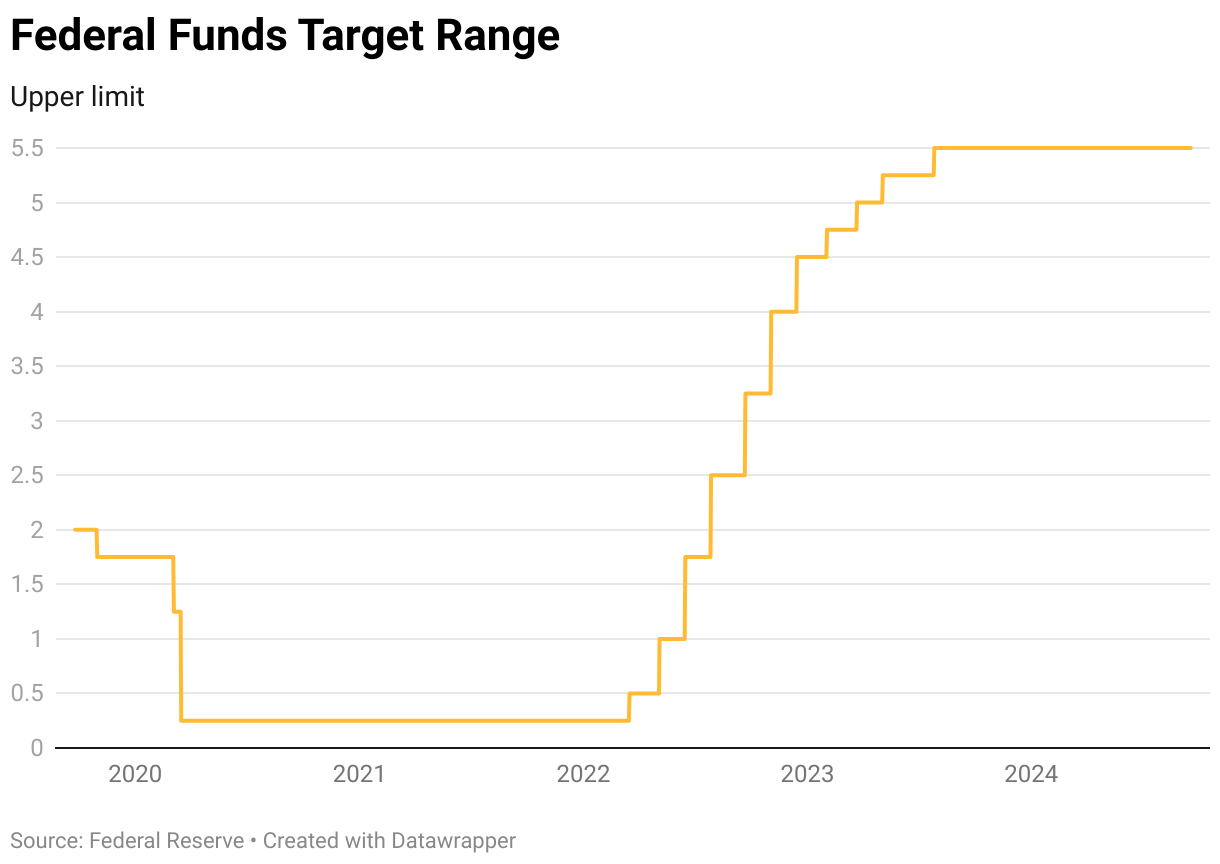

Falling interest rates may pique the interest of prospective homebuyers but experts don’t necessarily think it is going to loosen the market anytime soon. The rate for a 30-year fixed mortgage averaged 6.09% for the week, according to Freddie Mac. The dip comes as the Federal Reserve cut its benchmark interest rate by 50 basis points on Wednesday, Sept. 18.

Mortgage rates have been slowly declining since hitting a 23-year high of 7.79% in October 2023. Though rates may still seem pretty high, every percentage point makes an impact. For every one percentage point mortgage rates increase, buying power lowers by 10%.

At the same time rising mortgage rates decreased buying power, housing prices skyrocketed. Even with recently falling mortgage rates in anticipation of the Fed cutting its key rate, the housing market has barely budged.

