‘The time has come for policy to adjust’: Powell says rate cuts imminent

For the first time in definitive terms, Federal Reserve Chair Jerome Powell said it is time to cut rates after witnessing “unmistakable” cooling in the labor market. Powell made the remarks Friday, Aug. 23, at the Kansas City Fed’s annual economic symposium in Jackson Hole, Wyoming.

“The time has come for policy to adjust,” Powell said. “The direction of travel is clear and the timing and pace of rate cuts will depend on incoming data, the evolving outlook and the balance of risks.”

“We will do everything we can to support a strong labor market as we make further progress toward price stability with an appropriate dialing back of policy restraint,” Powell added. “There is good reason to think that the economy will get back to 2% inflation while maintaining a strong labor market.”

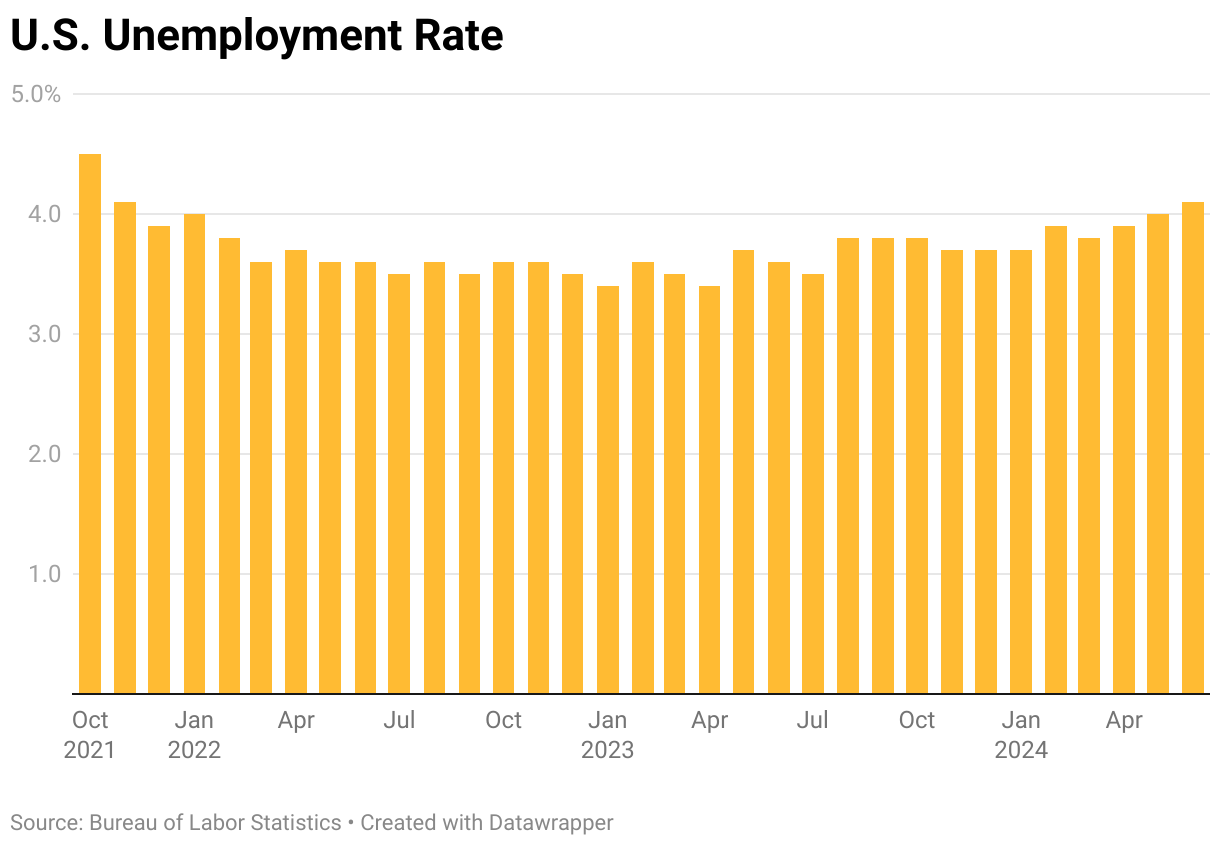

Despite the optimism, the labor market is undoubtedly slowing. In July, the unemployment rate spiked up to 4.3%, triggering a recession indicator. And the latest Labor Department revisions showed the Bureau of Labor Statistics overestimated job growth by 818,000 for jobs added throughout the year ending in March.

“The current level of our policy rate gives us ample room to respond to any risks we may face, including the risk of unwelcome further weakening in labor market conditions,” Powell said.

Given the remarks, markets are practically using permanent ink to mark a September rate cut. The Federal Open Market Committee, which sets the overnight lending rate, will meet three more times this year. Powell left the size and pace of rate cuts open to interpretation.

Is Powell’s ‘soft landing’ slipping away? Job worries cloud Jackson Hole speech

Jackson Hole, Wyoming, is known for its temperate summers, but Federal Reserve Chair Jerome Powell is probably feeling the heat turn up a bit ahead of his most-anticipated speech of the year. Powell will speak Friday, Aug. 23, at the Kansas City Fed’s annual economic symposium at Grand Teton National Park.

“This is his opportunity to send us a clear message on some aspect of what the Fed is thinking about,” Kathleen Hays, editor-in-chief of Central Bank Central, said. “I don’t think it’s going to be just looking at the economy and inflation. He’ll probably put this in a bigger context. At the same time, I think people are going to be waiting for him to just give us a little more guidance on where you’re leaning now.”

On Wednesday, the Fed released minutes from the latest Open Market Committee meeting in July. It decided to keep rates the same two days before a disappointing jobs report rocked people’s views of the labor market.

According to the minutes, the vast majority of people in that meeting expressed that it would likely be appropriate to cut rates in September. That said, several made comments that they could have also gotten behind a cut in July, which didn’t happen.

But here’s the kicker: Many participants noted that reported payroll gains might be overstated, and some noted the easing labor market faced a higher risk of more serious deterioration.

Now, it is confirmed that payroll gains have been overstated, just as many of those Fed members suspected.

“Since January of 2023, we’ve seen one downward revision after another to the data — it’s become systematic,” QI Research CEO Danielle DiMartino Booth told Straight Arrow News in August.

The latest Labor Department revision shows the U.S. economy added 818,000 fewer jobs than previously reported over 12 months ending March 2024. That’s about a 30% hit to what the Bureau of Labor Statistics initially released. It doesn’t mean those jobs were lost, it means they were never there in the first place. Therefore, while the labor market was still strong over those 12 months, it wasn’t on quite the tear the initial data indicated. These estimates will not be finalized until February 2025.

