Inflation cooled for the fifth straight month in August at 2.5%, inching closer to the Federal Reserve’s target of 2%. But core prices, which strip out food and energy, stayed stagnant at 3.2%. Is it time for the central bank to adjust its core inflation target of 2%?

The Federal Reserve has a dual mandate of full employment and price stability. To keep those numbers in line with a strong economy, they use tools like adjusting the federal funds rate, which is the overnight lending rate for banks but in a downstream way that affects interest rates on everything from mortgages to car loans.

The range is currently set at 5.25-5.50% after the Fed raised rates from near zero starting in March 2022 through July 2023. The Federal Open Market Committee will meet next week and is expected to start cutting interest rates for the first time this year.

While it seems like the 2.5% increase in consumer prices would give Fed Chair Jerome Powell a little cover, the central bank puts the focus on core inflation, which strips out volatile food and energy prices. Core inflation is still at 3.2% annually due mainly to rising shelter costs.

Straight Arrow News interviewed Monetary Macro CIO and the Fed Guy Joseph Wang Wednesday morning, Sept. 11, to discuss the latest inflation data. The conversation turned to whether the 2% target is a realistic endgame.

The following transcript is edited for length and clarity. Watch the full clip in the video above and catch the entire interview on SAN’s YouTube page.

Joseph Wang: I think we might be in a new, higher inflation regime. So we have to be careful. The future does not always look like the past. Over the past 20 years, we’ve had a world where inflation was pretty stable around 2%, but it wasn’t always like that.

Before the “Great Moderation” period, we were in the 1970s and 80s where inflation was volatile and sometimes very high. I think we’re heading into an era where inflation is probably going to be more volatile and higher than it was in the past. That’s certainly what the CPI is telling me.

Now looking on a year-over-year basis, we’ve been above 3% for some time and honestly, it looks kind of stuck there. Now we could have recessions that temporarily bring that down, but I think the next time we have a recession, maybe we just have more stimulus checks and so forth, and that makes it surge again.

So I think the future is going to be a world where inflation is going to be higher and more volatile. And that’s something that we’re going to have to get used to.

Simone Del Rosario: Fed Chair Jerome Powell gets asked this a lot and he loves to slap this down, which is, “Is the 2% target rate out of date and should we be looking at a 3% target?”

I know Jay Powell continues to stick to his 2% conviction but are you hearing anything different?

Joseph Wang: We have to realize that the 2% inflation target is nothing magical. It’s nothing set in stone. It’s a decision made by people. Now, in the Fed’s case, it was decided in 2012 to have an inflation target of 2%. Does it have to be that way? We could easily change it.

I think it’s helpful to understand why we might want to change the target. Traditionally speaking, economists think there’s a trade off between inflation and unemployment. So they would think that if we have 3% inflation, in order to get 3% inflation down to 2%, we have to have a bit of a recession, we have to have the unemployment rate go up a little bit. So ultimately, whether or not we decide to have a higher inflation target is a political decision as to whether or not the government can tolerate a temporary recession.

When inflation was around 4% and it looked like it would have come down, there were actually many people, influential people, writing columns in big newspapers saying, “Hey, why don’t we just change the inflation target so that it’s 3% or maybe a little bit more, instead of 2%?” They were saying this because they did not want the political costs of having temporarily higher unemployment, of creating a recession. So whether or not we change the inflation target is ultimately going to depend upon the political appetite for economic weakness.

Honestly, at 3% inflation, I think that’s close enough to 2% that people would just kind of struggle and say, “Yeah, it’ll eventually get there,” and they won’t have to change the target. But the next economic cycle, when we have an upswing, maybe inflation goes back to 4%, maybe a little bit more. Depending on who’s in power, maybe they don’t want to take that risk of having a recession to get inflation down, and maybe at that time, we’ll have some serious conversations within the government about whether or not they could change the inflation target.

To your point about what the Fed people have been talking about now, definitely they would never say that they’re going to raise the inflation target. But at the moment, they are having a discussion about their framework and that’s due to be released in a couple years.