Existing home sales fell 2.5% in August, according to a release from the National Association of Realtors.

What do further rate cuts mean for prospective buyers and sellers? Straight Arrow News interviewed Selma Hepp, chief economist at CoreLogic.

This transcript has been edited for length and clarity. Watch the full interview in the video above.

Simone Del Rosario: Homeowner hopefuls have been putting off plans to buy for years. Are these lower rates going to be the entrance point they’re looking for?

Selma Hepp: I think the lower mortgage rates are certainly helping. Every time we saw mortgage rates come down, it did help spur some buyer demand. For example, when you think about what happened after the Fed meeting last December, mortgage rates came down. That certainly spurred housing market demand; same thing the year prior.

So whenever we move closer to 6% and further away from 7% and even come down to the 5% range, it does help with affordability. It helps with a buyer’s budget and it brings back that demand that we desperately have been needing in the housing market.

Simone Del Rosario: Is it possible that more affordable mortgage rates could actually drive up housing prices since more buyers would be trying to enter the market?

Selma Hepp: Yeah, that’s a question that keeps coming up because everybody’s worried that there’s so much pent up demand and not enough supply, meaning that as soon as mortgage rates come down, you’ll see more buyers coming in and pushing those prices higher. That’s certainly a possibility, but what we did see over the course of this year is more inventory of existing homes for sale, and that has helped put a lid on home price appreciation.

And the other thing is, when you think about mortgage rates further coming down, it’s going to unlock some of that inventory that’s been locked in because the difference was so high between where people locked in and where mortgage rates were.

So with that spread coming lower, I think we’re going to see unlocking of some of that inventory, so the balance between buyers and sellers is going to be better, and it’s going to keep the lid again on the rate of home price appreciation. So we certainly hope for that going forward.

Simone Del Rosario: For sellers looking at the market right now, when would be an optimal time for sellers to enter the market?

Selma Hepp: That’s usually very individual decision. It depends on how long you’ve owned the home. Are you moving to another place where home prices are more affordable or not; are you staying in the area? And it depends also, on what your family situation is.

A lot of time sellers are driven by a change in family status. So they are either selling because they need a bigger home or there is a divorce situation, or maybe somebody is no longer around, and so that’s usually what drives sales.

That’s the most frequent reason for sales, but sometimes lower mortgage rates are helping. They do help sellers sort of feel better about their next purchase because it’s more affordable again. And I think definitely with mortgage rates coming down, it’s going to help with that sense of, ‘How much am I giving up to buy my new home?’ So yeah, I think it will help the number of sellers in the market as well.

Simone Del Rosario: Yes, selling a home is an individual decision and has to do with your personal life. But what we’ve seen over the past couple of years is people holding onto their low interest mortgage rates and not moving on to the next home when they typically would.

So this could unleash sellers, but at the same time, I believe the sellers would want to have the best price they can get for their house since they’ve waited so long to be able to sell it.

Selma Hepp: That’s often an interesting dilemma because you want the most you can get for your home, but then you also think about, with next home that you’re purchasing, that next seller is gonna want for the most for their home as well.

That’s always a dilemma that sellers find themselves in, but you’re absolutely right in terms of length of tenure for sellers. Over the course of the last couple of decades, we’ve seen people staying in their home longer and longer because homes have become increasingly more unaffordable and there are fewer homes available for sale.

So oftentimes what I hear sellers say is, ‘I do want to sell. I do want to move, but where am I going to move? There’s no inventory. There’s not something that fits what I’m looking for.’ And so they just end up staying put.

Simone Del Rosario: Obviously, these mortgage rates have been a large part of people’s decision-making process. But as you just pointed out, that’s not the only thing that is stalling the housing market. What are the other things that are making the housing market more sticky?

Selma Hepp: Affordability is the biggest one. But affordability, the lack of affordability, comes from the fact that we’ve under built for so long, particularly first-time or entry-level homes. So when people are trying to think about their first home or thinking about moving to another home, there are fewer homes to choose from. So that’s holding people back a lot.

We definitely saw that. For example, mortgage rates came down in early spring of 2023 and we saw a burst of buyers coming into the market, but there were not enough homes for sale. And that’s when home prices surged again and we saw significantly more appreciation in the market because of that imbalance.