“And it takes a lot of time for the Bureau of Labor Statistics data to work its way into subsequent revisions for the Bureau of Economic Analysis data for GDP,” DiMartino Booth noted of revisions.

All of these moving parts are putting the Fed’s soft landing scenario at risk. A soft landing is being able to come down from too-high inflation without triggering a recession.

Inflation has come down quite a bit. The Fed’s preferred inflation measurement (core PCE) is at 2.6%, close to its 2% target. And the softening labor market is all the more reason to act.

In Powell’s speech Friday listeners will hope to hear from him that a soft landing is still in sight.

“We know the Fed’s going to be cutting rates,” Hays said. “We know they’re going to normalize. So it’s more of a question of when and how much and how fast.”

Complicating matters is the upcoming election. The Federal Reserve is a politically independent body and it would never want to be seen as carrying water for one party or another.

There is only one meeting before the election, on Sept. 17-18. Taking politics out of it, most economic signs point to the need to cut rates in September. But that will likely give the economy a boost, and that’s why in an interview with Bloomberg, Donald Trump said cutting before the election is “something that they know they shouldn’t be doing.”

The next Fed meeting starts the day after Election Day, but the Fed may not wait that long with the labor market showing these cracks.

Preview: What will Fed Chair Jerome Powell say at Jackson Hole?

The next time investors, economists, central bankers and other attentive Fed audiences will hear publicly from Fed Chair Jerome Powell is at his Jackson Hole Economic Symposium address.

People around the world will be listening for Powell to set the stage for the Fed’s next interest-rate decision. For more on what Powell might say, Straight Arrow News interviewed Central Bank Central Editor-in-Chief Kathleen Hays, who will be attending the symposium.

The following transcript has been edited for length and clarity. Watch the interview in the video above.

Simone Del Rosario: You’re going to be in Jackson Hole for this big speech that Fed Chair Jerome Powell will make. What are we going to hear from him that is different from what we hear in the FOMC press conferences?

Kathleen Hays: That’s a really good question, because in the press conferences, he gets hammered with questions. He will not be taking questions in Jackson Hole, No. 1. No. 2, I wonder if he’ll want to put the inflation that’s been experienced, where the Fed is now and where it’s going, into a bigger framework.

It was a tricky time. There were supply shocks, and one of the supply shocks was the labor market. There weren’t as many people there and so wages went up. Now all these things have happened and here we are now. And somehow give us this broader sense of how they’re looking at things now.

Could he talk about the neutral rate? Are we closer? Do we have to [move] the neutral rate up or down, etc.? What are the metrics they’re looking at?

One person suggested to me that he thought they could look at the upcoming framework review, which is going to start sometime in the fall. Remember, they changed their framework just when the pandemic was starting to say, “We have to see maximum inclusive employment before we would hike rates, and we’d have to see inflation at or above, I believe it was 2.5% and rising before we would start hiking rates to bring it down.”

Some people think that was one of the reasons that they move so slowly, too slowly, slower than they should have to start hiking rates when they did. And maybe that’s something he’ll address.

I myself think he’s going to keep it pertinent. He’s going to keep it more in terms of what everybody’s trying to figure out right now. And give us more of a framework, a bigger sense of being willing to move slowly, I’m not sure.

It’s up to him. And I think, after all the emphasis we’ve seen here and the market upheaval recently, it will behoove him to help us all understand better where they are now and what’s going to drive their coming steps. And maybe even cool off some of the idea that there’d be any emergency cuts because because markets go crazy for a day or two.

Simone Del Rosario: It would be interesting to hear him put this journey into perspective. It’s been a tough one for people out there, to live through a peak of 9% inflation, to continue to see inflation, for it to take so long for it to come down. We’re sitting here right now with a headline number of 2.9% and that looks incredibly promising when you look back at what we’ve been through to this point. So it will be interesting to hear if he puts the last several years into perspective, given everything that the economy has gone through since the COVID-19 pandemic.

How big will the Fed go with rate cuts after July’s inflation report?

Following the latest jobs report that showed a weakening labor market, consumer prices rose by less than 3% on an annual basis for the first time since March 2021. Given the Federal Reserve’s dual mandate of price stability and maximum employment, one is coming into focus while the other is slipping away.

How to interpret the data is up for debate and begs two big questions: How big of a rate cut will the Federal Reserve make and is it still on schedule for September?