There are former Fed speakers who are whispering that, “Instead of having a 2% inflation target, what if we have something called an inflation band?” So what that means is that my target is not a 2% point, but maybe it’s 2% plus or minus 1%. So that means that inflation at 1.5% is within the band, it’s okay. If it’s 2.5% or even 3%, that’s okay as well.

So that could be a way to, by sleight of hand, increase the inflation target simply by tolerating inflation higher than 2% because it’s still within the band. That is something that people discussed before in the Fed and now they’re discussing again. I don’t know what they will ultimately decide. I think it might depend upon just how easy they think it is to maintain 2% in the coming years.

Inflation cools to 2.5% in August but monthly core prices came in hotter

Consumer price inflation cooled for the fifth straight month in August at 2.5% annually, inching closer to the Federal Reserve’s target of 2% inflation one week before the central bank’s next rate decision. Monthly prices rose 0.2% from July, according to data released by the Bureau of Labor Statistics Wednesday, Sept. 11.

Core inflation, which removes volatile and energy prices, rose 3.2% annually and 0.3% compared to July. While the annual number came in as expected, the monthly increase is hotter than the 0.2% expected.

Shelter continues to be the main driver of core inflation as the index went up 0.5% compared to July and is still up 5.2% year-over-year. Shelter price increases are responsible for 70% of the annual rise in core prices.

The price of groceries didn’t budge on a monthly basis, and food away from home rose 0.3% over July. Energy prices dropped 4% annually while gas prices are down 10.3% compared to August of last year.

New car prices were unchanged for the month and fell 1.2% on an annual basis. Used cars, which had a massive spike amid the latest inflation run, dropped 10.4% compared to August 2023.

The BLS also reported the airline fares index rose 3.9% in August after declining in each of the previous 5 months.

August’s inflation report is one of the last data puzzle pieces ahead of the Federal Open Markets Committee meeting next week. The Federal Reserve is expected to cut interest rates for the first time since 2020. The central bank has a dual mandate and uses inflation data and unemployment to make its policy decisions.

The U.S. economy missed expectations and added just 142,000 jobs in August, but the unemployment rate did come off July’s surprise 4.3%, settling at 4.2%.

A New York law went into effect in September 2023 that banned property owners from renting out homes for fewer than 30 days unless the host stayed there with the guests and registered with the city. At the time, the city claimed apps like Airbnb and VRBO exacerbated the city’s rising rents and contributed to a housing shortage.

But Airbnb cited data Tuesday, Sept. 3, that it says casts doubt on those claims one year from the law’s inception. Stays of less than 30 days fell in the city by 83% since September 2023, according to a report from Airdna.