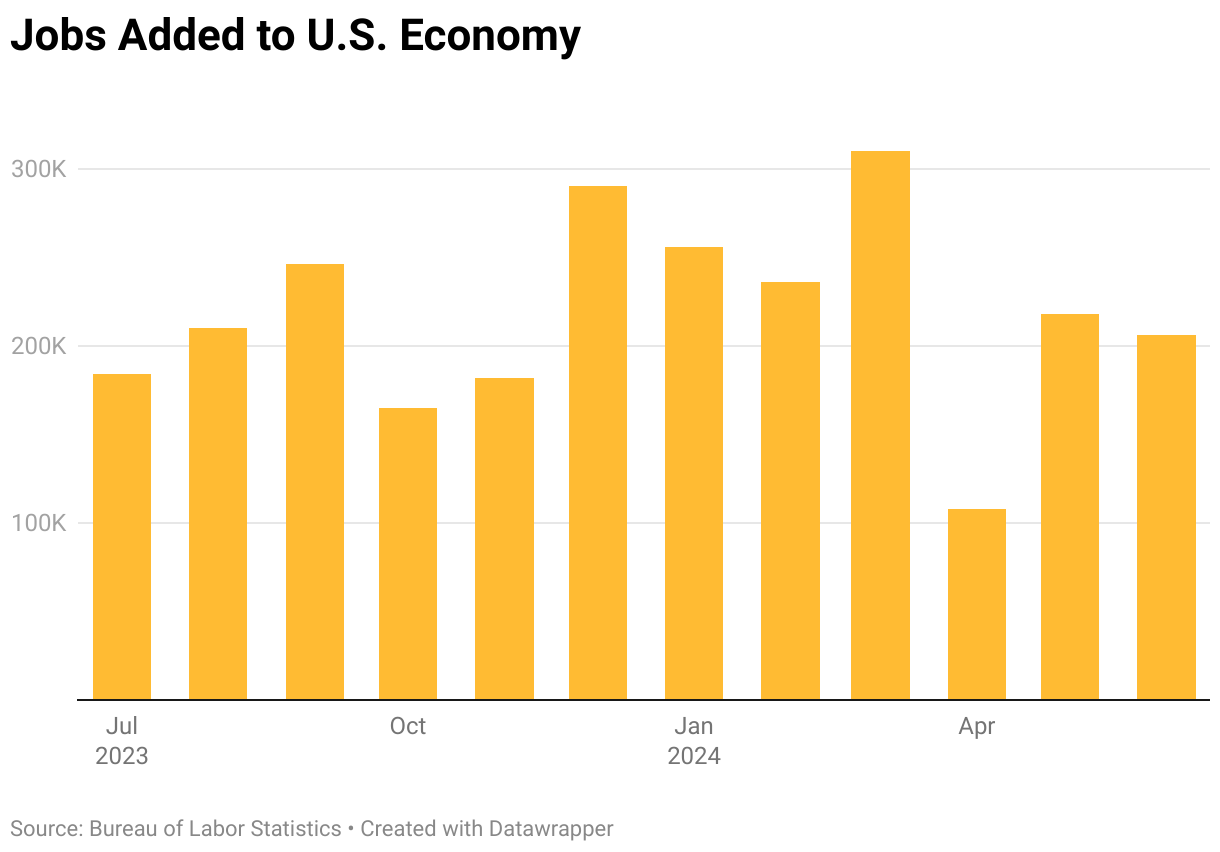

In July, the U.S. economy added 114,000 jobs, a huge miss from the 175,000 jobs expected. Unemployment ticked up to 4.3% from 4.1% in June. But consumer price inflation rose just 2.9% annually, inching closer and closer to the Fed’s target of 2%.

The Federal Open Market Committee won’t formally meet in August. Instead, central bankers will get together for The Federal Reserve Bank of Kansas City’s Jackson Hole Economic Symposium next week, where Fed Chair Jerome Powell will deliver an address.

“This is his opportunity to send us a clear message on some aspect of what the Fed is thinking about,” Central Bank Central Editor-in-Chief Kathleen Hays told Straight Arrow News.

While analysts still expect a cut in September, it’s unclear how big the Fed will go. Hays said calls for a 75-basis-point cut are out of touch and mostly a response to the “stock market carnage” from early August. She added that the odds of an emergency rate cut before the next meeting have dwindled the inflation data released Wednesday, Aug. 14.

Hays said the central bank leaders she speaks with are still looking at a cut between 25-50 basis points.

The following transcript has been edited for length and clarity. Watch the full interview in the video above.

Simone Del Rosario: There’s been so much conversation about how much the Fed is going to cut. People are even throwing out 75 basis points. This inflation report does not point to that.

Kathleen Hays: Oh, heavens, I don’t think anything pointed to a 75-basis-point emergency rate cut. Because [the] stock market had a big decline and then the yen carry trade blew up after the BOJ made its rate hike, that was not entirely expected, so they all fed together. It was a confluence of forces.

One of the people I spoke to said that these calls for 50-basis-point cuts, even 75 basis points, kind of smacked of investor entitlement. ‘Oh, if things are going bad, the Fed has to hop in and do something.’ So I think 75 basis points was more out of that ruckus, that big stock market carnage, if you will.

In terms of the numbers, it seems to me the Fed is moving slowly. Miki Bowman from the board of governors, in the last few days said she’s not convinced it’s time to cut yet. She thinks the labor market still looks pretty strong. Raphael Bostic, who’s president of the Atlanta Fed, in the last couple of days said he’s sure they cut rates by the end of the year, but he doesn’t think they’re necessarily there yet. Mary Daly, president of the San Francisco Fed, says that she does think they’re going to need to cut in the last part of the year.

It’s just a question now of when they start and how much they do. Does that mean they’re going to do 50-basis-point cuts? Doesn’t the more cautious, gradual, 25-basis-point cut get you there? If suddenly the labor market starts looking a lot weaker, then you could say that could mean they would speed things up. But even Austin Goolsbee, president of the Chicago Fed who’s one of the more dovish people on the Federal Open Market Committee, still says yes they need to cut, policy is restrictive, and there’s a concern if they wait too long the labor market will really start weakening

Simone Del Rosario: Most everybody was targeting September for a rate cut until that jobs report came out and then it was, ‘Why didn’t the Fed cut in July?’ We’re looking at a Fed that has been incredibly cautious. That said, we do have quite a bit of data between now and September. What does that jobs report in less than a month look like for the Fed to have more urgency? Do you think it’s going to be another bad jobs report? Or do you think that’s going to stabilize a little bit?

Kathleen Hays: Well, jobless claims just came back down to 233,000. And I think what’s very important [is the] Bureau of Labor Statistics had a very important number that they sort of downplayed in that report. We know that the unemployment rate jumped up to 4.3% from 4.1% and it wasn’t because necessarily people were losing jobs. It was because more people were coming into the labor force again. And when you start looking for a job and you don’t have one yet, you’re counted as unemployed.

I think even more important is the fact that the number of people who could not go to work because of weather, and that’s a category in the BLS numbers, was up over something like 460,000 in July. That month usually averages about 40,000. So many people have looked at that and said, ‘Hmm, maybe that’s one of the reasons. That was the week of the hurricane that we got that jump in unemployment. Maybe that affected payrolls.

We don’t know for sure but I think that’s one of the things that will be very interesting to see. Does the labor market, via the next jobs report look like, as some would say, normalizing? As former St. Louis Fed President Jim Bullard, said to me recently, he thinks you’re getting more to the natural rate of unemployment. The 3% employment, when it got that low, was kind of abnormal, right? And this is now more of a normal rate of unemployment. He’s convinced that the Fed will do 25 basis points in September. And remember, he was calling for that at the beginning of the year. He thinks they need to get less restrictive, and they can do it gradually.

The ‘Taylor Rule’ John Taylor from Hoover, from Stanford University, he thinks [that according to his rule] the funds rate needs to get down to about 4.5%, maybe 4%. And they could do that with two 25-basis-point cuts and a 50-basis-point cut.

That July weakness in the labor market is going to have to be verified by the August report. If it isn’t, it seems to me that’s going to be the perfect opportunity for them to say, ‘Yes, we know we can start cutting now, we can start normalizing. But 25 basis points at a time is enough.’

Simone Del Rosario: Is there any chance that they don’t cut? Let’s say, to your point, we get the next jobs report and it has normalized and this last month was a fluke. Then you get another inflation report like this. Is it convincing?

Kathleen Hays: My bet would be that they’d have to see another inflation report that is not as good as this one. Yes, this one made some progress on the headline. You can look at the monthly numbers as well. I think it would take something that looks like it’s pushing inflation back up again for them not to cut now.

The doors wide open, but thank goodness you’ve got Jay Powell at Jackson Hole next week and giving his all-important [speech at the] Kansas City Fed Symposium conference Friday morning. This is his opportunity to send us a clearer message, on some aspect, of what the Fed is thinking about. He doesn’t have to do that. I don’t think it’s going to be just looking at the economy and inflation. He’ll probably put this in a bigger context. At the same time, I think people are going to be waiting for him to just give us a little more guidance on where you’re leaning now.

Fed cutting rates before September like ‘yelling fire in a crowded theater’

Many argue the Federal Reserve missed the boat after failing to cut rates to ease financial conditions two days before latest jobs report triggered a recession indicator on Friday, Aug. 2. The Federal Open Market Committee is not scheduled to meet again until Sept. 17-18.

Now, experts are making the case for deeper rate cuts in light of rising unemployment. Some are even suggesting the Fed issue an emergency rate cut between now and the September meeting.

It would, at this point, be akin to yelling fire in a crowded theater if they were to come in with an emergency rate cut.

Danielle DiMartino Booth, CEO, QI Research

Former Fed adviser and CEO of QI Research Danielle DiMartino Booth said that while the Fed is behind the ball, an emergency cut would do “more harm than good.” In an interview with Straight Arrow News, she talked about the signs Fed Chair Jerome Powell missed that led to July’s decision.

The following transcript has been edited for length and clarity. Watch the full interview in the video above.

Simone Del Rosario: I know you have been warning about these underlying symptoms of recession for some time. The Fed chose not to cut in July and then two days later had this jobs report that wrecked the markets for a moment. Where are you? Are they okay to wait until September to cut? Do you want to see something from them in the meantime?

Danielle DiMartino Booth: It would, at this point, be akin to yelling fire in a crowded theater if they were to come in with an emergency rate cut. Those are usually reserved for end of the world type of moments, financial pandemics, financial crises, credit events. So I think at this point it would do more harm than good.

I was strongly of the mind that they should have cut rates at the July meeting. At the podium, when he was pressed, [Fed] Chair [Jerome] Powell did acknowledge that there was a discussion about whether or not to cut rates in July. So you know that even though the decision was unanimous, there were no dissents, that there were some who believed that they should have started in July.

This is nothing new, companies aggressively laying off. Again, it’s been occurring for most of 2024 and yet [Powell has] been ignoring it.

Danielle DiMartino Booth, CEO, QI Research

There’s a company called MacroEdge and they do a very transparent job of tracking job cut announcements. We’ve had an average of 100,000, more than 100,000 job cuts announced over the last four or five months here in a time of the year that is typically benign. Usually you see your worst month of the year be January, that’s when the CEO and the CFO come in and clean house. But April was worse and it’s been just awful ever since then. For heaven’s sake, we’re seven days into the month of August and we’ve already seen 40,000 job cuts announced.

We’re talking about Jay Powell here, he founded the Industrial Group when he was at The Carlyle [Group]. He speaks to lot of CEOs. He knows that they’re in the process of reducing their head count. So just in terms of data on the ground, anecdata, it’s all around him and it’s been all around him.

This is nothing new, companies aggressively laying off. Again, it’s been occurring for most of 2024 and yet he’s been ignoring it. So I really do think that he should have [cut rates] on July 31.

The reason I think that we’ve seen the Wall Street Journal mention 50 basis points is because that’s now become a base case for September 18 or we wouldn’t have read it in the Wall Street Journal.

Simone Del Rosario: We are going to get another month of jobs data before the Fed meets again. What sort of labor picture do you think it’s going to paint when we look up the first Friday of September to see what happened in August?

Danielle DiMartino Booth: I mean, anything is possible with this Bureau of Labor Statistics. I’m done guessing what they’re going to do and what they’re going to report. When the data is eventually revised by law, we see where it really, really is.

For me at least, because there is this systematic downward revision of the data, I just feel like it’s a politicized institution at this point. And I don’t say that lightly, and I’m certainly not trying to be insulting to anybody inside the organization.

I just feel like [the Bureau of Labor Statistics is] a politicized institution at this point. And I don’t say that lightly.

Danielle DiMartino Booth, CEO, QI Research

But you typically see the unemployment rate continue to increase after it’s stopped rising by a tenth of a percentage point. It’s what you’ve seen in many, many recessions looking back: Initially there’s a very gradual rise in the unemployment rate and then it really starts to take off. And we are seeing companies being much more aggressive and large with their layoff announcements and it is actually manifesting in the jobless claims data as well.

Simone Del Rosario: Is it politicized or are they just not as accurate at this point? Is the survey outdated or do you firmly believe that there are underlying political reasons why the picture is rosier when they first paint it than it turns out to be later?

Danielle DiMartino Booth: Again, we are having this discussion in August 2024 and we’ve been seeing downward revisions since January 2023. If, at this point, there has not been an internal recognition that the model is broken and it’s been addressed, then it’s what we call willful blindness.

So at some point you have to recognize that something is broken and address it, not just ignore it, unless you’re ignoring it willfully. And again, I’m not trying to be insulting of the institution, but we’ve just seen a headline in a $25 trillion economy that funding for the household survey is going to be cut. That’s the most ridiculous thing I’ve ever heard in my life.

In a world in which we have big data, artificial intelligence, ways to streamline operations, make certain practices and methodologies more efficient, that we can’t better track the U.S. labor force, it just seems nonsensical to me.

Here’s why this former Fed adviser says we are already in a recession

The creator of a recession indicator that was triggered this past week said her rule is broken this time around and there’s no recession right now. But not everyone agrees. In fact, a different recession indicator points to the U.S. having entered a recession in October of last year.

“We’re not in a recession,” Sahm Rule creator Claudia Sahm told Straight Arrow News. “It’s never time to panic, but it’s also not recession time either. So it’s not a recession. And yet the risks are there.”

Recessions are declared by the National Bureau of Economic Research in hindsight by looking at the economy’s growth over previous quarters. Recession indicators like Sahm’s look at rising unemployment rate trends for more immediate indications the country has entered a recession.