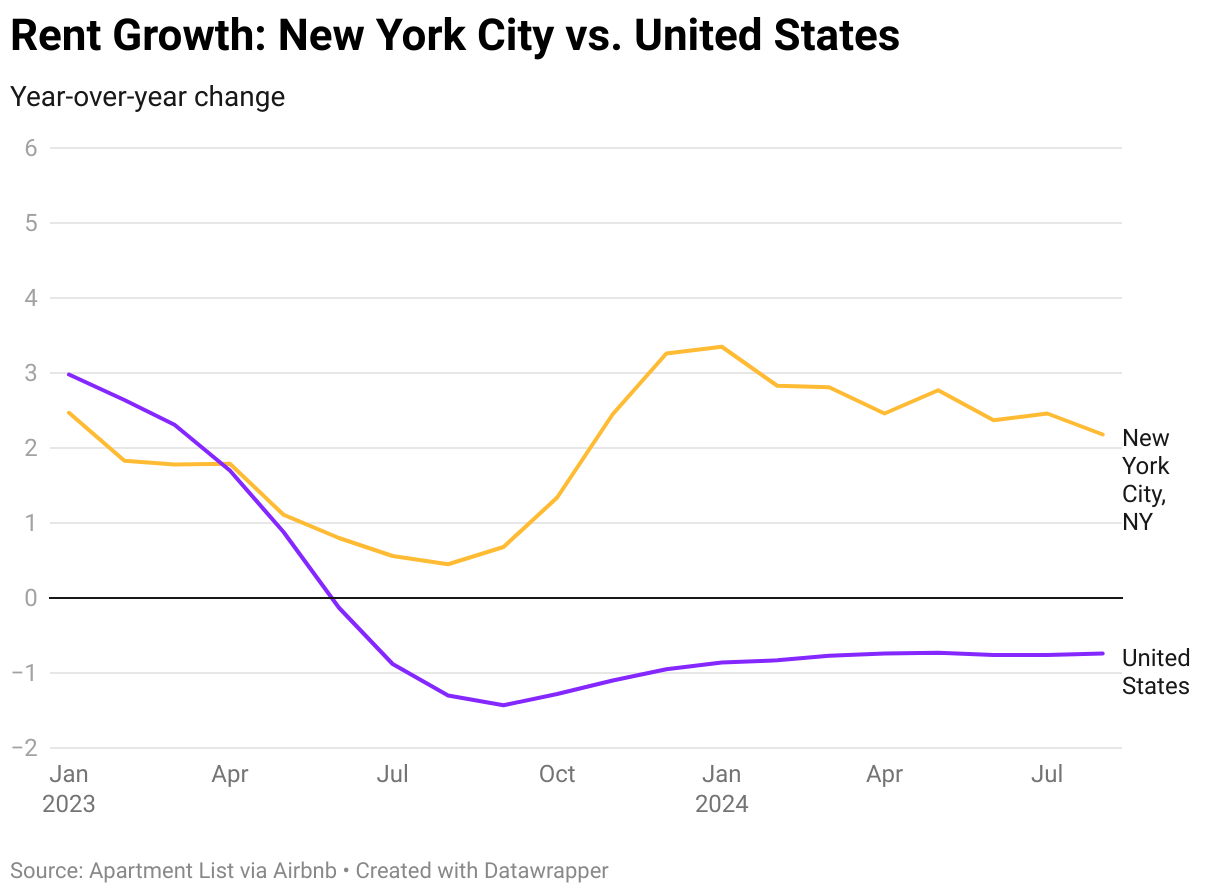

Rent growth in New York still rose 2.4% compared to last year, while nationally it fell by 0.8%, according to data from Apartment List. Meanwhile, median rent in Manhattan crossed $5,000 for the first time ever. Apartment vacancies were also nearly unchanged at 3.4%, according to Apartment List.

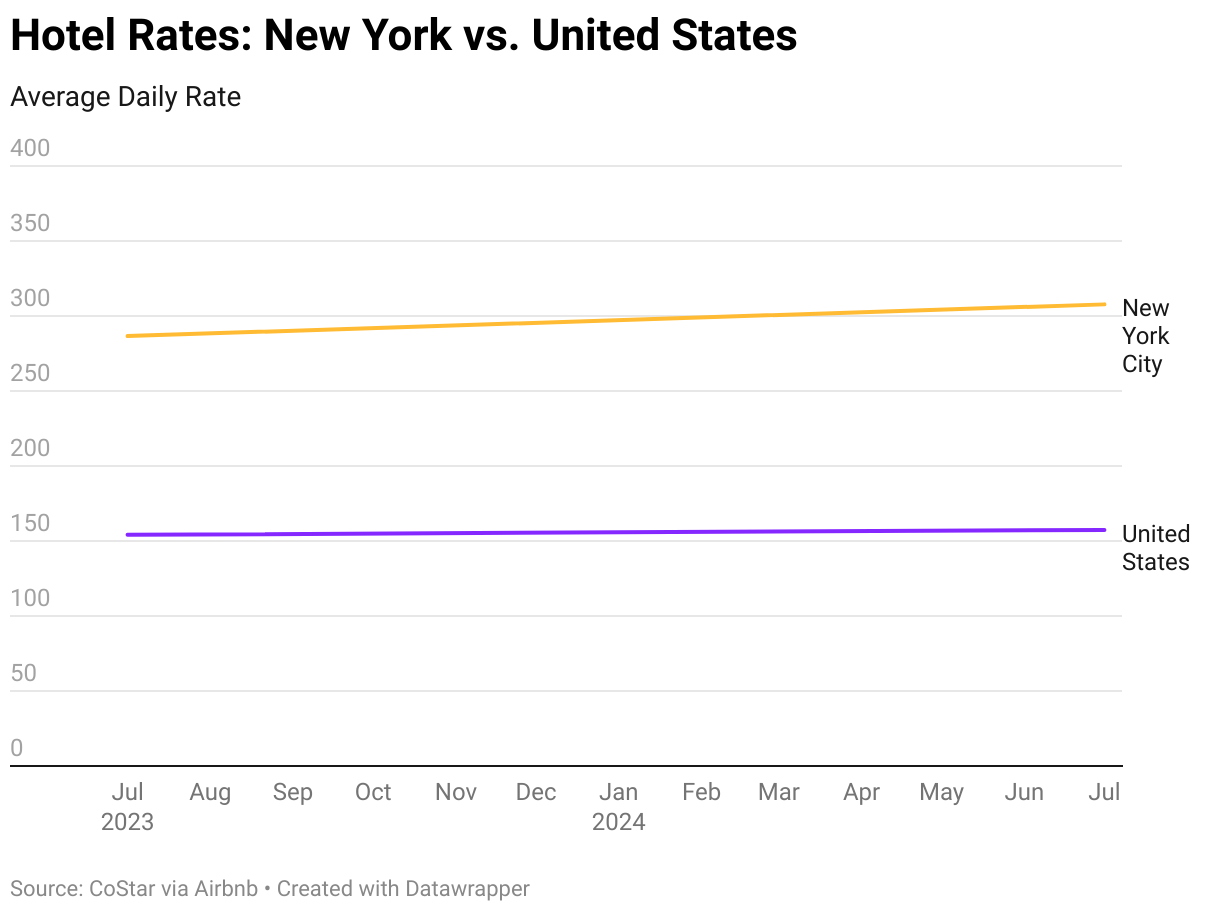

Airbnb said hotel operators are the true beneficiaries of the law, with the cost of a single night in the city surging 7.4% over the last 12 months, while nationally, it rose just 2.1%. The average night in New York runs $307.75, nearly double the national average of $157.39, according to data cited by Airbnb from CoStar.

“It’s time for New York City to reevaluate LL18 and consider amendments that would at a minimum, allow homeowners to once again host guests,” Airbnb’s Vice President for Public Policy Theo Yedinsky said in a statement Tuesday. “By rolling back parts of the law, the city can increase the supply of accommodations for consumers, support resident hosts, and revitalize local businesses that depend on tourism dollars. A more sustainable, sensible and equitable model benefits residents, visitors, and the broader community – ensuring that regulations support, rather than stifle, community and economic growth.”

Short-term rental apps have been blamed for rising rents and housing shortages throughout major U.S. cities.

“People own more than one home and rent them out for profit, while others struggle to afford their first home at all,” Tatum Joerndt explained in an analysis for the Lincoln Memorial University Law Review. “Being a renter through Airbnb allows the owner to make more money off these short-term stays than they would renting the property out as a home.”

New York isn’t the only city to pass short-term rental restrictions. In San Francisco, hosts can’t rent their homes for more than 90 days unless they are staying there at the same time. They also have to pay a hotel tax and follow insurance and safety requirements.

Meanwhile in Atlanta, one must be a city resident to own a short-term rental and they can only own two. Atlanta also charges a fee for an annual rental license and an 8% tax on rental fees for each property.