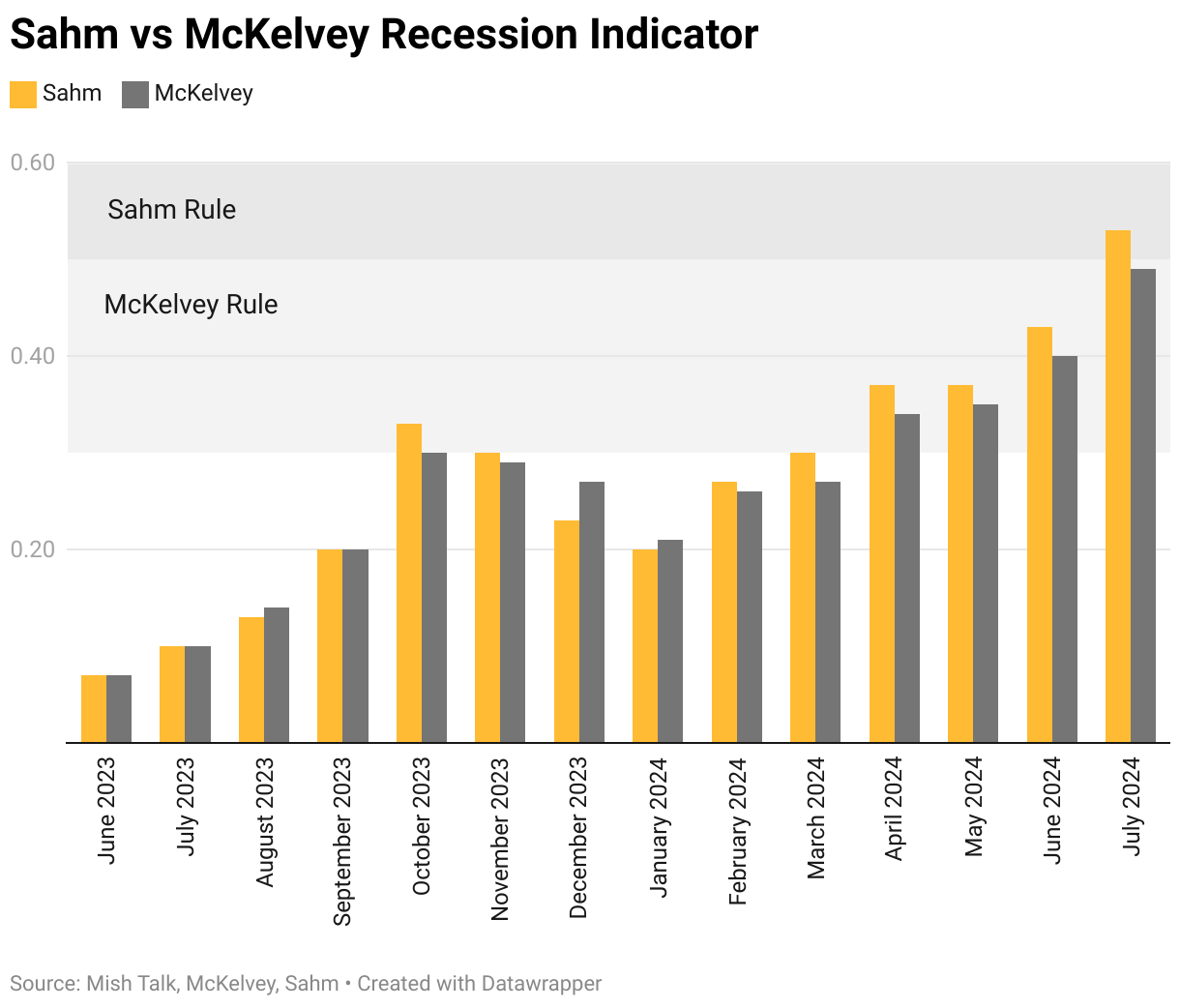

While Sahm’s rule was triggered by last week’s release of July’s jobs data, a different recession indicator was set off last October. In simple terms, the McKelvey Rule hits when the three-month average rise in unemployment hits 0.3 percentage points above the year’s low, compared to Sahm’s 0.5-percentage-point threshold.

The following transcript has been edited for length and clarity. Watch the full interview in the video above.

Danielle DiMartino Booth: I do think we’re in recession. Everything that we’ve seen from the Bureau of Labor Statistics with regards to the fourth quarter of 2023 indicates that they’re going to be revising into negative territory the final three months of 2023.

So that would stretch job losses from the third quarter of 2023 – when there were 192,000 jobs lost in the United States – that would stretch that into the fourth quarter and give us a six-month stretch of job losses upon revising the Bureau of Labor Statistics survey data with the hard data that we get from the Census Bureau, where companies are legally obligated once a quarter to report their headcount.

And that’s kind of the ultimate decision. That’s when the ink dries, if you will, on the payrolls data that we see the Bureau of Labor Statistics release.

Simone Del Rosario: So we’re looking at a recession that would have started in October of last year?

Danielle DiMartino Booth: I personally see the recession as having started in October 2023 because that’s the first time that the McKelvey Rule, which is less arduous than the Sahm Rule – and it doesn’t date back to 1948, it dates back to 1968 – but it has not missed a single recession since then.

Rather than a 0.5-percentage-point increase in the unemployment rate off of its lowest level in the prior 12 months, it is a 0.3-percentage-point increase in the unemployment rate over the prior 12-month period’s low.

Again, it has a spotless track record since 1968. It was triggered in October of 2023. The Bureau of Labor Statistics said that we lost 192,000 jobs in the three months ending Sept. 30, 2023. So the National Bureau of Economic Research could theoretically backdate it further, but again, the McKelvey Rule is what I’ve relied on.

The former chief economist at Goldman Sachs, he was interviewed by the Wall Street Journal in January 2008 when his rule was triggered, and he was asked the same question: ‘Well, your McKelvey Rule was triggered in December of 2007. Do you think we’re in recession?’ And he said, ‘Well, you know, my rule might be broken,’ basically.

But of course, the NBER did backdate that recession to December 2007 and the McKelvey Rule was not broken. Luckily, the Bloomberg Economics team agrees with me that recession, that job losses started in October 2023.

Simone Del Rosario: Why isn’t the Federal Reserve looking at these data points?

Danielle DiMartino Booth: I think the Fed is choosing to look the other way in this instance. There are some regulations that the Fed has been working on that could really define Chair Powell’s legacy – that would begin to regulate the private equities, the hedge funds, the BlackRocks of the world that are in some cases larger than banks if you consider the trillions of dollars that they have under management – and in order to push through with some of these regulations, he really does need higher-for-longer [rates] on his side.

He needs the higher-for-longer policy enough to go with what the Bureau of Labor Statistics first reports, even though we know that since January 2023, we’ve seen one downward revision after another to the data. It’s become systematic, in fact, the persistence with which we’ve seen downward revisions to what’s first reported. But again, I think [Fed Chair Jerome] Powell’s got his own reasons.

Simone Del Rosario: How do you square this idea that we could be in a recession right now with the GDP numbers that we’re seeing? The latest reading, the advance estimate, showed an annual growth rate of 2.8%.