Quincy, a rural town in central Washington, is the most-searched summer travel destination on Airbnb. Quincy is seen as a perfect escape from the city, known for beautiful hiking trails, camping spots and the river. Quincy is also home to one of the most stunning music venues in the world, the Gorge Amphitheatre. Quincy is followed by Columbia, S.C. and Las Vegas as the most-searched summer destinations.

Americans surprise with confidence in economy though job concerns grow

Americans are more confident in the economy than analysts expected and that confidence has been growing throughout the summer. The Conference Board released its consumer confidence survey for August, with a 103.3 rating, beating the 100.7 expected and exceeding July’s 101.9 surprise.

It’s the highest confidence rating in months, but there’s more behind the headline number.

Conference Board Chief Economist Dana Peterson said that while consumers are more positive about business conditions now and in the future, they’re also more concerned about the labor market.

In July, unemployment rose to 4.3%. In August, fewer people told the Conference Board jobs were “plentiful” while slightly more said jobs were “hard to get.” Fewer people also expected their incomes to increase this year, while more expected their incomes to decrease.

That said, Americans’ inflation expectations dropped to their lowest level since March 2020. That comes as the Federal Reserve’s own inflation expectations are getting more rosy, as Fed Chair Jerome Powell addressed in his Jackson Hole speech last week.

“Inflation is now much closer to our objective, with prices having risen 2.5% over the past 12 months,” Powell said. “After a pause earlier this year, progress toward our 2% objective has resumed. My confidence has grown that inflation is on a sustainable path back to 2%.”

“He is confident now, not just waiting for more confidence, but confident that inflation is moving lower,” Central Bank Central Editor-in-Chief Kathleen Hays emphasized in an interview with Straight Arrow News. “It’s heading for that 2% target. And the concern is unemployment.”

Powell’s speech signaled a likely rate cut coming in September, and Americans are expecting interest rates to decline. That expectation, however, hasn’t made Americans rethink buying homes. Average responses over the past six months show plans to purchase homes are at a new 12-year low. But Americans are planning more smaller purchases. Buying plans for cars, refrigerators, TVs, washing machines, smartphones and laptops all increased.

Overall, Americans are feeling better about their family’s financial situation moving forward. They don’t see the results of the election causing much volatility in the economy and recession expectations are unchanged in August and well below 2023’s peak.

But confidence can be drawn along income lines. Those making less than $25,000 are feeling less confident overall, while those making more than $100,000 are the most optimistic.

Businesses, investors and the Federal Reserve all pay close attention to measures of consumer confidence. It’s a window into how much buying power Americans are comfortable yielding, and household spending accounts for more than two-thirds of the U.S. economy.

DOJ’s collusion case claims RealPage’s algorithm is the reason rent is too high

Have you been paying too much for rent? Across the country, rent prices skyrocketed in 2022 and 2023 and it could be because of illegal activity. The Justice Department on Friday, Aug. 23, filed an antitrust suit against RealPage, a Texas-based software company that is accused of using algorithms to allow widespread collusion among landlords.

“Everybody knows the rent is too damn high. And we alleged this is one of the reasons why,” Attorney General Merrick Garland said. “When companies, and in this case, landlords, use a software tool to facilitate cooperation with respect to rents, they violate the antitrust laws, they make rents higher than they would otherwise be, and they prevent rents from going down.”

The federal government joins attorneys general from eight states in suing RealPage. The company, which has been fighting these allegations for years, said the case lacks merit and will do nothing to bring down rent prices.

It’s a collusion case, it’s a price-fixing case, it’s a cartel case, but it’s not one where the landlords are accused of directly communicating or agreeing among themselves.

Professor Spencer Waller, Director, Institute for Consumer Antitrust Studies

“We are disappointed that, after multiple years of education and cooperation on the antitrust matters concerning RealPage, the DOJ has chosen this moment to pursue a lawsuit that seeks to scapegoat pro-competitive technology that has been used responsibly for years,” RealPage said in a statement.