Danielle DiMartino Booth: So we had 2-point-something percent in 2001 when it was first reported. Of course, it was another six quarters later that we revised it and found out that it was a negative number.

It takes magnitudes of the amount of time to get correct unemployment data, correct payrolls data. You can double the time that it takes to figure out what the actual GDP is that’s associated with that time frame.

If you find out that you’re 830,000 jobs shy of what you thought you were, which is what we found out in the third quarter of 2023 looking backward with hard data in hand, then you have to subsequently go back and back out. Well, 830,000 people were not actually working; 830,000 people were not actually producing the economic output that we thought we were. So you’ve got to back that out.

It takes a lot of time for the Bureau of Labor Statistics data to work its way into subsequent revisions for the Bureau of Economic Analysis data, for GDP.

It’s at inflection points. It’s when contractions become expansions, when expansions become contractions, that these big statistical agencies have trouble seeing the turning point, given their modeling.

But it wasn’t until 2018 that we saw the final GDP revision from the Great Recession that ended in June 2009. Again, the recession ended June 2009. We didn’t get the final revision for GDP for that recession until 2018.

Simone Del Rosario: On one hand, this can seem incredibly frustrating if people feel like we’re in a recession, they feel like the economy’s not good, and yet we continue to get, on the surface, economic releases that show a pretty strong economy. But that said, if, to your point, we are already in a recession, does that take some of the panic away since we’ve already been going through it, or is it going to get worse? What’s your read on that?

Danielle DiMartino Booth: Well, your average recession is 10 months long in the post-war era. So using that average length of time, we should theoretically be starting to recover and coming out of recession.

That being said, the Federal Reserve has waited now 12 months, now longer than 12 months, and the longer it waits, typically the deeper and longer the recession is as a result.

There have been some great studies that empirically demonstrate this. The period leading up to the Great Recession, 2007-2009, the Fed waited 15 months. It’s the longest the Fed’s ever waited.

So we’re just at the 12-month mark now. But it certainly looks like we’re going to get to the 14-month mark if it’s Sept. 18 that we can anticipate that first rate cut. So that’s about as long as the Fed has ever waited to provide relief in the form of the beginning of an easing cycle.

Why the Sahm Rule creator says the recession rule is wrong this time

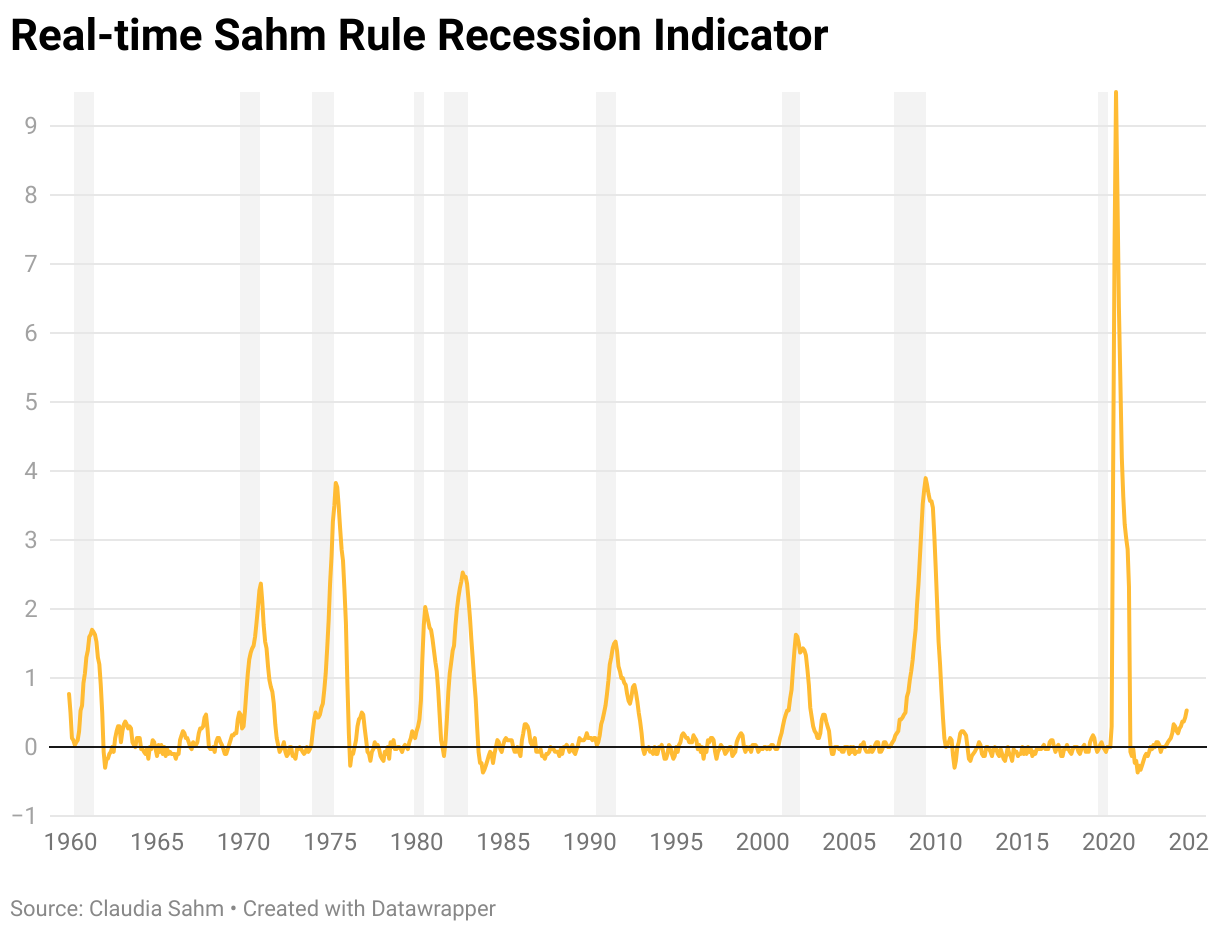

Recession fears have dominated headlines since Friday’s jobs report, where the rising unemployment rate triggered a recession indicator known as the Sahm Rule. The rule has an incredible track record of signaling the start of a recession, yet this time is an outlier, according to the rule’s creator.

The Sahm Rule states a recession in the U.S. has started when the three-month average of the unemployment rate crosses 0.5% or more relative to its low from the previous 12 months. July’s surprise unemployment rate of 4.3% triggered the Sahm Rule with a 0.53% rise.

Asked point-blank whether the U.S. is in a recession, Claudia Sahm told Straight Arrow News, “No, we are not.”

It’s not a recession and yet the risks are there because we do have these increases in the unemployment rate.

Claudia Sahm, Chief Economist, New Century Advisors

The following transcript has been edited for length and clarity. Watch the full interview in the video above.

Claudia Sahm: We should be concerned that [the unemployment rate] has been rising over the past year. And this is not just about hitting a particular level, or in July, we saw a larger jump than we’ve seen. The Sahm Rule averages across months. It looks over a year-long period. So it’s trying to get this direction that we’re headed and it’s not a good direction.

Now there are some very specific reasons, very special reasons that the Sahm Rule right now looks more ominous than it is. And the first thing we can say about, “we’re not in a recession,” is anytime we make a pronouncement like that, we should look around.

And in fact, broadly speaking, this economy is still growing and a recession means that it’s contracting, right? So we still see consumer spending, we’re adding jobs, industrial production. It’s slowed down, it’s not growing as fast, but we’re still growing. So that’s not a recession – right now.

So what’s going on with the unemployment rate? So there’s the bad reason unemployment rate goes up is there’s less demand for workers, it gets harder to find jobs. Hiring rates have come down a lot. It is a lot harder if you’re on the outside trying to find a job right now. So the unemployment rate has gone up for a bad reason. It does that in recessions.

The unemployment right now is also going up for one of the good reasons. So we have had more people join the workforce who weren’t working before. In particular, there was a big increase in immigration. And that was so important for solving the labor shortages that we’ve been suffering through. And yet, it takes time to adjust. I mean, that should be the theme of this cycle since the pandemic, that big messy changes take time and it’s painful.

It can make it really hard to read where the economy is, but right now we have people who’ve come in, and for some of them, it’s just going to take time for them to find jobs. And in that period, the unemployment rate will go up. Once they find the jobs, it can come back down. And frankly, people coming in to work, that’s a good sign for keeping the economy growing because there are more workers. That extra piece of unemployment rate increase looks bad but actually, it’s probably not.

I can say, looking broadly, what we know about the economy, we’re not in a recession. I mean, it’s never time to panic, but it’s also not recession time either. So it’s not a recession and yet the risks are there because we do have these increases in the unemployment rate that are of the more problematic kind, we just don’t know exactly how much.

Simone Del Rosario: When you created this rule, it was so policymakers could act on signs of a recession. Looking at what’s happening right now, there’s obviously a major movement happening with unemployment. What’s the remedy?

Claudia Sahm: There is a very clear policy lever out there to be pulled and that is the Federal Reserve beginning to reduce interest rates. And that’s the most straightforward one at this point. And the Fed has told us they are pointed at doing that.

Before we found out about July’s employment report, that’s the path they were on. Seeing that there is probably more weakness or at least more slowing in the labor market than we had previously thought, that probably means that they can get going in September, and maybe even cut interest rates more quickly than they had expected.

And it’s important that they have that lever to pull. It’s so important that we’re still in a position of strength. We’re not in a recession, we are still growing, there’s a lot of good things in U.S. economy.

The direction is not good, right? We don’t need to soften or weaken more than we have and that’s kind of where we’re pointed. And the realization that the Fed has been putting pressure on the economy to slow it down and for them to say, “Okay, we don’t need to slow it down anymore,” and reduce risk, that is the release valve to this that can get us to a good place.

That we just kind of settle into the jobs catch-up, we keep growing, we stay away from the recession. That’s the path. And you can tell the story and the path is there. It’s just anytime you get close to these real risky places in the economy, like a recession, you have to be careful because the people can get scared, markets can react. Things can unfold in unpredictable ways. So I think people should have their guard up more than a typical time and yet, there’s still a path to this all being just fine.

Simone Del Rosario: Are you concerned about a near-term recession or are you confident that when the Fed pulls that lever, the risk is over?

Claudia Sahm: I’m a macroeconomist. I’m always concerned. I devoted much of my career to studying recessions and how to fight them. And so I think it’s a risk that we should always be aware of, or at least policymakers should certainly be aware of. It is not my base case.

And again, I don’t want to make light of the Sahm Rule. The pattern I identified, there are other similar people looking at labor market conditions, it’s not like I’m the only one who’s pointed to weakness right now.

It does have a really strong track record and I don’t want to dismiss it out of hand. Something is happening and I don’t want to just write off any of the bad signs because now would be the time to act on them. Given all that, I think the risks are there. They’re not overwhelming. And because we’re still in a position of relative strength, that gives us a real leg up in terms of like what happens over the next three months, six months, 12 months.

Simone Del Rosario: Did the Fed make a mistake last week by not cutting?

Claudia Sahm: I have made the argument for much of this year that the Federal Reserve should begin to gradually lower interest rates, that inflation was coming down. Yes, the beginning of the year was a little rough. We’re also learning that we probably got head-faked by some of that data. We might be getting head-faked by some of the employment data now. It might not be as bad as it looks, right? But there was definitely a case, inflation is coming down, the Federal Reserve should get out of the way.

I had said last week they should start gradually reducing rates because it would be so much better to gradually reduce interest rates, watch the effects on the economy, because there are many question marks. We don’t know exactly how this amount of interest rate cuts translates into that amount of spending. So just to kind of watch and see what the economy does.

Hindsight’s 20-20. I think they could have been the winner last week if they had gone ahead with a cut, but you don’t get to go back and redo. I firmly believe they will assess the situation and take the steps necessary. It takes time for their tools to work so they do need to get going. But it’s not like all is lost. They’re going to have to probably play some catch up and they won’t get to do the victory lap.

Simone Del Rosario: The Fed is finding itself back in a position that it was when it started the hiking campaign, which was that it started hiking too late and then they were doing massive hikes. There’s all this talk now about how much more they may have to cut in September and beyond. Do you think that’s overblown?

Claudia Sahm: This cycle was always going to be messy. This has been a very hard-to-read economy. If you think about it, 2022, the Fed went really fast. They raised interest rates really quickly. There were a lot of concerns that we were going to be in a recession, that that was going to be part of what we had to have happen to get inflation down because it had gone up. Well, in fact, two years later, there has been no recession and we had a big disinflation.

It was not pretty in terms of how you would necessarily want the policy to roll out, but things worked out relatively well. So just because it doesn’t have this elegant, gradual cuts, it’s about getting the job done.

It clearly creates strain on families and businesses when they see the stock market, big numbers moving and what comes next. Fear can take on a life of its own and that is something that lives around the edges and in the middle of a recession. So you don’t want to treat those dynamics lightly, but we’ve dealt with a very uncertain, hard-to-read world for the last four and a half years. So we’re not done with the drama.