To understand more about the case and its merits, Straight Arrow News interviewed Spencer Weber Waller, a professor and director of the Institute for Consumer Antitrust Studies at Loyola University.

This interview has been edited for length and clarity. Watch the full interview in the video above.

Simone Del Rosario: Professor, what is the difference between RealPage suggesting rent prices and what we see from a Zillow or Redfin estimate?

Spencer Waller: RealPage is a software system that has a very high market share among landlords in places like New York and some other cities. And the gist of this case, and it’s interesting, it’s a collusion case, it’s a price-fixing case, it’s a cartel case, but it’s not one where the landlords are accused of directly communicating or agreeing among themselves.

It’s kind of what we would call a hub-and-spoke conspiracy, where the landlords are using a common agent, a third party, to coordinate their behavior. And the complaint talks about how each of these large landlords feeds a variety of confidential proprietary information, and then the algorithm and RealPage communicates with them only, but it’s effectively the same as them communicating with each other because RealPage has access to all of this confidential information, uses it to formulate, according to the complaint, common recommendations that are inevitably followed by the landlord. And you end up with essentially the same result as if they had gone into a room or emailed each other and agreed to a common and ever-escalating rent for the various apartment buildings and other stuff that they own.

Simone Del Rosario: RealPage has been fighting these allegations for a couple of years now. They argue the software is not the reason prices are so high, that it is a lack of housing. They also say that their customers aren’t required to use this price, and in fact, many of them don’t use the suggested price. So what arguments does the DOJ and these other states have to make in order to prove their case?

Spencer Waller: There are two sets of cases going on: One is this government action that was filed late last week, and then there are separate class actions where groups of consumers are saying that they’ve overpaid. So the antitrust laws would not deal with a situation where a landlord had high prices on their own unless they were a monopoly and that isn’t at stake here. So high prices by themselves are not a violation of the antitrust laws without something more.

The something more in this case — a civil case, nobody’s going to jail, the government case has no fines — [is] the government is trying to stop the use of a common platform, a common algorithm, a common coordination point. And this has been done before.

If you go all the way back to the 1930s, there was a similar kind of case involving the movie industry where the government won, where they couldn’t really prove that the movie studios were trying to coordinate on price that would be charged in the movie theaters during the Great Depression; they couldn’t really prove that the movie studios talked to each other, but they had each sent sort of a common letter to their distributors talking about the prices that would be set. And that was enough.

So this hub and spoke where you use a third party to coordinate is an accepted legal strategy. Of course, the government has to prove this, but the complaint has a solid legal theory.

Other countries use similar kinds of coordination. I was an expert for the government of Chile some years ago where supermarkets were coordinating their price through a wholesaler. But again, there was no evidence that they specifically talked to each other. They may have, but the government couldn’t prove it. But to use a common agent to then formulate a plan to set a common price and/or raise it, those are illegal under U.S. law. Again, if you can prove it.

Simone Del Rosario: We are entering an era where AI and algorithms are going to be ruling business. What sort of things can we take away from the fact that algorithms are going to be calling a lot of the shots more and more?

Spencer Waller: Antitrust is grappling with this. The basic requirement for violation of Section 1 in the Sherman Act is some agreement in restraint of trade. It doesn’t have to be a written agreement. It doesn’t even have to be a formal agreement. It can be approved by direct or circumstantial evidence.

If you saw a bunch of people and you asked them how much for an apple on the street, and they each said $0.4325, that would be kind of odd. And you look into it, and you try to see if they had some mechanism by which they coordinated that price.

Now, it would be a pretty cut-and-dry case if each real estate company or anybody else coordinated through an accountant, through a trade association, or just like some expert consultant. There are all kinds of cases like this, where if you feed this common, highly-proprietary, highly-detailed, forward-looking information to a third person who formulates recommendations and then the recommendations are followed. That has held in other circumstances, other factual circumstances, to be enough to show an agreement. And that’s what the government is alleging here. And the fact that it’s a permutation involving an algorithm rather than a human or an old-fashioned way of coordinating is interesting. But that’s acceptable in a legal theory. And again, the law is reasonably easy. The facts are hard.

Simone Del Rosario: What do you expect RealPage to come forward with to say this is not collusion and it’s not an antitrust violation?

Spencer Waller: Well, at this stage, a complaint has been filed. I’m going to put on my hat as a civil procedure professor rather than an antitrust person. What happens now is the defendant has a choice. They can either file an answer, which just says, you admit, you deny, or you don’t know about the allegation. They would admit that they’re RealPage and they’re incorporated wherever they’re incorporated. And they would then admit and deny the key paragraphs of the complaint. And then the case goes into discovery.

Most defendants in this situation file a motion to dismiss that says even if everything in the complaint is true, it doesn’t amount to a violation of the law. A judge has to decide that. As I understand it, the government’s case is going to be decided by a judge, not a jury. The judge has to decide a motion to dismiss and the judge has to accept everything in the complaint as true and then measure it up against the law.

And as I was saying, the law is supportive of the government’s case. They’re smart people. They have good lawyers on this. The states are important partners in this case. They have other very gifted antitrust lawyers who work on this in conjunction with the DOJ. A little bit’s about the predilections of the judge, but I would expect that this is a strong complaint that’s a good chance of making it through the motion to dismiss.

At that point, the defendants have kind of a moment of truth. Do they want to spend the time and money turning over all their documents and depositions and other information to the government, a bunch of which they’ve already had to do? So they sort of know what’s coming.

And at that point, given that nobody’s going to jail and the government doesn’t get any money out of this, I would expect them to have some serious conversations about settling this case if, again, if it survives that motion to dismiss. If the defendants are successful in their motion to dismiss, the case is over and the government would have to appeal.

Home sales in July picked up after 4 months in a market slump

After a four-month slump, sales of previously occupied homes finally picked up in July. Lower mortgage rates and a rising number of homes on the market appear to have encouraged more home shoppers to make a move.

Despite the news, the increased supply of homes did not help cool home prices. Sales are still down 2.5% from this time last year. Although numbers came in slightly above expectations from economists, the market remains cautious.

Home prices have been steadily increasing for 13 consecutive months. The national median sales price climbed by 4% from last year, reaching over $400,000 in July.

The National Association of Realtors’ chief economist said while sales are still sluggish, consumers are seeing more options. Affordability is improved thanks to lower mortgage rates, and inventory is on the rise. There were 1.33 million unsold homes at the end of July.

The U.S. housing market has faced some serious challenges since mortgage rates began to climb in 2022. Last year, existing home sales plunged to their lowest level in nearly three decades, with mortgage rates hitting a 23-year high of 7.79%.

But there may be some relief on the horizon for prospective buyers. Mortgage rates have been easing recently, with the average 30-year home loan now sitting at around 6.5%. With inflation showing signs of cooling and signs of a softer job market, there’s speculation that the Federal Reserve may cut its benchmark interest rate for the first time in four years as early as next month.

New York City to use city land in massive housing expansion

New York City Mayor Eric Adams has issued an order to figure out what city-owned land would be best for housing development. The city is currently tackling an affordable housing crisis, as it struggles with a rental vacancy of just 1.4%

The order from Adams requires all city agencies from the New York City Police Department to the New York City Department of Parks and Recreation to look for city-controlled land that could be transformed into housing.

This is all part of a broader initiative by the Adams administration. The goal is 500,000 new homes by 2032 to help with that housing crisis. Mayor Adams emphasized that his administration is leaving “no stone unturned” in the quest to alleviate the housing shortage.

Projects like a recent rezoning in the Bronx will yield about 7,000 new homes, 1,700 of which are said to be below market rate.

The order also establishes a task force that will assess city-controlled land for housing potential and provide guidelines for agencies to support housing production.

Officials said they’ll explore every option, from garages to libraries, in order to deliver on their pledge to build half a million homes by 2032.