It was a missed opportunity by the Fed. At least that’s what it looks like today. We’ll get inflation data next week, maybe it doesn’t. But it looks like that was a missed opportunity, but there are so many more opportunities ahead of them to do good policy.

Employers added only 114,000 jobs in July, according to data released Friday, Aug. 2, by the Bureau of Labor Statistics. That number missed economists’ expectations of 175,000. Meanwhile, the unemployment rate in July ticked up to 4.3% from 4.1% in June. July marked the fourth straight month the unemployment rate rose and it is at its highest level since October 2021.

“I don’t think that this report tells us that we’re headed for recession,” former Acting and Deputy Labor Secretary Seth Harris told Straight Arrow News Friday. “The GDP [gross domestic product] numbers don’t give us any indication that we’re headed for recession. The second quarter GDP numbers were good, solid numbers; not booming, but very good for this deep into a growth cycle in the United States.”

Real GDP is estimated to have risen by 2.8% year over year, according to the “advance” estimate released by the Bureau of Economic Analysis. The official number will be released on Aug. 29.

The Sahm Rule

These latest recession fears come from what is known as the Sahm rule, developed by economist Claudia Sahm. The rule states a recession in the U.S. has started when the three-month average of the unemployment rate crosses 0.5% or more from the previous year’s low.

“I agree with Claudia about Claudia’s rule, and that is that it can be a little bit too pessimistic, particularly when you are at, historically, very, very low unemployment rates,” Harris said, referencing Sahm’s own contention that the rule could be overstated in this instance due to labor market behavior from the COVID-19 pandemic and an increase in immigration.

“We’ve seen that we had a period of more than two years of unemployment rates below 4%,” Harris told SAN. “That’s the longest period we’ve had that low [of] unemployment since the 1960s. But it shows us that our economy can be immensely successful with an unemployment rate that gets to and remains below 4%. That is where full employment begins.”

Meanwhile, Harris said movement in the markets due to an imminent recession is an “overreaction.”

“We’ve seen a meaningful sell off in equity markets around the world, not just in the United States, but certainly here in the United States over the course of the last several days, and a part of that is recession concerns, which is, in my view, a gross overreaction to what we’re seeing right now,” he said. “We certainly are not seeing numbers that suggest that a recession is imminent, or the recession is even an intermediate-term concern. It can be a longer-term concern, but I don’t think we can see it as an intermediate-term concern.”

However, Sahm herself, who stands by her statement that the U.S. is not currently in a recession despite triggering her rule, told Yahoo! Finance Friday that she is “very concerned” about a recession in the next three to six months.

After July’s big jobs miss, experts say a 50bps cut should be on the table

Experts are criticizing the Federal Reserve for being behind the ball after July’s jobs report showed a weakening labor market, two days after the Fed decided to leave its interest rate unchanged. Economists say the Fed’s restrictive monetary policy is now hurting the once-robust labor market.

In July, the U.S. economy added 114,000 jobs, a huge miss from the 175,000 jobs expected. Unemployment ticked up to 4.3% from 4.1% in June.

“I think that all of those indicators tell us that the Fed needs to act. They should have acted in their last meeting, maybe even a little earlier than that,” said Seth Harris, former Acting and Deputy Labor Secretary under President Barack Obama. “Now the question is, how big of a bump do they need to give? Is it 25 basis points? Is it 50 basis points?

“Let me just say, nobody was talking about 50 basis points before this report,” he added. “I think we’re now going to see people talking about 50 basis points and some folks will even talk about more. So I think that this report really sends a signal to the Fed. The boat is pulling out, the train is leaving the station, whatever analogy you want to use, and they need to get on board.”

Fed Chair Jerome Powell hinted that a September rate cut could be on the table during a press conference Wednesday, June 31, ahead of Friday’s jobs report.

The Fed is holding its interest rate at a two-decade high in an effort to tame inflation, but Harris said the weakening labor market requires a more decisive approach.

“Go ahead and cut rates aggressively and send an indication that you really are concerned about growth and you’re also concerned about employment,” Harris told Straight Arrow News. “To me, a 25 basis point cut was signal sending. It wouldn’t have had a dramatic effect on the economy directly, but by sending the signal that their concerns about inflation have been reduced, that inflation descended to a level that suggests that we’re going to be just fine in that area, but that they are also concerned about growth and employment.

“That was signaling, not policymaking. Now, I think they have to think about policymaking. After seeing these numbers, I think they have to think about policymaking.”

What the June jobs report tells us about the state of the economy

The June jobs report came back a bit of a mixed bag. On the one hand, the U.S. economy added slightly more jobs than expected at 206,000. On the other hand, the unemployment rate ticked up to 4.1%.

It’s the first time the unemployment rate has been above 4% since late 2021. Analysts had expected unemployment to stay at 4% and anticipated around 200,000 jobs added.

“The big downward revisions to April and May are the story,” Charles Schwab Chief Fixed Income Strategist Kathy Jones said on X. “Job market is slowing down.”

Historically, an unemployment rate of around 4.1% is strong. But since the economy has been below that for 2.5 years and reached a five-decade low of 3.4% unemployment in 2023, the upward trend is catching attention.

The Federal Reserve last projected unemployment would be at 4% for 2024 and 4.2% for 2025, so already exceeding that 2024 number makes a rate cut look all the more likely. The Fed is now projecting one rate cut this year. The market is betting the Fed will hold steady for its July meeting and cut in September.

Back in May, Fed Chair Jerome Powell said there are two paths to cutting rates.

“That we do gain greater confidence that inflation is moving sustainably down toward 2% and another path could be unexpected weakening in the labor market, so those are paths in which you could see us cutting rates,” Powell said.

The Fed’s preferred inflation gauge shows prices rose 2.6% annually in May. The more widely-cited consumer price index shows a 3.3% rise in prices. Meanwhile, wages are outpacing inflation, rising 3.9% over 12 months in June, though the pace of wage gains is slowing.

While the latest jobs data still shows a robust labor market, it is softening from its status as one of the strongest labor markets in history.

An unemployment rate between 4%-5% is considered “full employment,” which is when a country’s available labor is being used in the most efficient way.

Full employment does not mean zero unemployment. Economists believe there needs to be some level of unemployment to minimize inflation and allow people to move between jobs, pursue education or improve job skills. The idea of full employment is that people looking for full-time work should be able to find it, although it might not be their preferred job.

But initial unemployment claims are trending up and the number of people who are unemployed for more than half a year is also climbing. More than a fifth of the unemployed fall under that category, while the median amount of time people are unemployed is nearly 10 weeks. One year ago, it was 6.4 weeks.